Guide to Interest and Administrative Charges

Hierarchy

1. Date of publication

This guide was published on .

This guide replaces the Treasury Board Guideline on Interest and Administrative Charges dated .

2. Application, purpose and scope

This guide applies to the organizations listed in section 6 of the Policy on Financial Management.

The purpose of this guide is to provide departments with information on charging interest on overdue accounts and levying administrative charges for dishonoured payment instruments.

This guide supports the Interest and Administrative Charges Regulations (the regulations) and the Directive on Public Money and Receivables. This guide complements the regulations and the directive; it does not present new mandatory requirements.

Sections 3 and 4 provide the context that led to the adoption of the regulations and clarify the application of the regulations.

Section 5 and Appendix A provide details on the calculation of interest in accordance with the regulations.

Section 6 provides clarifications on administrative charges to levy when a department receives a dishonoured payment instrument.

Sections 7 and 8 discuss special considerations regarding the application of the regulations including those related to the application of the Low-Value Amounts Regulations.

Section 9 provides information on circumstances where interest or administrative charges may be waived or reduced.

Appendix B provides guidance for the application of the publication requirement under paragraph 8(b) of the regulations.

3. Context

Receivables are an important asset of the Government of Canada, involving billions of dollars and a wide range of transactions. Their management is vital to responsible fiscal management in the federal government.

Among the key management practices for receivables, departments must take appropriate, timely and cost‑effective collection actions to reduce the risk of not collecting debts, as any decision to forego the collection of a debt has a fiscal impact on the federal government. To increase the effectiveness of collection actions, departments apply interest on overdue accounts and administrative charges on dishonoured payment instruments to encourage debtors to pay amounts due promptly.

The application of interest, penalties or charges on overdue accounts must be authorized by an act of Parliament, regulation, order, contract or arrangement. Normally, receivables resulting from taxation and duties have specific legislative and regulatory authorities (for example, Income Tax Act, Customs Act) for the imposition of interest and penalties on overdue amounts owing to the government. For receivables not related to taxes, legislative authority is granted under section 155.1 of the Financial Administration Act (FAA) and requires the payment of interest and administrative charges on amounts owed to the federal government, unless another act of Parliament, regulation, order, contract or arrangement states otherwise.

Section 155.1 of the FAA is made operative through the Interest and Administrative Charges Regulations, which came into effect on April 1, 1996. Since the issuance of the regulations, debtors have an incentive to pay their non‑tax related accounts on time so that debtors, and not general taxpayers, pay the cost of financing the receivables.

4. Application of the regulations

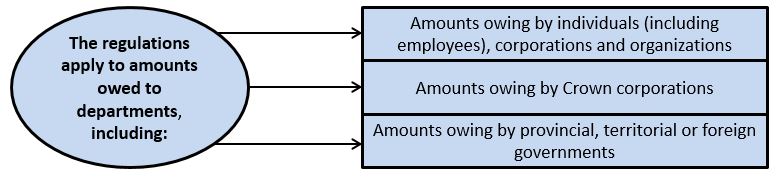

Figure 1 below summarizes the application of the Interest and Administrative Charges Regulations. Explanatory information on this table is provided in subsections 4.1 to 4.3.

Figure 1 - Text version

The regulations apply to amounts owed to departments, including amounts owing by individuals (including employees), corporations and organizations, amounts owing by Crown corporations and amounts owing by provincial, territorial or foreign governments.

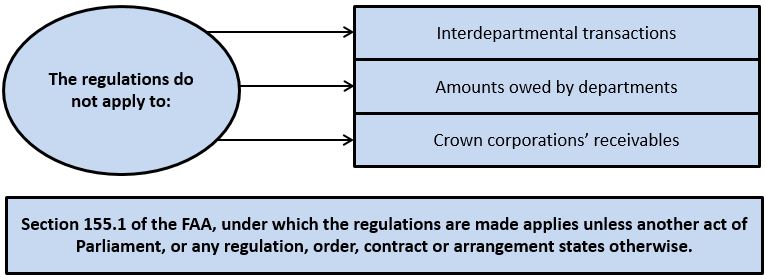

The regulations do not apply to interdepartmental transactions, amounts owed by departments and Crown corporations’ receivables.

