ARCHIVED - Canada Revenue Agency - Report

This page has been archived.

This page has been archived.

Archived Content

Information identified as archived on the Web is for reference, research or recordkeeping purposes. It has not been altered or updated after the date of archiving. Web pages that are archived on the Web are not subject to the Government of Canada Web Standards. As per the Communications Policy of the Government of Canada, you can request alternate formats on the "Contact Us" page.

2011-12

Report on Plans and Priorities

Canada Revenue Agency

The original version was signed by

The Honourable Gail Shea, P.C., M.P.

Minister of National Revenue

Mission

To administer tax, benefits, and related programs, and ensure compliance on behalf of governments across Canada, thereby contributing to the ongoing economic and social well‑being of Canadians.

Vision

The CRA is the model for trusted tax and benefit administration, providing unparalleled service and value to its clients, and offering its employees outstanding career opportunities.

Values

Promise

Contributing to the well-being of Canadians and the efficiency of government by delivering world-class tax and benefit administration that is responsive, effective, and trusted.

Table of Contents

- Our raison d'être

- Our contribution to the Federal Sustainable Development Strategy (FSDS)

- Planning summary

- Contribution of priorities to strategic outcomes

- Taxpayer and business assistance (PA1)

- Assessment of returns and payment processing (PA2)

- Accounts receivable and returns compliance (PA3)

- Reporting compliance (PA4)

- Appeals (PA5)

- Benefit programs (PA6)

- Internal services (PA7)

Message from the Minister

The Canada Revenue Agency (CRA) plays an important role in implementing our government's commitments with regards to administering Canada's tax laws; assessing and collecting taxes and levies; delivering social and economic benefits, such as the GST/HST credit and the Canada Child Tax Benefit; and ensuring that this is all done with the transparency and integrity Canadians have come to expect.

This Report on Plans and Priorities 2011-2012 outlines how the CRA will fulfil this role, while ensuring that it operates within our means.

Our government's Economic Action Plan has brought much needed tax relief to Canadians and I am proud of the role the CRA had in implementing these measures. Going forward, we will continue to keep focused on priorities, including fairness to taxpayers. We will work to close loopholes, enter into more tax treaties to combat international tax evasion, and continue with efforts to combat the underground economy.

As we look to the future, Canadian taxpayers can continue to have confidence that the CRA will maintain strong stewardship of our tax and benefits system.

The Honourable Gail Shea, P.C., M.P.

Minister of National Revenue

Message from the Commissioner

The Canada Revenue Agency (CRA) has a key role to play in Canada's economy by administering taxes for federal, provincial, territorial, and First Nations governments; we also contribute to the government's social outcomes through our benefit programs. Our Report on Plans and Priorities is an annual opportunity for us to state the challenges and opportunities we see over the planning period, and how we will respond so that the Agency continues to be a world leader in tax and benefit administration.

Over the last two years, the CRA has played a key role in the delivery of the government's Economic Action Plan: our timely and efficient implementation of tax measures ensured that vital sectors of our economy received the support that they needed to survive through difficult economic times. We will continue to support government priorities over the following year, through responsible allocation of resources, to ensure that we sustain our core business while respecting the need for fiscal restraint.

Addressing non-compliance with tax and benefits legislation is an important element of our core business and essential to protecting Canada's revenue base. Providing services that help taxpayers and benefit recipients fulfil their obligations and receive their entitlements is also core to our mandate. This plan outlines some key compliance initiatives to address the highest risk areas of non-compliance, renews our commitment to online, secure self-service, and outlines steps to maintain Canadians' trust and confidence in the CRA as a fair and effective organization.

The challenges ahead present an opportunity for the CRA to demonstrate once again that we are a resilient and reliable organization that continues to deliver on its mandate and achieves results for Canadians.

Linda Lizotte-MacPherson

Commissioner and Chief Executive Officer

Canada Revenue Agency

Section I: Agency Overview

Our raison d'être

The Canada Revenue Agency (CRA) is responsible for administering, assessing, and collecting hundreds of billions of dollars in taxes annually. The tax revenue it collects is used by federal, provincial, territorial, and First Nations governments to fund programs and services that contribute to the quality of life of Canadians.

