Treasury Board of Canada Secretariat

www.tbs-sct.gc.ca

Common menu bar links

Breadcrumb Trail

ARCHIVED - Royal Canadian Mounted Police

This page has been archived.

This page has been archived.

Archived Content

Information identified as archived on the Web is for reference, research or recordkeeping purposes. It has not been altered or updated after the date of archiving. Web pages that are archived on the Web are not subject to the Government of Canada Web Standards. As per the Communications Policy of the Government of Canada, you can request alternate formats on the "Contact Us" page.

Section III: Supplementary Information

Financial Tables –Summary of Departmental Strategic Outcomes as per Program Activity Architecture

Table 1: Comparison of Planned to Actual Spending (including FTEs)

| Program Activity ($ millions) |

Actual 2005-2006 |

Actual 2006-2007 |

2007-2008 | |||

| Main Estimates | Planned Spending | Total Authorities | Actual | |||

| Federal and International Operations | 579.7 | 626.0 | 685.5 | 796.5 | 834.4 | 659.5 |

| Protective Policing Services | 125.7 | 108.9 | 112.3 | 129.0 | 149.5 | 140.1 |

| Community, Contract and Aboriginal Policing | 1,991.8 | 2,140.7 | 2,335.1 | 2,378.7 | 2,543.9 | 2,289.0 |

| Criminal Intelligence Operations | 71.6 | 81.8 | 85.5 | 91.5 | 91.7 | 90.8 |

| Technical Policing Operations | 168.8 | 190.8 | 187.2 | 198.8 | 217.0 | 212.5 |

| Policing Support Services | 67.3 | 84.0 | 70.7 | 72.1 | 81.5 | 91.4 |

| National Police Services | 161.9 | 170.9 | 144.1 | 158.0 | 174.1 | 178.0 |

|

Registration, Licensing and Supporting Infrastructure |

68.5 | 74.2 | 66.5 | 66.5 | 70.3 | 49.9 |

|

Policy, Regulatory, Communications and Portfolio Integration |

2.4 |

3.9 | 3.9 | 4.5 | 12.4 | |

|

Pensions under the RCMP Contribution Act |

23.6 | 20.4 | 23.0 | 23.0 | 19.6 | 19.6 |

|

To compensate members of the RCMP for injuries received in the performance of duty |

39.1 | 55.1 | 55.8 | 55.8 | 65.0 | 62.0 |

|

Payments in nature of Workers’ Compensation, to survivors of members of the Force |

1.4 | 2.0 | 1.5 | 1.5 | 2.1 | 2.1 |

|

Pensions to families of members of the RCMP who have lost their lives while on duty |

0.1 | 0.1 | 0.1 | 0.1 | 0.1 | 0.1 |

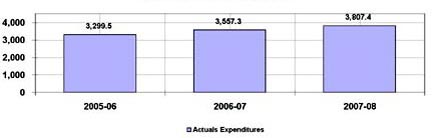

| Total | 3,299.5 |

3,557.3 | 3,771.2 | 3,975.4 | 4,253.6 | 3,807.4 |

| Less: Non-Respendable Revenue | 107.2 | 99.3 | N/A | 107.5 | N/A | 109.5 |

|

Plus: Cost of services received without charge |

201.9 | 221.5 | N/A | 209.2 | N/A | 215.0 |

| Net Cost of Department | 3,394.2 | 3,679.5 | 3,771.2 | 4,077.1 | 4,253.6 | 3,912.9 |

| Full Time Equivalents | 23,578.8 | 24,786.4 | N/A | 27,669.0 | N/A | 26,299.0 |

Total Gross Expenditures ($ millions)

Table 2: Voted and Statutory Items

| Financial Requirements by Authority ($ millions) | ||||

|

Vote |

2007-2008 | |||

|

Main Estimates

|

Planned Spending

|

Total Authorities

|

Actual

|

|

|

Royal Canadian Mounted Police Law Enforcement Program

|

||||

|

45 Operating expenditures

|

1,259.0 | 1,313.0 | 1,990.2 | 1,769.9 |

|

50 Capital expenditures

|

197.9 | 217.0 | 328.5 | 233.7 |

|

55 Grants and Contributions

|

43.7 | 43.7 | 82.0 | 77.5 |

|

(S) Pensions and other employee benefits – Members of the Force

|

288.6 | 288.6 | 283.2 | 283.2 |

|

(S) Contributions to employee benefit plans

|

51.1 | 51.1 | 63.3 | 63.3 |

|

(S) Pensions under the Royal Canadian Mounted Police Pension Continuation Act

|

23.0 | 23.0 | 19.6 | 19.6 |

| Total Department | 1,863.3 | 1,936.4 | 2,766.8 | 2,447.2 |

|

Note: Total authorities are main estimates plus supplementary estimates plus other authorities. Due to rounding, figures may not add to totals shown. In addition, $11.9 million was available from proceeds of disposal of surplus Crown Assets, of which $7.9 million was spent. The balance will be available as spending authority in 2008-2009. Numbers listed above do not include refunds of amounts credited to revenues in previous years ($662,092). |

||||

Table 13: Financial Statements

Financial Statements

(Unaudited)

of

ROYAL CANADIAN MOUNTED POLICE

For the year ended

March 31, 2008

STATEMENT OF MANAGEMENT RESPONSIBILITY

Responsibility for the integrity and objectivity of the accompanying financial statements for the year ended March 31, 2008 and all information contained in these statements rests with the management of the Royal Canadian Mounted Police (RCMP). These financial statements have been prepared by management in accordance with Treasury Board of Canada Secretariat (TBS) accounting policies which are consistent with Canadian generally accepted accounting principles for the public sector.