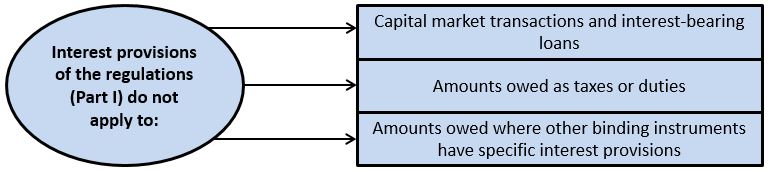

Interest provisions of the regulations (Part I) do not apply to capital market transactions and interest-bearing loans, amounts owed as taxes or duties and amounts owed where other binding instruments have specific interest provisions.

Section 155.1 of the FAA, under which the regulations are made applies unless another act of Parliament, or any regulation, order, contract, or arrangement states otherwise.

4.1 When do the regulations apply?

Figure 2 below summarizes circumstances when the regulations apply.

Figure 2 - Text version

The regulations apply to amounts owed to departments, including amounts owing by individuals (including employees), corporations and organizations, amounts owing by Crown corporations and amounts owing by provincial, territorial or foreign governments.

General: the regulations apply to overdue accounts resulting from amounts owing to departments and where any instrument payable to them is dishonoured. This includes amounts owing by individuals (including employees), corporations and organizations. The following paragraphs provide additional information on the application of the regulations.

The departments to which the regulations apply are those included in the definition of “department” provided in section 2 of the FAA.

Amounts owing by Crown corporations: the regulations apply to amounts owed to a department by a Crown corporation unless another act of Parliament, a regulation, an order, a contract or an arrangement states otherwise.

Amounts owing by provincial, territorial or foreign governments: the regulations also apply to amounts owing by a provincial, territorial or foreign government unless another act of Parliament (that is, the Parliament of Canada), a regulation, an order, a contract or an arrangement states otherwise.

In some instances, an act, a regulation or a policy instrument from another government would preclude the other government from paying interest on its overdue accounts, but that act, regulation or policy instrument would not constitute an act of Parliament or a regulation within the meaning of subsection 155.1(1) of the FAA; therefore, the regulations would still apply.

If departments are uncertain about the application of the regulations to a provincial, territorial or foreign government, they should seek advice from their legal counsel.

When legislation or a contract is silent on charging interest: when another act of Parliament, a regulation, an order, a contract or an arrangement is silent on the subject of payment of interest on overdue accounts or for late payments, the regulations automatically apply.

Debt due to the Crown: interest and administrative charges are debts due to the Crown under subsection 155.1(3) of the FAA. They may be recovered through any collection methods available to departments in their management of receivables.

4.2 When do the regulations not apply?

Figure 3 below summarizes circumstances when the regulations do not apply.

Figure 3 - Text version

The regulations do not apply to interdepartmental transactions, amounts owed by departments and Crown corporations’ receivables.

Section 155.1 of the FAA, under which the regulations are made applies unless another act of Parliament, or any regulation, order, contract, or arrangement states otherwise.

Interdepartmental transactions: the regulations do not apply to interdepartmental receivables. Any amounts owing by another department are not subject to interest and administrative charges.

Amounts owed by departments: the regulations do not apply when a department owes amounts to third parties, such as for the late payment of invoices from suppliers or for the late or non-payment of salaries to employees. Another authority is required for the federal government to pay interest on overdue accounts such as an authority provided under a Treasury Board policy or directive (for example, payment on due date requirements included in the Directive on Payments).

Crown corporations’ receivables: the regulations do not apply to amounts owed to a Crown corporation, as stated in paragraph 3(a) of the regulations.

Other binding instruments state otherwise: under section 155.1 of the FAA, interest and administrative charges are payable in accordance with the regulations except when otherwise provided by, or pursuant to, any other act of Parliament, regulation, order, contract or arrangement. If any of these instruments state that section 155.1 of the FAA or the regulations, in whole or in part, do not apply or explicitly state that no interest or administrative charges are payable, these instruments take precedence over the regulations.

4.3 When should interest not be charged according to the regulations?

Figure 4 below summarizes circumstances when interest provisions of the regulations do not apply.

Figure 4 - Text version

Interest provisions of the regulations (Part I) do not apply to capital market transactions and interest-bearing loans, amounts owed as taxes or duties and amounts owed where other binding instruments have specific interest provisions.