No other public organization touches the lives of more Canadians on a daily basis. The CRA uses its federal infrastructure to deliver benefits, tax credits, and other services that support the economic and social well‑being of Canadian families, children, and persons with disabilities.

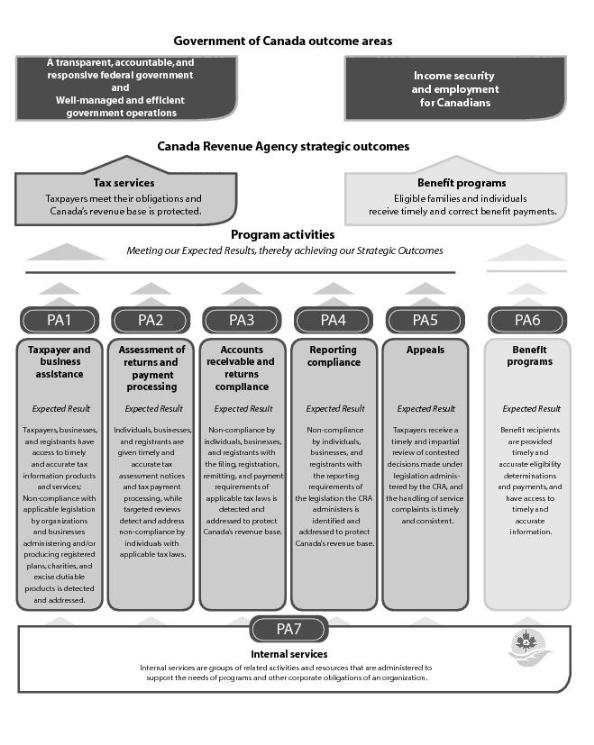

The CRA contributes to three of the Government of Canada's outcome areas:

- a transparent, accountable, and responsive federal government;

- well-managed and efficient government operations; and

- income security and employment for Canadians.

Our mandate

The CRA is mandated to administer tax, benefit, and other programs for the Government of Canada and provincial, territorial, and certain First Nations governments.

In carrying out its mandate the CRA strives to make sure that Canadians:

- pay their required share of taxes;

- receive their rightful share of entitlements; and

- are given an impartial and responsive review of contested decisions.

The following two strategic outcomes summarize the CRA's contribution to Canadian society.

- Taxpayers meet their obligations and Canada's revenue base is protected.

- Eligible families and individuals receive timely and correct benefit payments.

The achievement of these outcomes shows that we are fulfilling our mandate from Parliament.

Delivering results

In addition to the administration of income tax and benefit programs, the CRA now administers harmonized sales tax for five provinces. The CRA also verifies taxpayer income levels in support of a wide variety of federal, provincial, and territorial programs, ranging from student loans to health care initiatives. In addition, we provide other services, such as the Refund Set‑Off Program, through which we aid other federal agencies and departments, as well as provincial and territorial governments, in the collection of debts that might otherwise become uncollectible.

Our contribution to the Federal Sustainable Development Strategy (FSDS)

The Federal Sustainable Development Act establishes environmental sustainability as a long-term government-wide priority. It requires the Government of Canada to develop and table an FSDS that makes environmental decision-making more transparent.

The first FSDS sets a clear direction for environmental sustainability. It articulates four themes that establish common sustainable development (SD) goals and targets across government. The CRA is implicated by Theme IV: Shrinking the Environmental Footprint – Beginning with Government. The CRA's contributions are further explained in Section II, under Internal Services (PA7).

This icon is used throughout the CRA Report on Plans and Priorities (RPP) to indicate activities that

contribute to Theme IV of the FSDS.

This icon is used throughout the CRA Report on Plans and Priorities (RPP) to indicate activities that

contribute to Theme IV of the FSDS.

The CRA has prepared a detailed internal SD strategy that accounts for all interventions that support SD within the CRA. We also prepared an SD National Action Plan that will move us towards achieving our long-term SD outcomes. This Plan is articulated under two broad headings and three goals, namely:

- Goal 2–Deliver sustainable programs and services to Canadians

- Goal 3–Improve business sustainability

As part of its compliance with the Federal Sustainable Development Act, the CRA will table the CRA SD Strategy 2011-2014 through its 2011-2012 RPP and report on performance through the corresponding CRA Departmental Performance Report.