Management is responsible for the integrity and objectivity of the information in these financial statements. Some of the information in the financial statements is based on management’s best estimates and judgment and gives due consideration to materiality. To fulfill its accounting and reporting responsibilities, management maintains a set of accounts that provides a centralized record of the RCMP’s financial transactions. Financial information submitted to the Public Accounts of Canada and included in the RCMP’s Departmental Performance Report is consistent with these financial statements.

Management maintains a system of financial management and internal control designed to provide reasonable assurance that financial information is reliable, that assets are safeguarded and that transactions are in accordance with the Financial Administration Act, are executed in accordance with prescribed regulations, within Parliamentary authorities and are properly recorded to maintain accountability of Government funds. Management also seeks to ensure the objectivity and integrity of data in its financial statements by careful selection, training and development of qualified staff, by organizational arrangements that provide appropriate divisions of responsibility and by communication programs aimed at ensuring that regulations, policies, standards and managerial authorities are understood throughout the RCMP.

The financial statements of the RCMP have not been audited.

| William J.S. Elliott, Commissioner | Alain P. S�guin, Chief Financial and Administrative Officer |

Ottawa, Canada

August 5, 2008

Statement of Operations (unaudited)

For the year ended March 31, 2008

(in thousands of dollars)

| 2008 | 2007 | |

| EXPENSES (note 4) | ||

| Community, Contract and Aboriginal Policing | 2,386,135 | 2,245,564 |

| Federal and International Policing | 691,887 | 648,497 |

| Technical Policing Operations | 220,629 | 204,446 |

| National Police Services | 197,752 | 183,421 |

| Protective Policing Services | 146,484 | 116,024 |

| Criminal Intelligence Operations | 94,573 | 85,920 |

| Policing Support Services | 89,259 | 85,742 |

| Registration, Licensing and Supporting Infrastructure – Firearms | 49,135 | 84,192 |

| Policy, Regulatory, Communication and Portfolio Integration – Firearms | 13,009 | 2,604 |

| Other Activities | 83,821 | 77,627 |

| Total expenses | 3,972,684 | 3,734,037 |

| REVENUES (note 5) | ||

| Community, Contract and Aboriginal Policing |

1,386,391

|

1,347,642

|

| National Police Services |

14,688

|

15,545

|

| Other Activities |

42,266

|

34,569

|

| Total revenues |

1,443,345

|

1,397,756

|

| NET COST OF OPERATIONS |

2,529,339

|

2,336,281

|

| The accompanying notes form an integral part of these financial statements. | ||

Statement of Financial Position (unaudited)

For the year ended March 31, 2008

(in thousands of dollars)

| 2008 | 2007 | |

| ASSETS | ||

| Financial assets | ||

| Accounts receivables and advances (Note 6) | 570,860 | 364,510 |

|

Total financial assets

|

570,860 | 364,510 |

| Non-financial assets | ||

| Inventory | 44,133 | 36,917 |

| Tangible capital assets (Note 7) | 1,160,654 | 1,103,518 |

|

Total non-financial assets

|

1,204,787 | 1,140,435 |

| Total | 1,775,647 | 1,504,945 |

| Liabilities and Equity of Canada | ||

| LIABILITIES | ||

| Accounts payable and accrued liabilities (Note 8) | 364,199 | 307,983 |

| Vacation pay and compensatory leave | 191,138 | 185,431 |

| RCMP Pension Accounts (Note 9) | 12,052,621 | 11,703,416 |

| Deferred revenue (Note 10) | 110,350 | 103,753 |

| Employee severance benefits (Note 11) | 461,683 | 439,453 |

| Other liabilities (Note 12) | 9,242 | 8,419 |

|

Total liabilities

|

13,189,233 | 12,748,455 |

| Equity of Canada | (11,413,586) | (11,243,510) |

| Total | 1,775,647 | 1,504,945 |

| Contingent liabilities (Note 13) | ||

| Contractual obligations (Note 14) | ||

| The accompanying notes form an integral part of these financial statements. | ||

Statement of Equity (unaudited)