Capital market transactions and interest-bearing loans: the interest provisions of the regulations do not apply to capital market transactions and amounts owed under interest-bearing loans, including hypothecary loans or mortgages.

Note There is an exception for concessionary loans, as described in subsection 7.6 of this guide.

Amounts owed as taxes or duties: amounts owed as taxes or duties have specific legislation and regulations on the application of interest charges.

Amounts owed where other binding instruments have specific interest provisions: the interest provisions of the regulations do not apply to amounts owed where other acts of Parliament, regulations, orders, contracts or arrangements provide for the charging of interest on those amounts.

Administrative charges still apply: although the charging of interest under Part I of the regulations does not apply to the circumstances listed in the previous three paragraphs, any dishonoured instruments used to make a payment or settlement of an amount owed related to these elements are still subject to administrative charges under Part II of the regulations, unless another act of Parliament, regulation, order, contract or arrangement states otherwise.

5. How is interest calculated?

Note Examples of interest calculations in accordance with section 5 of the regulations are provided in Appendix A of this guide. These examples apply in all cases where interest has to be calculated in accordance with the regulations.

General application: under the regulations (subsection 5(1)), when an account is overdue or a payment is late, departments must charge interest compounded monthly at the average bank rate plus 3% from the due date to the day before the date that payment is received.

Partial payment: when a partial payment is received, the period for which interest accrues in relation to that partial payment ends on the day before the day on which the partial payment is received.

Receipt date: the payment’s receipt date is either the day on which the payment is made at a financial institution or when it first arrives in a department. Departments must date-stamp or batch all incoming payments by date received and use that date in calculating any interest due.

Interest rate information: the interest rate used to calculate the interest charge on overdue accounts is available on the Rates for Receiver General payments web page. The interest rate is the same as that used by departments to pay interest on overdue supplier accounts.

Interest accrues until collection or debt deletion: when departments take collection actions to recover a debt, including the use of a set-off, the interest on any overdue account continues to accrue until the debt is collected or, when a debt is not settled in full, remitted or forgiven. This applies even when the probability of recovering a debt and accrued interest is low, for example, when a debtor has declared bankruptcy or ceased operations.

Note The effects of a write-off on the debt and accrued interest are provided in subsection 9.2 of this guide.

5.1 What information should be provided to debtors when charging interest?

Demand for payment information: A demand for payment (for example, invoices, bills or statements) issued to recipients should include information such as the total amount owing, payment terms (payment due date and any conditions of that payment), lists or schedules of applicable fees and rates, and notice that interest will be charged on late payments.

Monthly statements: to ensure the proper application of the interest provisions of the regulations, debtors should receive monthly statements (or a notice informing them of the online availability of their statements) providing the following information:

- the previous balance of amount owing to the department

- the current charges and payment due date related to these charges

- any amount overdue and the interest charged

- the payments received

- the total amount now owing

- a notice that interest is charged on late payments

- an explicit statement that the payment due date for any amounts overdue remains the original due date and not the payment due date for current charges issued on the statement

The above list is not exhaustive; other elements may be added or modified, depending on the status and characteristics of the debtor’s account.

Applicable taxes are included in the amount due: when an account is overdue or a payment is late, interest is charged on the total amount due, including applicable taxes that are included in the amount due.

Sales taxes are not charged to interest and administrative charges: the Goods and Services Tax or Harmonized Sales Tax, the Quebec Sales Tax and provincial sales taxes are not charged to interest and administrative charges imposed under the regulations. Interest and administrative charges amounts must be clearly segregated on the invoice, bill or statement of account.

6. How are administrative charges levied?

General application: departments are to levy administrative charges when an item (for example, a cheque) payable to the federal government is returned as “NSF” (non-sufficient funds) or otherwise dishonoured.

Charges: departments normally use Receiver General concentrator accountsFootnote 1 for deposits, and financial institutions obtain reimbursement for dishonoured items through a charge-back. In such cases, the administrative charge is $15.

When dishonoured items are processed by a financial institution and departments have to issue a payment to reimburse the financial institution because a charge-back is not possible, the administrative charge is $25.

Account monitoring: departments may arrange with a financial institution to monitor the account of a debtor that has tendered a dishonoured item and, once the account contains sufficient funds, to certify the item, return it to the department, or clear the item directly. Departments charge the debtor for account monitoring fees they had to pay to a financial institution in addition to the charges described above.

