ARCHIVED - Office of the Superintendent of Financial Institutions Canada

This page has been archived.

This page has been archived.

Archived Content

Information identified as archived on the Web is for reference, research or recordkeeping purposes. It has not been altered or updated after the date of archiving. Web pages that are archived on the Web are not subject to the Government of Canada Web Standards. As per the Communications Policy of the Government of Canada, you can request alternate formats on the "Contact Us" page.

2007-08

Departmental Performance Report

Office of the Superintendent of Financial Institutions Canada

Supplementary Information (Tables)

Table of Contents

- Sources of Respendable and Non-respendable Revenue

- User Fees/External Fees

- Response to Parliamentary Committees and External Audits

- Internal Audits and Evaluations

- Travel Policies

Table 3: Sources of Respendable and Non-Respendable Revenue

This table identifies revenues by program activity received from sources both internal and external to the government. For 2007-2008, OSFI’s total revenues were $90.5 million, including non-respendable revenue of $374 thousand for the collection of Late and Erroneous Filing Penalties. The respendable revenues are largely comprised of asset- or premium-based industry assessments, surcharge assessments to staged institutions, and user fees for specific services related to Regulatory Approvals. The majority of cost-recovered services in Regulation and Supervision of Federally Regulated Financial Institutions relates to implementing the internal ratings-based approach of the New Basel Capital Accord.

Respendable Revenues

The increase in respendable revenues in 2007-2008 from the previous year is largely due to increases in Base Assessment revenue and increases in Pension Fee Revenue. The 2007-2008 Pension Fee rate was $24.00 per member, 45% higher than the 2006-2007 rate. This rate increase was required in order to recover an accumulated deficit from the last 3 years as a result of directing incremental resources to problem pension plans.

| ($ thousands) | Actual 2005-2006 |

Actual 2006-2007 |

2007‑2008 | |||

| Main Estimates |

Planned Revenues |

Total Authorities |

Actual | |||

| (1) Regulation and Supervision of Federally Regulated Financial Institutions | ||||||

| Base Assessments | 67,726 | 60,375 | 70,489 | 70,489 | 70,489 | 70,080 |

| User Fees and Charges | 6,268 | 3,588 | 2,147 | 2,147 | 2,147 | 3,226 |

| Cost-Recovered Services | 3,515 | 4,248 | 3,278 | 3,278 | 3,278 | 3,403 |

| (2) Regulation and Supervision of Federally Regulated Private Pension Plans | ||||||

| Pension Plan Fees | 3,809 | 5,281 | 6,513 | 6,513 | 6,513 | 7,220 |

| (3) International Assistance | ||||||

| Base Assessments | - | 93 | 519 | 519 | 519 | - |

| Cost-Recovered Services | 1,378 | 1,610 | 1,507 | 1,507 | 1,507 | 1,582 |

| (4) Office of the Chief Actuary | ||||||

| User Fees and Charges | 96 | 145 | 35 | 35 | 35 | 21 |

| Cost-Recovered Services | 3,993 | 3,919 | 5,247 | 5,247 | 5,247 | 4,527 |

| Total Respendable Revenues | 86,784 | 79,259 | 89,735 | 89,735 | 89,735 | 90,059 |

Non-Respendable Revenues

The non-respendable revenues are all related to late and erroneous filing penalties. Effective 2002-2003, OSFI began collecting late and erroneous filing penalties from financial institutions that submit late and/or erroneous financial and corporate returns. On August 31, 2005 the Administrative Monetary Penalties (OSFI) Regulations came into force. These Regulations implement an administrative monetary penalties regime pursuant to which the Superintendent can impose penalties in respect of specific violations, as designated in the schedule to the Regulations. These Regulations incorporate the late and erroneous filing penalty regime and replace the Filing Penalties (OSFI) Regulations.These penalties are billed quarterly, collected and remitted to the Consolidated Revenue Fund. By regulation, OSFI cannot use these funds to reduce the amount that it assesses the industry in respect of its operating costs.

| ($ thousands) | Actual 2005- 2006 |

Actual 2006- 2007 |

2007-2008 | |||

| Main Estimates |

Planned Revenues |

Total Authorities |

Actual | |||

| Regulation and Supervision of Federally Regulated Financial Institutions | ||||||

| Filing Penalties | 805 | 227 | 450 | 450 | 450 | 374 |

| Total Non-Respendable Revenues | 805 | 227 | 450 | 450 | 450 | 374 |

Table 4-A: User Fee Reporting

Access to Information User Fees

1 According to prevailing legal opinion, where the corresponding fee introduction or most recent modification occurred prior to March 31, 2004:

- the performance standard, if provided, may not have received parliamentary review; and

- the performance standard, if provided, may not respect all establishment requirements under the User Fee Act (e.g. international comparison; independent complaint address).