For the year ended March 31, 2008

(in thousands of dollars)

| 2008 | 2007 | |

| Equity of Canada, beginning of year | 11,243,510 | 10,693,793 |

| Net cost of operations | 2,529,339 | 2,336,281 |

| Current year appropriations used (Note 3) | (2,455,813) | (2,297,710) |

| Revenue not available for spending | 96,719 | 124,488 |

| Refund of prior year expenditures | 8,531 | 7,737 |

| Change in net position in the Consolidated Revenue Fund (Note 3) | 206,315 | 600,376 |

| Services received without charged from Other government departments (Note 15) | (215,015) | (221,455) |

| Equity of Canada, end of year | 11,413,586 | 11,243,510 |

| The accompanying notes form an integral part of these financial statements. | ||

Statement of Cash Flow (unaudited)

For the year ended March 31, 2008

(in thousands of dollars)

| 2008 | 2007 | |

| OPERATING ACTIVITIES | ||

| Net Cost of Operations | 2,529,339 | 2,336,281 |

| Non-cash items | ||

|

Amortization of tangible capital assets

|

(136,892) | (125,580) |

|

Loss on disposal, write-off and adjustments in tangible capital assets

|

(8,593) | (15,976) |

|

Services received without charge from other government departments

|

(215,015) | (221,455) |

| Variations in Financial Position | ||

|

Increase (decrease) in financial assets

|

206,350 | (148,315) |

|

Increase (decrease) in inventory

|

7,216 | (1,010) |

|

Decrease in prepaid expenses

|

– | (831) |

|

Increase in liabilities

|

(440,778) | (465,100) |

| Cash used by operating activities | 1,941,627 | 1,358,014 |

| CAPITAL INVESTMENT ACTIVITIES | ||

|

Acquisitions of tangible capital assets

|

206,853 | 211,174 |

|

Proceeds from disposal or transfer of tangible capital assets

|

(4,232) | (4,079) |

| Cash used by capital investment activities | 202,621 | 207,095 |

| FINANCING ACTIVITIES | ||

| Net Cash provided by Government of Canada | (2,144,248) | (1,565,109) |

| The accompanying notes form an integral part of these financial statements. | ||

ROYAL CANADIAN MOUNTED POLICE

Notes for Financial Statements (Unaudited)

For the year ended March 31, 2008

1. Authority and Mandate

The Royal Canadian Mounted Police (RCMP) is Canada’s national police service and an agency of Public Safety Canada.

The RCMP mandate is based on the authority and responsibility assigned under section 18 of the Royal Canadian Mounted Police Act. The mandate of the RCMP is to enforce laws, prevent crime and maintain peace, order and security. Ten program activities highlight our Program Activity Architecture (PAA). These include:

- Community, Contract and Aboriginal Policing

Contributes to Safe Homes and Safe Communities by providing police services to diverse communities in eight provinces (with the exception of Ontario and Quebec) and three territories through cost-shared policing service agreements with federal, provincial, territorial, municipal and Aboriginal governments.

- Federal and International Operations

Provides policing, law enforcement, investigative and protective services to the federal government, its departments and agencies and to Canadians.

- Technical Policing Operations

Provides policy, advice and management to predict, research, develop and ensure the availability of technical tools and expertise to enable front line members and partners to prevent and investigate crime and enforce the law, protect against terrorism and operate in a safe and secure environment.

- National Police Services

Contributes to Safe Homes and Safe Communities for Canadians through the acquisition, analysis, dissemination and warehousing of law enforcement-specific applications of science and technology to all accredited Canadian law enforcement agencies.

- Protective Policing Services

Directs the planning, implementation, administration and monitoring of the RCMP National Protective Security Program. This includes the protection of dignitaries, the security of major events and special initiatives including Prime Minister-led summits of an international nature.

- Criminal Intelligence Operations

A national program for the management of criminal information and intelligence in the detection and prevention of crime of an organized, serious or national security nature in Canada or internationally as it affects Canada.

- Policing Support Services

Providing services in support of the RCMP’s role as a police organization.

- Registration, Licencing and Supporting Infrastructure – Firearms

Delivery of licencing activities through federal Chief Firearms Officers (CFO) operations, arrangements with other federal government departments and the management of provincial CFO roles and relationships; registration of firearms in the Canadian Firearms Registry (CFR) and support to Public Agencies through licencing and registration activities; operation of the Central Processing Site and the 1-800 call centre; maintenance and analysis of program performance data and management of the Program's information technology infrastructure and its interface with other databases.

- Policy, Regulatory, Communication and Portfolio Integration – Firearms

Activities to support the Commissioner as deputy head of the department; Chief Operating Officer activities to support federal Chief Firearms Officers (CFO), licencing, registration and public agencies and in the management of federal-provincial/CFO roles and relationships. Human Resources Management services of the department including compliance with Central Agencies requirements; and Finance and Administration activities of the department including compliance with Central Agencies on financial and administrative issues.

- Corporate Infrastructure

Includes the vital administrative services required for an organization to operate effectively. The costs associated with this activity are distributed among the remaining program activities.

2. Summary of Significant Accounting Policies

The financial statements have been prepared in accordance with TBS accounting policies which are consistent with Canadian generally accepted accounting principles for the public sector.