7. Special considerations

7.1 Overpayments or erroneous payments

General application of interest: in accordance with section 155.1 of the FAA and the regulations, interest is payable to the Crown on any amount owed resulting from an overpayment or an erroneous payment that is not received by the due date.

Example A department paid a supplier twice for the same invoice (a duplicate payment). The amount paid in excess must be collected. The department issues a demand for repayment to the supplier and specifies a due date. Interest will be payable by the supplier if the repayment is not received by the department by the due date specified on the demand.

Repayment arrangement: when an overpayment or erroneous payment occurs, arrangements will be made for repayment and departments will charge interest only when repayment is overdue.

Fraud and other offences: under the regulations, when departments make overpayments or erroneous payments as a result of fraud, falsification, willful misrepresentation or any other offence, these payments will incur interest charges from the date on which the overpayment or erroneous payment is made.

Salary overpayment: interest may be charged on amounts due resulting from overpayments or erroneous payments to employees of salaries, wages, benefits and allowances when a repayment is not received by the due date in the agreed-upon repayment schedule, where one exists. If no repayment schedule exists, then interest accrues as of the due date of the full amount.

Example Interest on salary overpayment could arise when an employee chooses to repay a salary overpayment by cheque instead of by deduction from the payroll system, but the amount is not repaid by the due date.

Negotiation of repayment terms: subject to any legislation, regulation or policy governing programs or departments, deputy heads and departmental officials have complete flexibility in negotiating and setting repayment terms. Under subsection 6(3) of the regulations, interest may be charged on the total amount outstanding and not just on missed or late payments. This application of this flexibility is particularly appropriate when the debt involves an overpayment by a department that was not the result of an error on its part. To charge interest on the total amount outstanding, departmental officials are to include an interest provision in the repayment arrangement.

7.2 Errors by departments and federal government system breakdowns

Errors in processing payments received: the regulations specify that a department must not apply interest or administrative charges when it makes an error that results in interest or administrative charges otherwise applying, for example, if it does not credit the right account, does not deposit or record the payment promptly, attempts to deposit a post-dated cheque early, or holds a cheque until it becomes stale-dated.

Error or delay in establishing amount due: when an error is made, or a delay is caused by a department or an authorized representative in establishing an amount payable, no interest is payable. Proper arrangements with debtors, including repayment schedules or a demand for payment, need to be implemented to accrue and charge interest.

System failure: in addition, no interest is payable when it accrued as a result of a breakdown or other failure in the system or communication links customarily used by the federal government to process payments.

7.3 Small amounts

Exception for small amounts: Paragraph 8(b) of the regulations provides an exception for charging interest that a department may apply regarding an outstanding amount due when:

- the deputy head responsible for the departmental program or service establishes a minimum amount (of an outstanding amount due ) under which a demand for payment (for example, an invoice) would not normally be issued for a period in respect to a program or service.

- the minimum amount established for a program or service and the applicable period (which is normally based on the invoicing cycle) is published on a Government of Canada website.

No interest is payable on an outstanding amount due when the amount is less than the minimum amount set for the purpose of paragraph 8(b) and the above criteria are met.

Establishment of minimum amounts: Several minimum amounts can be established within a department to meet specific program or service operational requirements. A deputy head may also establish a uniform minimum amount threshold for all departmental programs or services.

Authority to establish minimum amounts: The deputy head’s authority to establish minimum amounts for the purpose of paragraph 8(b) does not require a formal delegation of authority in order for other departmental officials managing programs or services to exercise this authority. However, a deputy head may require that this authority be formally delegated at his or her discretion.

Combination of small amounts: If there are several small outstanding amounts due that total more than the minimum amount threshold established by the deputy head for an invoicing period, departmental officials are to charge interest provided that the amounts are related or combining them is consistent with departmental policy.

Examples and additional guidance: Examples of the application of paragraph 8(b) of the regulations are provided below. In addition, guidance related to the application of the publication on a Government of Canada website requirement is provided in Appendix B of this guide.

- A department published on its departmental website a minimum amount of $10 applicable uniformly to all its programs or services for the purpose of the application of paragraph 8(b) of the regulations. Within the receivables portfolio, the department has an account for which a debtor has a residual debt of $8 owing to the department. At the end of the invoicing period, the department does not send an invoice to the debtor, as the total amount owing of $8 is less than the minimum amount threshold of $10. As a result, no interest is payable on the outstanding amount of $8.