- the performance result, if provided, is not legally subject to section 5.1 of the User Fee Act regarding fee reductions for unachieved performance.

Table 4–B: Policy on Service Standards for External Fees

Table 4-B is a standard reporting form developed to meet the reporting requirements of the Policy. As the requirements of the User Fee Act and the Policy are very similar, much of the information contained in this table is also found in table 4-A.

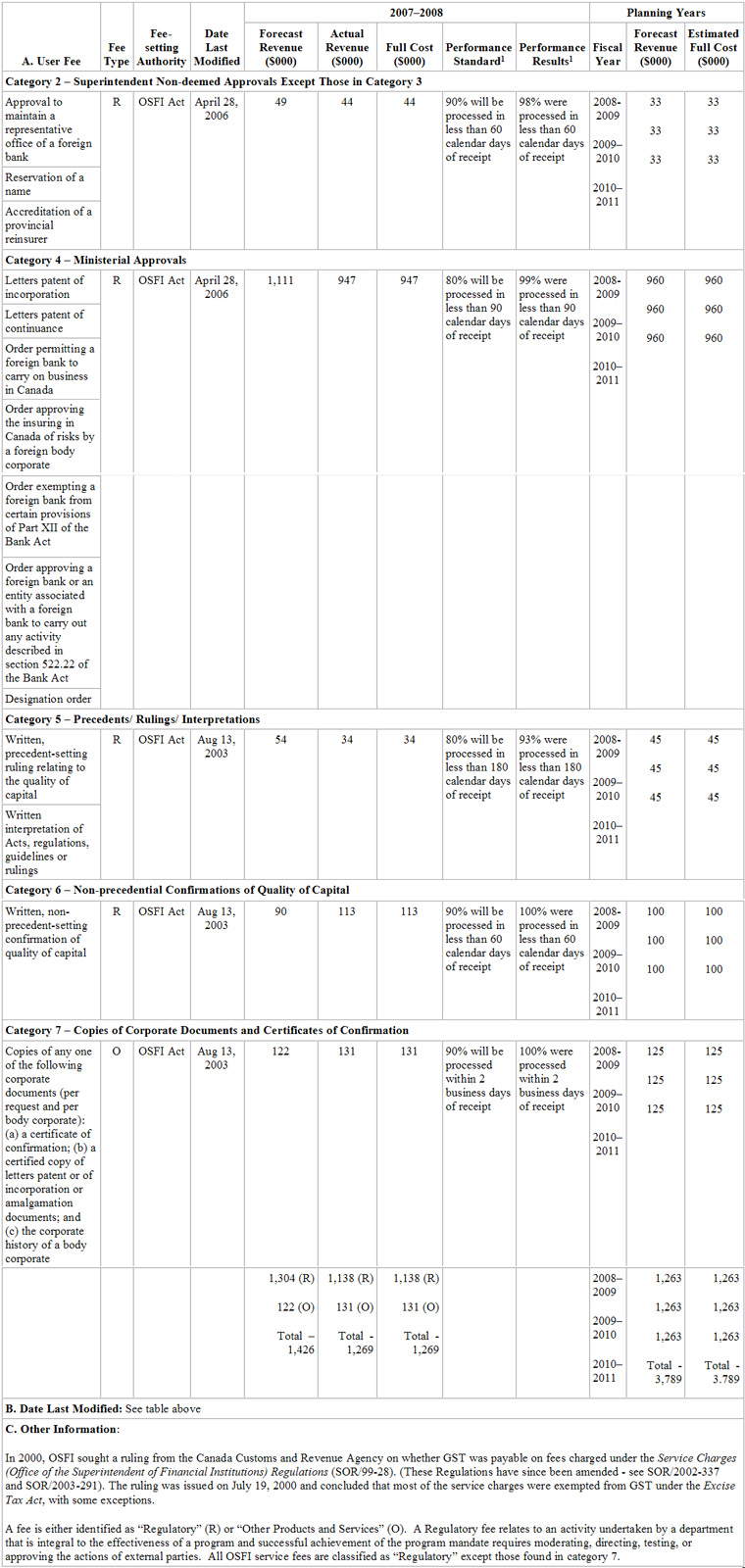

| A. External Fee | Service Standard2 | Performance Results3 | Stakeholder Consultation |