(a) The RCMP is primarily financed by the Government of Canada through Parliamentary appropriations. Appropriations provided to the department do not parallel financial reporting according to generally accepted accounting principles since appropriations are primarily based on cash flow requirements. Consequently, items recognized in the statement of operations and in the statement of financial position are not necessarily the same as those provided through appropriations from Parliament. Note 3 provides a high-level reconciliation between the bases of reporting.

(b) The department operates within the Consolidated Revenue Fund (CRF), which is administered by the Receiver General for Canada. All cash received by the RCMP is deposited to the CRF and all cash disbursements made by the RCMP are paid from the CRF. The net cash provided by Government is the difference between all cash receipts and all cash disbursements including transactions between departments of the federal government.

(c) Change in net position in the Consolidated Revenue Fund is the difference between the net cash provided by Government and appropriations used in a year, excluding the amount of non respendable revenue recorded by the department. It results from timing differences between when a transaction affects appropriations and when it is processed through the CRF.

(d) Revenues are accounted for in the period in which the underlying transactions or events occurred that gave rise to the revenues. Revenues that have been received but not yet earned or not spent in accordance with any external restrictions are recorded as deferred revenues.

(e) Expenses are recorded when the underlying transaction or expense occurred subject to the following:

- Grants are recognized in the year in which payment is due or in which the recipient has met the eligibility criteria.

- Contributions are recognized in the year in which the recipient has met the eligibility criteria or fulfilled the terms of a contractual transfer agreement.

- Vacation pay and compensatory leave are expensed as the benefits accrue to employees under their respective terms of employment.

- Services provided without charge by other government departments for accommodation, the employer’s contribution to the health and dental insurance plans, Worker’s Compensation and legal services are recorded as operating expenses at their estimated cost.

(f) Employee future benefits:

- Pension benefits for Public Service employees: Eligible employees participate in the Public Service Pension Plan, a multi-employer Plan administered by the Government of Canada. The department’s contributions to the Plan are charged to expenses in the year incurred and represent the total departmental obligation to the Plan. Current legislation does not require the department to make contributions for any actuarial deficiencies of the Plan.

- Pension benefits for RCMP members: The Government of Canada sponsors a variety of employee future benefits such as pension plans and disability benefits, which cover members of the RCMP. The department administers the pension benefits for members of the RCMP. The actuarial liability and related disclosures for these future benefits are presented in the financial statements of the Government of Canada. This differs from the accounting and disclosures of future benefits for RCMP presented in these financial statements whereby pension expense corresponds to the department’s annual contributions toward the cost of current service. In addition to its regular contributions, current legislation also requires the department to make contributions for actuarial deficiencies in the RCMP Pension Plan. These contributions are expensed in the year they are credited to the Plan. This accounting treatment corresponds to the funding provided to departments through Parliamentary appropriations.

- Severance benefits: Employees and RCMP members are entitled to severance benefits under labor contracts or conditions of employment. These benefits are accrued as employees render the services necessary to earn them. The obligation relating to the benefits earned by employees and RCMP members is calculated using information derived from the results of the actuarially determined liability for employee severance benefits for the Government as a whole.

(g) Receivables from external parties are stated at amounts expected to be ultimately realized; a provision is made for external receivables where recovery is considered uncertain.

(h) Contingent liabilities – Contingent liabilities are potential liabilities which may become actual liabilities when one or more future events occur or fail to occur. To the extent that the future event is likely to occur or fail to occur and a reasonable estimate of the loss can be made, an estimated liability is accrued and an expense recorded. If the likelihood is not determinable or an amount cannot be reasonably estimated, the contingency is disclosed in the notes to the financial statements.

(i) Environmental liabilities – Environmental liabilities reflect the estimated costs related to the management and remediation of environmentally contaminated sites. Based on management’s best estimates, a liability is accrued and an expense recorded when the contamination occurs or when the department becomes aware of the contamination and is obligated, or is likely to be obligated to incur such costs. If the likelihood of the department’s obligation to incur these costs is not determinable, or if an amount cannot be reasonably estimated, the costs are disclosed as contingent liabilities in the notes to the financial statements.

(j) Inventories – Inventories consist of parts, material and supplies held for future program delivery and not intended for re-sale. They are valued at cost. If they no longer have service potential, they are valued at the lower of cost or net realizable value.

(k) Foreign currency transactions – Transactions involving foreign currencies are translated into Canadian dollar equivalents using rates of exchange in effect at the time of those transactions. Monetary assets and liabilities denominated in foreign currencies are translated using exchange rates in effect on March 31st. Gains resulting from foreign currency transactions are included under “Other revenues” in note 5. Losses are included under “Other operating expenses” in note 4.

(l) Tangible capital assets – All tangible capital assets and leasehold improvements having an initial cost of $10,000 or more are recorded at their acquisition cost. Capital assets do not include intangibles, works of art and historical treasures that have cultural, aesthetic or historical value, assets located on Indian Reserves and museum collections.