- During the next invoicing period, the same debtor incurs another debt of $8 with the department, so the total amount owing now exceeds the minimum amount threshold of $10. This new debt and the original debt of $8 may be combined if consistent with the departmental process. In this case, an invoice will be sent to the debtor and interest will be charged on the total amount owing if it becomes overdue.

7.4 Provision of goods, services or the use of facilities

General application of interest: although departments are to minimize receivables in program design, certain types of goods, services, or uses of facilities may be provided on credit. Overdue accounts related to these receivables are subject to the regulations, and interest accrues starting on the due date specified in a demand for payment or included in any terms and conditions for the provision of the goods, services or the use of facilities.

7.5 Repayable contributions

General application of interest: contribution amounts that are repayable under a funding agreement are subject to the regulations unless otherwise provided, and interest will accrue when a payment is received after a scheduled repayment date in accordance with the terms and conditions of the contribution agreement.

7.6 Concessionary loans

Definition and general application of interest: a concessionary loan is a loan made at no interest or at rates significantly below “market.” When a repayment of a concessionary loan is in default, the “concession” is rescinded for the amount that is in arrears. Under subsection 7(1) of the regulations, the interest rate to apply to the amount in arrears is equal to the difference between the interest rate set out in the regulations (see section 5 of this guide) and the concessionary rate set out in the loan agreement.

Example If the concessionary rate set out in a loan agreement is 1% and the current interest rate in accordance with section 5 of the regulations is 4%, the interest rate to apply on any arrears is 3% (the difference between the current rate of 4% and the concessionary rate of 1%).

Exceptions: the provision described in this subsection does not apply to the following concessionary loans:

- in accordance with paragraph 7(2)(a) of the regulations, concessionary loans made to countries that are subject to a multilateral debt relief agreement or undertaking to which Canada is a party (for example, the Paris ClubFootnote 2)

- concessionary loans made to international organizations or countries for the purpose of developmental assistance (paragraph 7(2)(b) of the regulations)

- concessionary loans for which agreements already provide for interest on the arrears (paragraph 4(c) of the regulations)

7.7 Accountable advances Footnote 3

General application of interest: interest may be charged on standing advances and other accountable advances made for specific purposes (for example, travel advances) that are not settled within the time specified in the Accountable Advances Regulations.

Specific requirement for accountable advances, other than standing advances: These accountable advances must be accounted for, and any unexpended balance must be repaid no later than 10 working days after the purpose for which the advance was made is fulfilled.

The settlement period of 10 working days is satisfied when the claim, including any required receipts and the amount owing (if any) is submitted, not when it is approved or audited. If, for example, a travel claim is audited and adjusted, and the advance holder owes an additional amount, this amount becomes a general debt due to the Crown. The department will issue a notice demanding repayment by a specified date to the advance holder.

Demand for repayment: when a demand of an accounting (that is, asking for proof supporting the balance of the amount of the advance and expenditures made from that advance) and repayment of an accountable advance is issued by the department according to subsection 7(2) of the Accountable Advances Regulations, any unexpended balance must be repaid by the advance holder or custodian, not later than 30 days after receiving the demand.

Determination of amount owing: interest is payable only on the amount owing to the federal government (that is, the unexpended balance), not on the total advance amount. However, if the advance holder does not file a claim, the amount owing to the federal government is the amount of the advance. When advance holders are late in filing their claims (that is, not accounting for the advance), departments should immediately notify them that interest is accruing.

General application for administrative charges: the regulations apply to administrative charges to be levied when a dishonoured instrument is received as a reimbursement of an accountable advance.

7.8 Cost of security for debts

General application of interest: departments may seek security for debts due to the Crown to mitigate the risks of non-repayment of a receivable. As part of the management of security for debts, departments may incur costs such as those related to the appraisal, registration or realization of a security. Unless legal counsel advises that it is prohibited by law, the appraisal, registration, realization and any associated legal costs should be charged with interest to the debtor. The interest should be calculated from the time the costs are incurred until they have been recovered.

Legal consultation: to provide authority for charging interest and to avoid disputes and litigation, the guidance of legal counsel should be sought to ensure that these considerations are reflected in the documents that establish the debt and the security.