For more information on the CRA SD Strategy 2011-2014. Complete details on the Federal Sustainable Development Strategy.

CRA program activity architecture

Planning summary

Agency resources

Alignment to Government of Canada outcomes

| Performance indicators | Targets |

|---|---|

| Program activity (thousands of dollars) | Forecast spending | Planned spending | Alignment to Government of Canada outcome areas | ||

|---|---|---|---|---|---|

| 2010-2011 | 2011-2012 Footnote 1 | 2012-2013 Footnote 1 Footnote 2 | 2013-2014 Footnote 1 Footnote 2 | ||

| Strategic outcome: Eligible families and individuals receive timely and correct benefit payments. We assess our results against our benefits strategic outcome by measuring timelines and accuracy of payments and eligibility determination. We also monitor the number of government clients that rely on us as a service provider. Our targets vary between indicators. For information about CRA service standard targets please see our Web site. | |||||

| Benefit programs (PA6) | 338,978 | 356,806 | 351,618 | 355,196 | Income security and employment for Canadians |

| The following program activity supports all strategic outcomes within this organization. | |||||

|

|

|||||

|

|

|||||

| Strategic outcome: Taxpayers and benefit recipients receive an independent and impartial review of their service-related complaints. | |||||

|

Taxpayers' ombudsman Footnote 3

|

|||||

|

Total Planned Spending Footnote 4

|

|||||

Contribution of priorities to strategic outcomes

This CRA report on plans and priorities describes the results we expect to achieve over the next three years. It sets out our strategic and operational course during this period and identifies the resources needed to effectively and responsibly fulfil our mandate. It was developed in response to identified risks in our environment, global and domestic. Our objective is to make sure that we have in place effective strategies to deal with these risks.

Our plans are aligned with the following operational and management priorities for the Agency: promoting compliance, meeting service needs, addressing non-compliance, administering benefits, and enabling core business operations.

Implementing the initiatives over the period covered by this plan in the pursuit of our priorities will enhance our ability to achieve our strategic outcomes.

Our operating environment

An integral part of the strategic planning process involves a scan of the CRA's external and internal environment over the planning period. This assessment informs the decisions taken and underlies our priorities. The scan allows us to take stock of significant developments in the economic and social landscape, and determine whether priorities need to be adjusted in response.

A key feature of the current environment is the need for federal departments and agencies to contain costs as part of restoring the country to fiscal balance.

The CRA has moved proactively to ensure that the Agency will be able to continue delivering on its mandate while managing within a contained budget.

Globalization

Globalization and its associated powerful trends, such as the increasing pace of technological advancement, are also significant influences on the future of tax administration. The borderless nature of modern commerce allows companies to expand operations beyond their home country to establish global competitive advantage, but also creates increasing complexity for tax administrations as it becomes less clear where income is earned and where tax should be paid. The ability to move large amounts of money rapidly from one country to another helps those who want to avoid higher tax jurisdictions.

Tax administrations internationally are already responding to this new reality through increased collaboration–such as the move to joint audits of multinational corporations by two or more countries–and bilateral and multilateral information exchange is receiving unprecedented attention and support.

Over the next few years, we can expect globalization to increasingly influence the CRA as governments adapt taxation approaches to be effective in a global economy.

Technology and service

Although it is true that technological change offers the potential to increase overall productivity, it also results in an increased appetite by Canadians for real-time, integrated, cutting-edge service delivery. The CRA has made significant investments over the last 10 years to develop and implement a suite of tools, systems, and information-technology-enabled solutions in order to achieve maximum productivity. Information technology has enabled the CRA to automate many business transactions. We have already proven to be a leader in the Government of Canada in online service delivery. Over the planning period, we expect that demands for technology-enabled services will only increase. A critical success factor will be our ability to respond nimbly, building on our investments so far, while still safeguarding the reputation of the CRA and government for security and reliability.

IT sustainability

Over the years, we have managed our IT infrastructure by investing strategically to enable us to keep pace with our objectives for delivering affordable services and effective compliance activities. The aging of legacy applications is a concern that the CRA continues to guard against.