Amortization of capital assets is done on a straight-line basis over the estimated useful life of the capital asset as follows:

| Asset Class | Sub-asset Class | Amortization Period |

| Buildings | 20 to 30 years | |

| Works and Infrastructures | 20 years | |

| Machinery and Equipment | Machinery and Equipment | 5 to 15 years |

| Informatics – Hardware | 4 to 7 years | |

| Informatics – Software | 3 to 7 years | |

| Vehicles | Marine Transportation | 10 to 15 years |

| Air Transportation | 10 years | |

| Land Transportation (non-military) | 3 to 5 years | |

| Land Transportation (military) | 10 years | |

| Leasehold Improvements | Term of lease |

In the normal course of business, the RCMP constructs buildings and other assets as well as develops software. The associated costs are accumulated in Assets under Construction (AUC) until the asset is in use. No amortization is taken until the asset is put in use.

(m) Intellectual property such as licences, patents and copyrights are expensed in the period in which they are incurred.

(n) Measurement uncertainty – The preparation of these financial statements in accordance with TBS accounting policies which are consistent with Canadian generally accepted accounting principles for the public sector requires management to make estimates and assumptions that affect the reported amounts of assets, liabilities, revenues and expenses reported in the financial

statements. At the time of preparation of these statements, management believes the estimates and assumptions to be reasonable. The most significant items where estimates are used are contingent liabilities, environmental liabilities, the liability for employee severance benefits and the useful life of tangible capital assets. Actual results could significantly differ from those

estimated. Management’s estimates are reviewed periodically and, as adjustments become necessary, they are recorded in the financial statements in the year they become known.

3. Parliamentary Appropriations

The RCMP receives most of its funding through annual Parliamentary appropriations. Items recognized in the Statement of Operations and the Statement of Financial Position in one year may be funded through Parliamentary appropriations in prior, current or future years. Accordingly, the RCMP has different net results of operations for the year on a government funding basis than on an accrual accounting basis. The differences are reconciled in the following tables:

(a) Reconciliation of net cost of operations to current year appropriations used

|

|

2008 | 2007 |

|

(in thousands of dollars) |

||

| NET COST OF OPERATIONS | 2,529,339 | 2,336,281 |

| Adjustments for items affecting net cost of operations but not affecting appropriations | ||

| Add (Less): | ||

|

Services received without charge from other government departments

|

(215,015) | (221,455) |

|

Revenue not available for spending

|

96,719 | 124,488 |

|

Amortization of tangible capital assets

|

(136,892) | (125,580) |

|

Refunds of prior year expenditures

|

8,531 | 7,737 |

|

Increase in liability for severance benefits

|

(22,230) | (14,709) |

|

Transfer cost to assets under construction

|

122,808 | 128,072 |

|

Increase in liability for vacation pay and compensatory leave

|

(9,916) | (2,043) |

|

Increase in liability for contaminated sites

|

(524) | (1,203) |

|

Net loss and write-off on disposal of tangible capital assets

|

(12,249) | (15,921) |

|

Other

|

(7,627) | (1,282) |

| 2,352,944 | 2,214,385 | |

| Adjustments for items not affecting net cost of operations but affecting Appropriations | ||

|

Add (Less): |

||

|

Acquisitions of tangible capital assets

|

86,764 | 78,207 |

|

Accountable advances

|

(8) | 173 |

|

Inventory purchased

|

16,113 | 5,776 |

|

Prepaid expenses

|

– | (831) |

| Current year Appropriations Used | 2,455,813 | 2,297,710 |

(b) Appropriations provided and used

|

Appropriations Provided |

||

|

|

2008 | 2007 |

|

(in thousands of dollars) |

||

| Operating expenditures | 1,990,204 | 1,721,843 |

| Capital expenditures | 328,460 | 292,555 |

| Grants and Contributions | 81,956 | 74,846 |

| Statutory amounts | 378,782 | 374,004 |

| Less: | ||

| Appropriations available for future years | (4,060) | (3,543) |

| Lapsed appropriations – Operating | (319,529) | (161,995) |

| Current year appropriation used | 2,455,813 | 2,297,710 |

(c) Reconciliation of net cash provided by Government to current year appropriations used

|

|

2008 | 2007 |

|

(in thousands of dollars) |

||

| Net cash provided by Government |

2,144,248

|

1,565,109 |

| Revenue not available for spending |

96,719

|

124,488 |

| Refund of prior year expenditures | 8,531 | 7,737 |

| 2,249,498 | 1,697,334 | |

| Change in net position in the Consolidated Revenue Fund | ||

|

Variation in accounts receivable and advances

|

(206,350) | 148,315 |

|

Variation in inventory

|

(7,216) | 1,010 |

|

Variation in accounts payable and accrued liabilities

|

56,216 | 37,681 |

|

Variation in prepaid expenses

|

– | 831 |

|

Variation in pension liabilities

|

349,205 | 380,602 |

|

Variation in deferred revenue

|

6,597 | 28,225 |

|

Variation in liabilities

|

823 | 1,840 |

|

Other adjustments

|

7,040 | 1,872 |

| 206,315 | 600,376 | |

| Current year appropriations used | 2,455,813 | 2,297,710 |

4. Expenses

The following table presents details of expenses by category:

|

|

2008 | 2007 | |

|

(in thousands of dollars) |

|||

| Operating expenses: | Salaries and employee benefits | 2,609,985 | 2,471,754 |

| Professional & special services | 326,604 | 305,489 | |

| Travel & relocation | 167,412 | 152,530 | |

| Amortization | 136,892 | 125,580 | |

| Accommodation | 118,695 | 108,893 | |

| Utilities, material & supplies | 115,521 | 105,260 | |

| Purchased repairs & maintenance | 99,639 | 88,732 | |

| Telecommunications | 46,926 | 44,457 | |

| Rentals | 27,028 | 26,013 | |

| Provision for severance benefits | 22,230 | 14,708 | |

| Loss on disposal and write-off | 12,779 | 16,157 | |

| Information | 5,558 | 3,958 | |

| Other operating expenses |

191,452 | 186,605 | |

| Subtotal | 3,880,721 | 3,650,136 | |

| Transfer payments: | Compensatory grants to individuals | 78,696 | 72,261 |

| Transfers to other levels of Governments | 12,470 | 11,076 | |

| Payments to or on behalf of First Nations | 198 | 178 | |

| Other | 599 | 386 | |

| Subtotal | 91,963 | 83,901 | |

| TOTAL EXPENSES | 3,972,684 | 3,734,037 | |

5. Revenues

The following table presents details of revenues by category:

|

|

2008 | 2007 |

|

(in thousands of dollars) |

||

| Policing services | 1,428,039 | 1,381,340 |

| Firearms registration fees | 7,742 | 6,245 |

| Other revenues | 7,564 | 10,171 |

| TOTAL REVENUES | 1,443,345 | 1,397,756 |

6. Accounts Receivables and Advances

|

|

2008 | 2007 |

|

(in thousands of dollars) |

||

| Receivables from other departments and agencies | 228,326 | 23,280 |

| Receivables from external parties | 332,259 | 331,168 |

| 560,585 | 354,448 | |

| Less: Allowance for doubtful accounts on external receivables | (293) | (293) |

| Net receivables | 560,292 | 354,155 |

| Temporary advances | 8,062 | 7,815 |

| Standing advances | 2,506 | 2,540 |

| Total Advances | 10,568 | 10,355 |

| Total accounts receivable and advances | 570,860 | 364,510 |

7. Tangible Capital Assets

|

Cost |

||||

| Opening Balance |

Acquisitions and adjustments | Disposal and Write-offs | Closing Balance | |

| Land | 42,537 | 1,696 | 45 | 44,188 |

| Buildings | 763,950 | 30,773 | 1,783 | 792,940 |

| Works & Infrastructure | 13,247 | 23,280 | – | 36,527 |

| Machinery & Equipment | 524,861 | 20,968 | 466 | 545,363 |

| Vehicles | 461,272 | 66,955 | 41,675 | 486,552 |

| Leasehold Improvements | 12,254 | 5,915 | – | 18,169 |

| Assets Under Construction | 185,029 | 57,266 | 3,740 | 238,555 |

| Total | 2,003,150 | 206,853 | 47,709 | 2,162,294 |

|

Accumulated Amortization |

||||

| Opening Balance |

Amortization and Adjustments | Disposal and Write-offs | Closing Balance | |

| Land | ||||

| Buildings | 352,842 | 32,029 | 1,407 | 383,464 |

| Works & Infrastructure | 1,330 | 1,574 | – | 2,904 |

| Machinery & Equipment | 309,510 | 50,108 | 452 | 359,166 |

| Vehicles | 232,863 | 51,270 | 33,025 | 251,108 |

| Leasehold Improvements | 3,087 | 1,911 | – | 4,998 |

| Assets Under Construction | – | – | – | – |

| Total | 899,632 | 136,892 | 34,884 | 1,001,640 |

Amortization expense for the year ended March 31, 2008 is $ 136,892 (2007 – $ 125,580)

|

Net book value |

||

|

2008

|

2007

|

|

| Land |

44,188

|

42,537

|

| Buildings |

409,476

|

411,108

|

| Works and Infrastructure |

33,623

|

11,917

|

| Machinery and Equipment |

186,197

|

215,351

|

| Vehicles |

235,444

|

228,409

|

| Leasehold Improvements |

13,171

|

9,167

|

| Assets under Construction |

238,555

|

185,029

|

|

Total |

1,160,654

|

1,103,518

|

8. Accounts Payable and Accrued Liabilities

The following table presents the accounts payable and other accrued liabilities:

|

|

2008 | 2007 |

|

(in thousands of dollars) |

||

| Payables to other government departments | 29,241 | 21,769 |

| Payables to external parties | 272,561 | 243,984 |

| Accrued salaries and wages | 27,893 | 20,444 |

| Other | 34,504 | 21,786 |

| Total accounts payable and accrued liabilities | 364,199 | 307,983 |

9. RCMP Pension Accounts

The department maintains accounts to record the transactions pertaining to the RCMP Pension Plan, which comprises the RCMP Superannuation Account, the RCMP Pension Fund Account, the Retirement Compensation Arrangement Account and the Dependents Pension Fund Account. These accounts record transactions such as contributions, benefit payments, interest credits, refundable taxes and actuarial debit and credit funding adjustments resulting from triennial reviews and transfers to the Public Sector Investment Board.