7.9 Interest revenues

Treatment of interest revenues: normally, departments must not treat revenue from interest charges on overdue accounts receivables as additional funds to spend, as departments are not incurring the interest expense for the use of capital. The Department of Finance Canada absorbs the cost of interest on the use of capital as part of the public debt and does not charge these costs back to departments.

Exception: departments may pay interest on their use of capital as part of the administration of revolving funds and the interest charged under the regulations may be offset against those costs.

8. Are the low-value amounts thresholds applicable?

FAA section 155.2 and Low-Value Amounts Regulations: the small amounts provisions under section 155.2 of the FAA and the associated Low-Value Amounts Regulations apply to amounts owing to the Crown including interest charged under the Interest and Administrative Charges Regulations.

Small amounts deemed nil: where an amount receivable is deemed nil under the Low-Value Amounts Regulations, there is nothing to collect. In this case, interest does not accrue.

Note Subject to section 155.2 of the FAA and the Low-Value Amounts Regulations, an amount owing to a department is deemed nil when it is $2.00 or less.

Guide on Low-Value Amounts: detailed guidance on the application of section 155.2 of the FAA and the Low-value Amounts Regulations, including application related to interest, is provided in the Guide on Low-Value Amounts.

9. When may interest or administrative charges be waived?

Under sections 9 and 12 of the regulations, ministers, or any departmental officials having appropriate delegated authority, may waive or reduce interest and administrative charges under certain circumstances, which are summarized as follows:

Administrative costs exceed amount owing: applies when the administrative costs of assessing, billing and collecting the interest or administrative charge would exceed the amount of interest or administrative charge owing. This circumstance may arise when a debtor pays an overdue amount but not the accrued interest, and the outstanding accrued interest amount is minimal.

Interest amount in dispute: applies when the interest is in respect of an amount in dispute that has been settled in whole, or in part, in favour of the debtor.

Overpayments will be recovered from subsequent entitlements: interest may be waived or reduced when an overpayment or erroneous payment of salary, wages or recurring benefits or allowances is to be recovered from a subsequent payment of the same nature. However, the interest cannot be waived if the overpayment or erroneous payment was received as a result of a fraud, through falsification of a document or any other offence committed by the person who received the overpayment or erroneous payment.

Penalty waivers: when a person receives an overpayment or erroneous payment as a result of a fraud or other offence, the department may authorize a waiver of the interest payable when a fine or penalty that takes into account interest on the overpayment or erroneous payment has been imposed. The waiver does not require that the fine or penalty equal the interest that would have been charged. However, if the penalty is significantly less, the waiver should not generally be used. Both interest and a penalty could be imposed, as the Canada Revenue Agency does for tax fraud or evasion.

Emergencies: applies when there is a critical situation of a temporary nature that meets all of the following circumstances:

- is so serious as to be a national or provincial emergency

- causes substantial financial hardship

- is the result of a serious natural disaster, disease, acts of terrorism or act of sabotage

- results or may result in danger to the lives, health or safety of individuals, danger to property, social disruption or a breakdown in the flow of essential goods, services or resources

When all the circumstances above are met, the minister may waive or reduce interest and/or administrative charges on a case by case basis following an internally established set of criteria, or on a general basis for the duration of the emergency.

Circumstances beyond the debtor’s control: applies when a debtor was prevented from making a payment or the payment instrument was not processed in circumstances beyond the debtor’s control, such as a breakdown in the electronic systems used to transfer funds and process payments, a postal disruption, or incapacity of the debtor.

When a department is contemplating a waiver or reduction of interest or administrative charges in circumstances beyond the debtor’s control, the appropriate minister or departmental official shall take into consideration the case presented by the debtor and other considerations, as set out in subsections 9(3) or 12(3) of the regulations. In this case, a waiver must be on an individual basis (that is, there are no class waivers).

9.1 What are the effects of waiving interest or administrative charges?

No amount is payable: under subsections 155.1(4) and (5) of the FAA, if a department waives (or reduces) interest or administrative charges, no interest or administrative charge amount (or the reduced amount) is payable to the department. In such cases, there would be nothing to write off as the waiver of interest or the administrative charge has the effect of extinguishing the debt and releasing the debtor from all liability for the amount waived. An adjusting entry must be made to reverse or reduce any interest or administrative charge recorded in the accounts of the department.