| Category 2 – Superintendent Non-deemed Approvals Except Those in Category 3 |

In March 2005, paying and non-paying stakeholders were asked to review and comment on the proposed service standards that were developed based on the analysis and research. Comments were received over a three month period and feedback on the comments was provided to each stakeholder who took the opportunity to provide input. Stakeholders were generally supportive of the initiative, especially with regard to OSFI’s early implementation of the government’s policy. OSFI received some queries with regard to the increased administrative costs associated with monitoring compliance with these new standards. We noted that, as OSFI has monitored application processing time for a number of years, OSFI does not expect to incur additional costs associated with monitoring compliance with these service standards. This expectation has proven to be the case. OSFI continues to review the standards on an ongoing basis and, once experience with the application of the standards has developed, some modifications may be made. |

||

| Approval to maintain a representative office of a foreign bank | 90% will be processed in less than 60 calendar days of receipt | 98% were processed in less than 60 calendar days of receipt | |

| Reservation of a name | |||

| Accreditation of a provincial reinsurer | |||

| Category 4 – Ministerial Approvals | |||

| Letters patent of incorporation | 80% will be processed in less than 90 calendar days of receipt | 99% were processed in less than 90 calendar days of receipt | |

| Letters patent of continuance | |||

| Order permitting a foreign bank to carry on business in Canada | |||

| Order approving the insuring in Canada of risks by a foreign body corporate | |||

| Order exempting a foreign bank from certain provisions of Part XII of the Bank Act | |||

| Order approving a foreign bank or an entity associated with a foreign bank to carry out any activity described in section 522.22 of the Bank Act | |||

| Designation order | |||

| Category 5 – Precedents/ Rulings/ Interpretations | |||

| Written, precedent-setting ruling relating to the quality of capital | 80% will be processed in less than 180 calendar days of receipt | 93% were processed in less than 180 calendar days of receipt | |

| Written interpretation of Acts, regulations, guidelines or rulings | |||

| Category 6 – Non-precedential Confirmations of Quality of Capital | |||

| Written, non-precedent-setting confirmation of quality of capital | 90% will be processed in less than 60 calendar days of receipt | 100% were processed in less than 60 calendar days of receipt | |

| Category 7 – Copies of Corporate Documents and Certificates of Confirmation | |||

| Copies of any one of the following corporate documents (per request and per body corporate): (a) a certificate of confirmation; (b) a certified copy of letters patent or of incorporation or amalgamation documents; and (c) the corporate history of a body corporate | 90% will be processed within 2 business days of receipt | 100% were processed within 2 business days of receipt | |

| B. Other Information: | |||

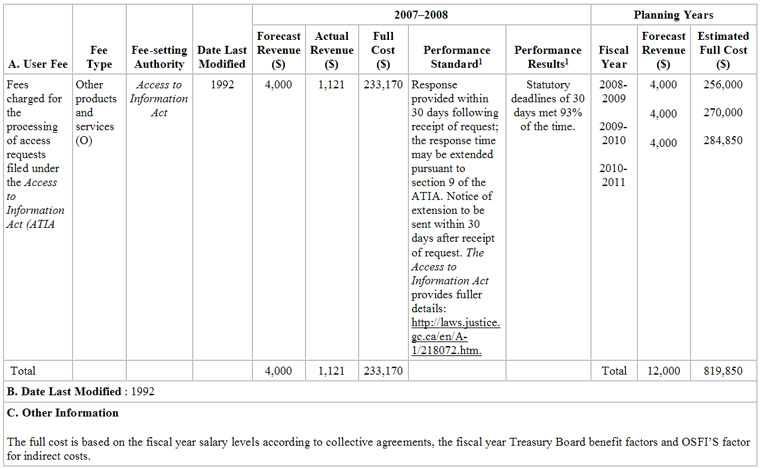

Access to Information Requests Policy on Service Standards for External Fees

| A. External Fee | Service Standard2 | Performance Results3 | Stakeholder Consultation |

| Fees charged for the processing of access requests filed under the Access to Information Act (ATIA). |

Response provided within 30 days following receipt of request; the response time may be extended pursuant to section 9 of the ATIA. Notice of extension to be sent within 30 days after receipt of request. The Access to Information Act provides fuller details: http://laws.justice.gc.ca/en/A-1/index.html

|

Statutory deadlines met 93% of the time | The service standard is established by the Access to Information Act and the Access to Information Regulations. Consultations with stakeholders were undertaken by the Department of Justice and the Treasury Board Secretariat for amendments done in 1986 and 1992. |

|

B. Other Information

None |

|||

2 As established pursuant to the Policy on Service Standards for External Fees:

- service standards may not have received parliamentary review; and

- service standards may not respect all performance standard establishment requirements under the User Fee Act (e.g. international comparison; independent complaint address).