The value of the liabilities reported in these financial statements for the RCMP Pension Plan accounts do not reflect the actuarial value of these liabilities determined by the Chief Actuary of the Office of the Superintendent of Financial Institutions nor the investments that are held by the Public Sector Investment Board.

The following table provides details of the RCMP Pension Plan Pension Accounts:

| 2008 | 2007 | |

|

(in thousands of dollars) |

||

| RCMP Superannuation Account | 11,989,180 | 11,640,609 |

| RCMP Pension Fund Account | 11,187 | 11,140 |

| Retirement Compensation Arrangement Account * | 23,717 | 22,258 |

| Dependents Pension Fund Account | 28,537 | 29,409 |

| Total |

12,052,621

|

11,703,416

|

* The Retirement Compensation Arrangement (RCA) account records transactions for pension benefits that are provided in excess of those permitted under the Income Tax Act. The RCA is registered with Canada Revenue Agency (CRA) and a transfer is made annually between the RCA Account and CRA to either remit a 50-percent refundable tax in respect of the net contributions and interest credits or to be credited a reimbursement based on the net benefit payments. As at March 31, 2008 the total refundable tax transferred (RCMP only) amounts to $23 million ($22 million in 2007).

10. Deferred Revenue

|

Deferred revenue – contract policing arrangements on tangible capital assets

|

||

| 2008 | 2007 | |

|

(in thousands of dollars) |

||

| Beginning of the year | 103,184 | 75,084 |

| Increase in net book value of contract policing capital assets | 6,275 | 28,100 |

| Revenue recognized | – | – |

| Deferred revenue – end of year | 109,459 | 103,184 |

|

Donation and bequest

|

||

| 2008 | 2007 | |

|

(in thousands of dollars) |

||

| Beginning of the year | 417 | 444 |

| Contributions received | 396 | 128 |

| Revenue recognized | (74) | (155) |

| Deferred revenue – end of year | 739 | 417 |

|

Registration fees

|

||

| 2008 | 2007 | |

|

(in thousands of dollars) |

||

| Beginning of the year | 152 | – |

| Registration fees received on application request | – | 152 |

| Revenue recognized | – | – |

| Deferred revenue – end of year | 152 | 152 |

| Total deferred revenue | 110,350 | 103,753 |

Deferred revenue consists of three categories: deferred revenue for contract policing arrangements on tangible capital assets, deferred revenue for donation and bequest accounts and deferred revenue for registration fees. Deferred revenue for contract policing arrangements on tangible capital assets represents the balance of revenue received at the time of acquisition of tangible capital assets owned by RCMP and dedicated for usage to meet contractual obligations over the life of the asset. The deferred revenue is earned on the same basis as the amortization of the corresponding capital asset. Deferred revenue for donation and bequest accounts represents the balance of contributions received for various purposes. They are recognized as revenue when the funds are expended for the specified purposes. Deferred revenue for registration fees represents the application fee received from clients where the application processing has not reached a sufficient stage to warrant recognizing revenue. They are recognized as revenue when the eligibility checks point of application is processed.

11. Employee benefits

(a) Pension benefits (Public Service employees): The department’s public service employees participate in the Public Service Pension Plan, which is sponsored and administered by the Government of Canada. Pension benefits accrue up to a maximum period of 35 years at a rate of 2 percent per year of pensionable service, times the average of the best five consecutive years of earnings. The benefits are integrated with Canada/Qu�bec Pension Plans benefits and they are indexed to inflation.

Both the employees and the department contribute to the cost of the Plan. The 2007-2008 expense amounts to $46 millions ($44 million in 2006-07), which represents approximately 2.1 (2.2 in 2006-07) times the contributions by employees. The department’s responsibility with regard to the Plan is limited to its contributions. Actuarial surpluses or deficiencies are recognized in the financial statements of the Government of Canada, as the Plan’s sponsor.

(b) Pension benefits (RCMP members): The department’s regular and civilian members participate in the RCMP Pension Plan, which is sponsored by the Government of Canada and is administered by the RCMP. Pension benefits accrue up to a maximum period of 35 years at a rate of 2 percent per year of pensionable service, times the average of the best five consecutive years of earnings. The benefits are integrated with Canada/Qu�bec Pension Plans benefits and they are indexed to inflation.

Both the members and the department contribute to the cost of the Plan. The 2007-2008 expense amounts to $224 million ($213 million in 2006-07), which represents approximately 2.4 times the contributions by members (2.5 in 2006-07). The RCMP is responsible for the administration of the Plan including determining eligibility for benefits, calculating and paying benefits, developing legislation and related policies and providing information to Plan members. The actuarial liability and actuarial surpluses or deficiencies are recognized in the financial statements of the Government of Canada, as the Plan’s sponsor.