9.2 When interest can be written off, and what are the effects?

Circumstance: when departments write off a debt as uncollectible, they must also write off the accrued interest related to this debt.

Effect: a write-off does not extinguish a debt. If the department resumes collection action, interest would be reinstated from the original due date unless it was extinguished through another authority, such as a forgiveness or a remission.

9.3 Who can authorize the waiver of interest and administrative charges?

Appropriate minister: under subsection 155.1(4) of the FAA, the appropriate minister of a department responsible for the collection of an amount owed to the Crown is authorized to waive the interest or administrative charge in accordance with the regulations.

Delegation: sections 9 and 12 of the regulations state that the appropriate minister of a department or any public officer authorized in writing by that minister may waive interest or an administrative charge under criteria specified in these sections. The authorization in writing from the minister referred to in these sections is normally performed through a departmental delegation chart for spending and financial authorities. Public officers occupying positions with delegated authority to waive interest and administrative charges may exercise this authority when required and in accordance with the regulations.

9.4 What are the reporting requirements related to waivers of interest or administrative charges?

Public Accounts: waivers of interest or administrative charges made under sections 9 or 12 of the regulations are reported in the Public Accounts of Canada in the manner prescribed in the Public Accounts instructions issued annually by the Receiver General.

10. Accounting for interest and administrative charges

Coding Manual: The Accounts Receivables section of the Government of Canada Accounting and Coding Manual provides guidance on how to account for interest and administrative charges payable to the federal government according to the regulations.

11. References

11.1 Legislation

11.2 Related policy and guidance instruments

- Policy on Financial Management

- Directive on Public Money and Receivables

- Directive on Charging and Special Financial Authorities

- Directive on Payments

- Government of Canada Accounting and Coding Manual

- Guide on Low-Value Amounts

12. Enquiries

Members of the public may contact Treasury Board of Canada Secretariat Public Enquiries if they have questions about this guide.

Individuals from departments should contact their departmental financial policy group if they have questions about this guide.

Individuals from a departmental financial policy group may contact Financial Management Enquiries for interpretation of this guide.

Appendix A: examples of interest calculations

The following definitions apply to this appendix:

- accrued interest

- Interest on overdue accounts or late payments that is calculated and accrued in accordance with section 5 of the Interest and Administrative Charges Regulations

- amount used to calculate interest

- Consists of any amount owing to a department that is overdue and accrues interest compounded according to section 5 of the regulations.

- debt

- Amount owing to a department as a result of an overpayment or erroneous payment; or under any other Act of Parliament, or any regulation, order, contract or arrangement.

- receipt

- payment received by the department from a debtor in relation to a debt due to the Crown

- total amount due

- Consists of the debt and accrued interest less the receipts.

Example 1

Amount owing: $5,000

Interest rate (April to May): 4.00%

Interest rate (June): 4.25%

Date of invoice: April 1

Due date: May 1

| Date | Receipt | Debt | Accrued interest | Total amount due | Amount used to calculate interest | Comments |

|---|---|---|---|---|---|---|

| Nil | $5,000.00 | Nil | $5,000.00 | Nil | Invoice issued. Amount is not overdue; therefore, no interest accrued. | |

| Nil | $5,000.00 | Nil | $5,000.00 | $5,000.00 | Interest started to accrue on the due date. | |

| ($3,000.00) | $2,000.00 | $7.12 | $2,007.12 | $2,000.00 |

Interest accrued for 13 days (May 1 to May 13) on the amount of $5,000. Interest calculation: (13 days ÷ 365) × 4% × $5,000 = $7.12 As of May 14, interest accrued on the amount of $2,000. |

|

| ($600.00) | $1,400.00 | $9.31 | $1,409.31 | $1,400.00 |

Interest accrued for 10 days (May 14 to May 23) on the amount of $2,000. Interest calculation: (10 days ÷ 365) × 4% × $2,000 = $2.19 As of May 24, interest accrued on the amount of $1,400. |

|

| Nil | $1,400.00 | $10.54 | $1,410.54 | $1,410.54 |

Interest accrued for 8 days (May 24 to May 31) on the amount of $1,400. Interest calculation: (8 days ÷ 365) × 4% × $1,400 = $1.23 As interest is compounded monthly, accrued interest calculated for the period from May 1 to May 31 will now be compounded. As of June 1, interest accrued on the amount of $1,410.54. |