3 Performance results are not legally subject to section 5.1 of the UFA regarding fee reductions for unachieved performance.

Table 5: Response to Parliamentary Committees and External Audits

| Response to Parliamentary Committees |

| Not applicable during 2007-2008. |

| Response to the Auditor General (including to the Commissioner of the Environment and Sustainable Development) |

| Not applicable during 2007-2008. |

| External Audits |

|

During 2007-2008, the Canada Public Service Agency conducted two audits of OSFI:

|

Table 6-A: Internal Audits

| 1. Name of Internal Audit | 2. Audit Type | 3. Status | 4. Completion Date | 5. Electronic Link to Report |

| Supervision Sector: Financial Conglomerate Group – Life Insurance | Supervision – Risk Assessment & Interventions | In-progress | 2008-2009 | Will be posted on OSFI website |

| Corporate Services: Human Resources Planning | Corporate Services – Human Services | In-progress | 2008-2009 | Will be posted on OSFI website |

| Corporate Services – Information Technology Services Planning | Corporate Services – Information Technology | In-progress | 2008-2009 | Will be posted on OSFI website |

| Regulation: Actuarial Division (support for Supervision) | Supervision – Risk Assessment and Interventions | In-progress | 2008-2009 | Will be posted on OSFI website |

| Regulation Sector: Legislative Approvals | Regulation Sector | In-progress | 2008-2009 | Will be posted on OSFI website |

| Superintendent’s office – Management Oversight | Superintendent’s Office | In-progress | 2008-2009 | Will be posted on OSFI website |

| Supervision Sector: Financial Institutions Group- Deposit Taking Institutions | Supervision – Risk Assessment & Interventions | Completed | June 2007 | Available on OSFI website |

| Supervision Sector: Credit Risk Department Review | Supervision – Support Group | Completed | April 2008 | Available on OSFI website |

| Corporate Services – Staffing Process | Corporate Services – Human Services | Completed | October 2007 | Available on OSFI website |

| Superintendent’s office- OSFI Planning Activities and Processes | Superintendent’s Office | Completed | April 2008 | Available on OSFI website |

Note: Actions taken as a result of completed audits are described in Section I.4.4

Table 7: Travel Policies

OSFI is a separate employer. In order to meet the requirements of its mandate, OSFI has elected to implement a travel policy specifically for OSFI. The OSFI policy is virtually identical to the Treasury Board Travel Directive, with the exception noted.

Comparison to the Treasury Board of Canada Special Travel Authorities as applied to OSFI’s executive group

OSFI takes a more restrictive approach than the TB Special Travel Authorities with respect to business class airfare for its Executive group of employees.

Comparison to the Treasury Board of Canada Travel Directive, Rates and Allowances as applied to all OSFI employees

OSFI Travel policy of the Office of the Superintendent of Financial Institutions |

| Authority: Under section 13 of the OSFI Act, the Superintendent is authorized to exercise the powers and perform the functions of the Treasury Board that relate to human resources management within the meaning of the Financial Administration Act, including the determination of terms and conditions of employment and the responsibility for employer and employee relations. |

| Coverage: The OSFI Travel Policy applies to all employees, including casual, term and indeterminate. |

Principal difference(s) in policy provisions: The TB Travel Directive allows for Business Class air travel for trips exceeding 9 hours. OSFI’s Travel Policy states that non-executives may be authorized to upgrade to Business/Executive Class air travel in accordance with the following principles:

|

| Principal financial implications of the differences: For 2007-2008 the estimated net cost of this difference in policy is approximately $191 thousand, based on 73 trips at an average additional cost of $2.6 thousand per trip. |

OSFI effectively monitors its travel costs through communications with all employees, directed communications on policy interpretation and guidance, direct communications with managers on travel claim issues, monthly monitoring against budget, and semi-annual detailed analyses of travel expenses.