A changing workforce

The CRA's strategic direction will move the CRA to a growing reliance on knowledge workers as our processing activities become increasingly automated and interactions are conducted more and more on a self-service basis. The aging of Canada's population will introduce new challenges for the CRA as an employer. We recognize that the competition for talent will be a major factor for the CRA over the next 5 to 10 years as baby boomers leave the workforce.

Immigration is already the major contributor to the growth in Canada's working-age population and this trend is generally expected to increase over time. We will need to consider how best to attract and develop a workforce of even greater cultural and linguistic diversity representative of the citizens we serve. The Agency strategic workforce plan is updated annually to respond to these challenges and make sure that we develop a workforce that meets our future requirements.

Taxpayer attitudes and behaviour

In common with other tax administrations around the world, we recognize that voluntary compliance is underpinned by fundamental social norms regarding compliance with the law and contribution to society. Some of our most persistent and difficult challenges, such as the underground economy, are exacerbated by citizens' willingness to participate in cash transactions for immediate gain without an awareness of, or concern for, the impact on Canadian society. As we search for compliance solutions that will ensure a sustainable tax system, it is important to not assume that all solutions will be technology-based. We will continue to encourage approaches that educate and influence Canadians (including those new to our country), to see responsible tax and benefit practices as key to Canada's success, and to willingly comply.

Expenditure profile

For the period 2007-2008 to 2010-2011, total spending amounts include all Parliamentary appropriations and revenue sources: Main Estimates, Supplementary Estimates, funding associated with the increased personnel costs of collective agreements, maternity allowances and severance payments, as well as funding to insure implementation of Federal Budget initiatives and the Agency's carry forward adjustments from the prior year. It also includes spending of revenues received through the conduct of CRA's operations pursuant to Section 60 of the Canada Revenue Agency Act, Children's Special Allowance payments, payments to private collection agencies pursuant to Section 17.1 of the Financial Administration Act and disbursements to the provinces under the Softwood Lumber Products Export Charge Act, 2006. For the period 2011-2012 to 2013-2014, planned spending excludes carry forward adjustments which are only finalized once Public Accounts are completed and it also does not include any amounts for maternity allowances and severance payments. Finally, for the period 2012-2013 and 2013‑2014 planned spending amounts do not yet include a forecast for disbursements to the provinces under the Softwood Lumber Products Export Charge Act, 2006 (estimated at $140M in 2011-2012).

Since 2007-2008 the Canada Revenue Agency's Operating Expenditures reference levels have changed primarily as a result of: collective agreements/contract awards; policy and operational initiatives arising from various Federal Budgets and Economic Statements; transfers from the Department of Public Works and Government Services Canada for accommodations and real property services; and the commencement of responsibilities related to the administration of corporate tax in Ontario and the Softwood Lumber Agreement. Over the same period, there have also been a number of decreases as a result of various government-wide budget reduction exercises. The Operating Expenditures Vote was also reduced to create the Agency's new Capital Expenditures Vote.

The Agency Statutory Authorities have fluctuated over the course of the 2007-2008 to 2013-2014 period as a result of: adjustments to the Children's Special Allowance payments for eligible children in the care of specialized institutions; adjustments to the rates for the contributions to employee benefit plans; increases to the spending of revenues received through the conduct of operations pursuant to Section 60 of the Canada Revenue Agency Act; the introduction from 2007-2008 to 2009-2010 of payments to private collection agencies pursuant to Section 17.1 of the Financial Administration Act; and finally, the introduction in 2006, and adjustments to disbursements to the provinces under the Softwood Lumber Products Export Charge Act, 2006.

For information on our organisational votes and/or statutory expenditures, please see the 2011–12 Main Estimates publication.

Analysis of Program Activities by strategic outcome

In Section 1 of this report we have articulated the environment and strategic context in which the CRA plans to operate over the next three years. We have highlighted the longer-term strategic agenda we will pursue that will enable us to meet the challenges we are facing. This strategic agenda also informs the activities we carry out on a daily basis on behalf of Canadians.

These day to day activities are described in further detail throughout the next Section: Analysis of Program Activities by Strategic Outcome. For each program activity, we present a high-level discussion on our plans and priorities, our expected results, and associated indicators and targets that will enable us to measure our success in achieving our strategic outcomes.