|

| ($400.00) | $1,000.00 | $14.48 | $1,014.48 | $1,010.54 |

Interest accrued for 24 days (June 1 to June 24) on the amount of $1,410.54. Interest calculation: (24 days ÷ 365) × 4.25% × $1,410.54 = $3.94 As of June 25, interest accrued on the amount of $1,010.54. |

|

| Nil | $1,000.00 | $15.19 | $1,015.19 | $1,015.19 |

Interest accrued for 6 days (June 25 to June 30) on the amount of $1,010.54. Interest calculation: (6 days ÷ 365) × 4.25% × $1,010.54 = $0.71 As interest is compounded monthly, accrued interest calculated for the period from June 1 to June 30 will now be compounded. As of July 1, interest accrues on the amount of $1,015.19. |

Example 2

Amount owing: $5,000

Interest rate (April to May): 4.00%

Interest rate (June): 4.25%

Date of invoice: April 1

Due date: May 1

| Date | Receipt | Debt | Accrued interest | Total amount due | Amount used to calculate interest | Comments |

|---|---|---|---|---|---|---|

| Nil | $5,000.00 | Nil | $5,000.00 | Nil | Invoice issued. Amount is not overdue; therefore no interest accrued. | |

| Nil | $5,000.00 | Nil | $5,000.00 | $5,000.00 | Interest started to accrue on the due date. | |

| ($5,000.00) | $0 | $7.12 | $7.12 | $0 |

Interest accrued for 13 days (May 1 to May 13) on the amount of $5,000. Interest calculation: (13 days ÷ 365) × 4% × $5,000 = $7.12 As of May 14, amount due is $7.12. |

|

| Nil | $0 | $7.12 | $7.12 | $7.12 | As the amount due of $7.12 consisting of accrued interest is not received on June 1 and interest is compounded monthly, the accrued interest (calculated for the period beginning on May 1) will now be compounded. | |

| Nil | $0 | $7.14 | $7.14 | $7.14 |

Interest accrued for 30 days (June 1 to June 30) on the amount of $7.12. Interest calculation: (30 days ÷ 365) × 4.25% × $7.12 = $0.02 As of July 1, interest accrues on the amount of $7.14. |

Appendix B: Guidance for the application of the publication requirement under paragraph 8(b) of the Interest and Administrative Charges Regulations

Paragraph 8(b) of the regulations states that: “no interest is payable on an outstanding amount due for a period in respect of a program or service if the total amount payable for the period, including accrued interest, is less than the minimum amount for which a demand for payment would normally be issued, as established by the deputy head responsible for the program or service and published for the purpose of this paragraph on a Government of Canada website.”

This provision requires departments that establish minimum amounts for the purpose of this provision to publish them on a Government of Canada website. When a minimum amount is published for the purpose of paragraph 8(b), the effect is that no interest is payable by a debtor when an outstanding debt due to a department, in respect of a program or service, at the end of a period (e.g. invoicing period) is below the minimum amount set by the department for that purpose.

Departments that do not use this regulatory option as part of their receivables management processes are not impacted by this publication requirement.

Examples of the application of this publication requirement are provided below.

Example 1

A department with a monthly invoicing cycle with an established threshold of $10 for all its receivables for the purpose of paragraph 8(b) would publish the following on a Government of Canada website:

Departmental minimum amounts for outstanding debts under which interest is not payable by a debtor

The Interest and Administrative Charges Regulations require federal departments and agencies to publish minimum amounts under which interest is not payable by a person on an outstanding amount due at the end of a period in respect of a program or service.

| Program or Service | Minimum Amount | Periodic frequency of demand for payments |

|---|---|---|

| All departmental programs or services | $10 | Monthly |

Example 2

A department that sets various minimum amounts for its programs or services for the purpose of paragraph 8(b) would publish the following on a Government of Canada website:

Departmental minimum amounts for outstanding debts under which interest is not payable by a debtor

The Interest and Administrative Charges Regulations require federal departments and agencies to publish minimum amounts under which interest is not payable by a person on an outstanding amount due at the end of a period in respect of a program or service.

| Program or Service | Minimum Amount | Periodic frequency of demand for payments |

|---|---|---|

| Program X | $5 | Bi-weekly |

| Program Y | $5 | Monthly |

| Service Z | $10 | Quarterly |

| All other departmental programs or services | $10 | Monthly |