(c) Severance benefits: The department provides severance benefits to its employees and RCMP members based on eligibility, years of service and final salary. These severance benefits are not pre-funded. Benefits will be paid from future appropriations. Information about the severance benefits, measured as at March 31, is as follows:

| 2008 | 2007 | |

| (in thousands of dollars) | ||

| Accrued benefit obligation, beginning of year | 439,453 | 424,744 |

| Expense for the year | 55,679 | 46,952 |

| Benefits paid during the year | (33,449) | (32,243) |

| Accrued benefit obligation, end of year | 461,683 | 439,453 |

12. Other liabilities

| 2008 | 2007 | |

|

(in thousands of dollars) |

||

| Benefit Trust Fund | 2,401 | 2,312 |

| Contractor Securities | 406 | – |

| Environmental Liabilities | 4,276 | 3,752 |

| Other | 2,159 | 2,355 |

| Total | 9,242 | 8,419 |

Benefit Trust Fund: This account was established by section 23 of the Royal Canadian Mounted Police Act, to record moneys received by personnel of the Royal Canadian Mounted Police, in connection with the performance of duties, over and above their pay and allowances. Receipts of $178,240 ($219,719 in 2007) were received in the year and payments of $88,880 ($136,650 in 2007) were issued. The fund is use for (i) the benefit of members, former members and their dependants; (ii) as a reward, grant or compensation to any person who assists the RCMP in the performance of its duties in any case where the Minister is of the opinion that such person is deserving of recognition for the services rendered; (iii) as a reward to any person appointed or employed under the authority of the RCMP Act for good conduct or meritorious service and (iv) for such other purposes that would benefit the RCMP as the Minister may direct.

13. Contingent Liabilities

(a) Contaminated sites: Liabilities are accrued to record the estimated costs related to the management and remediation of contaminated sites where the department is obligated or likely to be obligated to incur such costs. The department has identified approximately 21 sites (17 sites in 2007) where such action is possible and for which a liability of $4,275,715 ($3,752,007 in 2007) has been recorded. The department’s ongoing efforts to assess contaminated sites may result in additional environmental liabilities related to newly identified sites, or changes in the assessments or intended use of existing sites. These liabilities will be accrued by the department in the year in which they become known.

(b) Claims and litigation: Claims have been made against the department in the normal course of operations. Legal proceedings for claims totaling approximately $74 million ($84 millions in 2007) were still pending at March 31, 2008. Some of these potential liabilities may become actual liabilities when one or more future events occur or fail to occur. To the extent that the future event is likely to occur or fail to occur and a reasonable estimate of the loss can be made, an estimated liability is accrued and an expense recorded in the financial statements.

(c) Pension litigation: The Public Sector Pension Investment Board Act, which received Royal Assent in September 1999, amended the RCMPSA to enable the Federal government to deal with excess amounts in the RCMP Superannuation Account and the RCMP Pension Fund. The legal validity of these provisions has been challenged in the courts. On November 20, 2007, the court has rendered its decision and has dismissed all the claims of the plaintiffs. The plaintiffs are currently appealing this decision to the Ontario Court of Appeal.

14. Contractual Obligations

The nature of the RCMP’s activities can result in some large multi-year contracts and obligation whereby the RCMP will be obligated to make future payments when the services/goods are received. Significant contractual obligations that can be reasonably estimated are summarized as follows:

| (in thousands of dollars) |

2009 | 2010 | 2011 | 2012 | 2013 and thereafter | Total |

| Services agreement | 64,000 | 41,000 | 9,000 | – | – | 114,000 |

| Total | 64,000 | 41,000 | 9,000 | – | – | 114,000 |

15. Related Party Transactions

The RCMP is related as a result of common ownership to all Government of Canada departments, agencies and Crown corporations. The RCMP enters into transactions with these entities in the normal course of business and on normal trade terms. Also, during the year the RCMP received without charge from other departments, accommodation, the employer’s contribution to the health and dental insurance plans, worker’s compensation and legal services. These services without charge have been recognized in the department’s Statement of Operations as follows:

| Services received without charge from other government departments |

2008 | 2007 |

|

(in thousands of dollars) |

||

| Accommodation provided by Public Works and Government Services | 64,210 | 60,579 |

| Contributions covering employer`s share of employees` Insurance premiums and expenditures by TBS | 147,525 | 158,070 |

| Workers’ compensation cost provided by Human Resources Canada | 378 | 381 |

| Legal services provided by Department of Justice | 2,902 | 2,425 |

| Total | 215,015 | 221,455 |

The Government has structured some of its administrative activities for efficiency and cost-effectiveness purposes so that one department performs these on behalf of all without charge. The costs of these services, which include payroll and cheque issuance services provided by Public Works and Government Services Canada, are not included as an expense in the department’s Statement of Operations.

16. Comparative information

Comparative figures have been reclassified to conform to the current year’s presentation.