Section II: Analysis of Program Activities by Strategic Outcome

Taxpayer and business assistance (PA1)

Benefit to Canadians

Our aim is to make sure that taxpayers, businesses, and registrants are given the tools, help, and information needed to voluntarily comply with their tax obligations. Also, we clarify the interpretation of the tax laws to protect Canada's revenue base.

Planned spending by program activity

|

Planned spending 2012-2013 Footnote 1

|

Planned spending 2013-2014 Footnote 1

|

|||

|---|---|---|---|---|

Program activity—Expected results and measures

Promoting compliance

Outreach

The CRA uses outreach to connect with Canadians and deliver the information and help they need to meet their tax obligations and to receive any benefits to which they may be entitled. To make sure that our outreach efforts are directed to the most appropriate audience (such as seniors, new Canadians, persons with disabilities, small businesses), we identify segments and topics on which to focus our outreach using public opinion research, demographic analysis, business trends, environmental scans, and compliance risk analysis.

Over the planning period, we will explore ways to improve voluntary compliance through an enhanced understanding of how to promote responsible citizenship. We will also consider alternative delivery models and maximize the use of appropriate partners.

The CRA uses segmentation for program delivery, based on broad sectors such as individual taxpayers, businesses, charities, and so on. The current initiative will use data gathering and analysis of such factors as changing demographics and the drivers of non‑compliance to refine our segments and develop an inventory of taxpayer segments.

Meeting service needs

Support the Charities Program

To promote compliance with income tax legislation and regulations for registered charities, we offer a thorough and timely application process, provide direct assistance to charities through our enquiries processes, and carry out extensive outreach initiatives.

The CRA's outreach programs target the charitable sector and the public at large, and include information sessions held across Canada, as well as webinars and webcasts. These provide participants with information on tax-receipted donations, record keeping, tax planning schemes, preparing for an audit, and potential sanctions in cases of non-compliance. Information about the requirements for registration is also available on our “Charities and Giving” Web pages.

Registered charities and applicants for registered status will continue to have access to high-quality application and enquiries processes and outreach initiatives.

Maintain service delivery channels

Providing timely and accessible information about obligations and entitlements is fundamental to a self-assessment tax system. Canadians are using diverse channels (the Web, telephone, in person, and in writing) to satisfy their information needs. We want to encourage taxpayers to migrate to the more affordable self-serve channels with agent help readily available when needed.

Our 1-800 telephone networks provide help and information to taxpayers through automated and agent‑assisted services. These networks are managed in real time to balance call volumes across the country and to provide fair access. Callers using the automated service can get general information and simple account information such as refund status, RRSP contribution room, and Tax-Free Savings Account contribution room 24 hours a day, seven days a week. In addition, The CRA Web site is continually updated to provide the latest relevant information. The content and the structure of our Web site are fine-tuned, based on the results of usability testing, to ensure client needs are being met.

Over the planning period, we will focus our research and analysis on better understanding client information needs and expectations. We will also explore best practices and emerging technology in taxpayer services. This will help enhance the design and development of our products and services.

Our enquiries and information services will develop more training and job aids for agents to respond to the increasing complexity of enquiries. Our focus on multimedia training products and new applications that link agents' desktops to reference material will reduce the time agents need to research specific topics.

The telephone channel remains the most popular way for taxpayers to contact us. Data gathered under the quality assurance program will support and strengthen the quality and accuracy of our responses to enquiries, and allow us to identify agent training needs, procedural and accuracy trends, and product and service gaps.

Our GST/HST Rulings program provides a written rulings and interpretations and a 1-800 telephone service to registrants and taxpayers that is typically requested for more complex GST/HST information and transactions. The program houses technical experts who provide certainty as to how the tax applies to specific transactions.

Addressing non-compliance

Implement an enhanced tobacco stamping regime

We collect the excise duty on tobacco products manufactured domestically, and the Canada Border Services Agency collects the duty on imported tobacco products. Protecting the duty revenue from tobacco products ensures that high prices on those goods can be maintained, thereby contributing to the Government's health objective of reducing smoking among Canadians.

The new regime will provide a stronger legal framework for tobacco product stamping with stronger ministerial powers. These powers include the authority to limit the possession of tobacco stamps to legal tobacco activities, to impose new penalties for counterfeited and not-accounted-for stamps, and to require increased accountability and control of stamps issued.

The new stamping regime will also provide enhanced tools for the Royal Canadian Mounted Police, which is responsible for enforcing the Excise Act, 2001. More effective compliance and enforcement activities by all partners will strengthen the integrity of the legal tobacco regime and combat counterfeit and illicit tobacco products.

During the implementation period of the tobacco stamping regime, we will continue to consult with the tobacco industry (manufacturers and importers), provincial and territorial governments, and other federal agencies and departments to further ensure compliance with the Excise Act, 2001. We will work closely with both Treasury Board of Canada Secretariat and Department of Justice Canada officials to complete the regulatory amendments for the new regime, including the stamping regime guidelines and excise duty notices.

The CRA will fully implement the new stamping regime so that all tobacco products manufactured and imported into Canada bear the new stamp. At the same time, we will encourage provinces and territories to adopt the new regime.

Detect and deter non-compliance in the Charities Program

Registered charities in Canada are tax-exempt and can issue charitable donation receipts to donors. To maintain these privileges, registered charities must file a registered charity information return and financial statements, and operate within the parameters of the Income Tax Act. Although cases of serious and intentional non-compliance by registered charities are not wide-spread, they do exist. Examples include illegal tax shelter donation arrangements, false receipting, and unacceptable fundraising practices.

Over the planning period, the Charities Program will focus on addressing identified non-compliance in a timely manner.

The program initiatives we will pursue over the planning period are listed in the following table.

Priority initiatives

Promoting compliance

Meeting service needs

Addressing non-compliance

Assessment of returns and payment processing (PA2)

Benefit to Canadians

Our aim is to deliver efficient and correct assessing of individual, business, trust, and information returns and timely payment processing, thereby promoting voluntary compliance and contributing to the protection of Canada's revenue base.

Planned spending by program activity

Program activity—Expected results and measures

Meeting service needs

Maintain our electronic services

Many filing and reporting options are available to help Canadians meet their tax obligations and requirements. We will continue to expand and enhance our existing services in a way that ensures they will be sustainable, cost-effective, and continue to meet the needs of Canadians and their representatives. We will communicate through new and innovative ways, including the Message Centre. The Message Centre will be available to businesses and authorized third-party representatives through the My Business Account portal. The user will be informed of a new or awaiting message in the Message Centre upon logging into My Business Account.

To streamline incoming payments and to offer Canadians multiple payment options, the CRA is developing a payment strategy. The strategy will identify new payment options and enhance current methods of payment to make paying taxes more convenient for taxpayers. It will support the overall government strategy for reducing the paper burden.

Support the take-up of electronic filing and electronic payments

The CRA will pursue cost-effective ways to improve service to Canadians and will introduce new electronic services and enhancements to existing services over the planning period, such as enabling clients and authorized representatives to update client information. We will also continue to promote our e-Services to encourage uptake and ensure that corporations, businesses, and other institutions are aware of the legislative changes requiring many businesses to file returns electronically.

We are enhancing our e-Services such as transfer payments. This year, we will add the ability to transfer a payment to a different program within the same Business Number and, in 2012, we will add the ability to transfer a payment to a different Business Number. In addition, we will make it easier for businesses to authorize their representatives.

Maintain service delivery channels

Providing timely and accessible information about obligations and entitlements is fundamental to a self-assessment tax system. Canadians are using diverse channels (the Web, telephone, in person, and in writing) to satisfy their information needs.

We want to encourage taxpayers and benefit recipients to migrate to the more affordable self-serve channels. Over the planning period we will focus our research and analysis on better understanding client information needs and expectations. We will also explore best practices and emerging technology in taxpayer services. This will help enhance the design and development of our products and services.

Addressing non-compliance

We will enhance our ability to address non‑compliance by continuing to improve our post‑assessment review programs. We will do this through effective use of third‑party information and refining risk assessment capabilities.

We will focus on discrepancies, correcting errors, validating claims, and helping individuals and businesses comply in areas of new legislation. We will implement all required federal, provincial, and territorial legislative changes, giving effect to the tax agendas of governments across Canada.

The program initiatives we will pursue over the planning period are listed in the following table.

Priority initiatives

Meeting service needs

Addressing non-compliance

Accounts receivable and returns compliance (PA3)

Benefit to Canadians

Our aim is to promote and enforce compliance with Canada's tax laws for filing, withholding, registering, remitting, and debt obligations, including those amounts collected or withheld in trust for the Government of Canada, as well as the provinces, the territories, and certain First Nations governments.

Planned spending by program activity

Program activity—Expected results and measures

Addressing non-compliance

Payment non-compliance

Two main sources contribute to outstanding account receivables:

- debts that taxpayers create by not paying amounts owing when they file their returns; and

- debts identified by the CRA through our compliance activities.

Both sources shape taxpayer payment compliance obligations in respect of filing of returns and payment of amounts due.

The accumulation of new debt depends on factors that are outside of our control. They include:

- domestic and international economic situations;

- aggressive tax planning and strategic insolvencies; and

- socio-economic factors that may influence taxpayer compliance behaviour.

Although substantial progress has been made enhancing our collection capabilities, more work is needed. Our corporate risk inventory has identified a number of risks that could affect our ability to meet our business objectives. Payment compliance was identified as a significant business risk.

Our work on the payment non-compliance initiative will focus on continuing to improve the identification of the specific taxpayer segments involved. We will refine our management of the growing tax debt through various means, including addressing the underlying causes of payment non-compliance at the behavioural level. We will increase our attention on the need for earlier interventions with potential debtors to prevent debts from arising and to help taxpayers meet their obligations in a timely and fair manner. Meanwhile, our tactical approach remains centred on addressing the current accounts receivable inventory.

Identify non-compliance in the underground economy

The underground economy undermines the competitiveness of Canadian businesses because it offers an unfair advantage to those who fail to comply with Canada's tax laws. We use a mix of education, outreach, communication, and compliance actions to combat the underground economy. We carry out identification projects to detect non-filers engaged in underground economy activities and require them to file outstanding tax returns and register for the goods and services tax/harmonized sales tax (GST/HST).

The CRA has a comprehensive Underground Economy Compliance Strategy that includes a 28-point action plan designed to find the right mix of compliance risk treatments, which will effectively influence taxpayers engaged in underground economy activities to comply with their tax obligations and to help us to identify non-compliance.

Use risk assessment to identify non-compliance by employers and GST/HST registrants

We will address non-compliance with remittance, filing, and withholding rules through improvements in our internal quality assurance process as well as improved file selection for examinations.

We will also continue to advance tools and risk-management techniques to improve workload management and optimize our use of resources.

There is an added risk of non-compliance associated with the increase in tax rates as a result of the implementation of HST in British Columbia and Ontario. The CRA will work to make sure that our risk assessment techniques and risk criteria are updated.

Use risk assessment to detect and correct reporting non-compliance

The CRA uses tools and risk-management techniques to direct our compliance efforts to individuals, businesses, and non-profit organizations that are identified as being a high risk for not complying with tax laws.

We are developing an inventory of risk profiling activities to share best practices and to determine if there are any significant gaps within taxpayer segments.

The program initiatives we will pursue over the planning period are listed in the following table.

Priority initiatives

Addressing non-compliance

Reporting compliance (PA4)

Benefit to Canadians

Our aim is to help protect Canada's tax revenue through a range of verification, audit, and enforcement activities, as well as through education. Our activities focus on the accuracy and completeness with which taxpayers determine their tax liability.

Planned spending by program activity

Program activity—Expected results and measures

Addressing non-compliance

Identify aggressive tax planning schemes

Aggressive tax planning is a challenge confronting all developed countries. It can involve very complex structures with both domestic and international elements. The objective of this type of tax planning is to realize tax benefits that were never intended under the normal application of the tax laws.

Identifying aggressive tax planning schemes and evaluating the level of non-compliance associated with these schemes enables the CRA to take appropriate action at an early stage, dissuading taxpayers and their advisors from considering these types of arrangements. Countering abusive schemes at an early stage ensures that the CRA uses its resources in the most efficient and effective manner.

The CRA will continue to use calculated risk assessment, the application of third-party penalties to promoters of abusive schemes, and ongoing collaborative efforts with other tax administrations to identify aggressive tax planning schemes and to take action against those who participate in these types of arrangements.

Identify non-compliance in the underground economy

The underground economy undermines the competitiveness of Canadian businesses because it offers an unfair advantage to those who fail to comply with Canada's tax laws. We use a mix of education, outreach, communication, and compliance actions to combat the underground economy. We also work with other federal agencies and departments, provincial and territorial governments, tax administrations in other countries, international organizations, professional organizations, and key industry groups to share best practices and develop innovative strategies. We carry out identification projects to detect non-filers engaged in underground economy activities and require them to file outstanding tax returns and register for GST/HST. Our auditors work to detect and address underground economy activities and we do industry-specific projects to test innovative compliance approaches. Methods, approaches, and techniques that prove effective are then integrated into our established compliance programs.

Studies show that the underground economy is heavily concentrated in sectors where cash transactions are prevalent. Our underground economy audits focus on identifying unreported income, mainly in industries where there has been a higher level of non-compliance

We will continue to work with provincial and territorial tax administrations to reduce participation in the underground economy through research, information sharing, communication, education, and compliance initiatives. Our underground economy pilot projects help us develop more effective strategies to address the underground economy by identifying and studying emerging issues, gaining industry knowledge, exploring opportunities to gain access to third-party information, and developing and evaluating the effectiveness of compliance risk treatments. Compliance risk treatments flowing from the evaluation of our underground economy pilot projects could include changes in audit techniques, risk assessment, outreach, education, communications, partnerships, and legislation. The Atlantic Region Underground Economy Compliance Measurement Initiative is piloting innovative compliance risk treatments and designing methodologies to measure their impact on future taxpayer compliance behaviour. This project will allow us to develop ways to measure the impact and effectiveness of compliance risk treatments.

Use risk assessment to identify non-compliance by employers and GST/HST registrants

Employers and GST/HST registrants are of particular interest to us because of their responsibility to collect GST/HST and deductions at source for employees.

Over the planning period, we will address non-compliance with remittance, filing, and withholding rules through improvements in our internal quality review process, as well as improved file selection for examinations.

We will also continue to advance tools and risk-management techniques to improve workload management and optimize our use of resources.

Administering the SR&ED Program

The federal Scientific Research and Experimental Development (SR&ED) Program provides broadly based support for all types of SR&ED activities done in Canada.

We are consolidating and clarifying the SR&ED policy and related guidance documents to help clients better understand the SR&ED program. This will enhance accessibility and reduce the administrative burden on SR&ED claimants, particularly small businesses.

We are also developing a training program for the SR&ED program's research and technology staff. Implementation of this program, coupled with quality assurance reviews, is intended to enhance the quality of our SR&ED claims processing and improve the nationwide consistency of our application of law and policy.

Use risk assessment to detect and correct reporting non-compliance

The CRA uses tools and risk-management techniques to direct our compliance efforts (reviews, audits, and investigations) to individuals, businesses, and non-profit organizations that are identified as being a high risk for not complying with tax laws. We are engaged in a business transformation initiative, Compliance System Redesign, that will improve the effectiveness of our compliance programs by improving research and risk-assessment capabilities.

To gauge the effectiveness of our risk-assessment systems, we do periodic evaluations that may include comparing results from our research audits (selected by random sampling) with the level of non-compliance expected through our risk-assessment system. Where we see a divergence in results, we do an analysis to determine the cause and make changes to our systems, as necessary, to ensure continual improvement. Where a risk-assessment system accurately identifies non‑compliance, we should expect to see a high rate of success when taxpayers are selected for audit. We are also developing an inventory of risk-profiling activities to share best practices and to determine if there are any gaps within taxpayer segments.

The implementation of HST in British Columbia and Ontario could increase the rate of non-compliance. The CRA will ensure GST/HST compliance policy and procedures are enhanced, improve risk assessment and select files for audit based on GST/HST specific risks, and develop strategies for GST/HST workload development.

The program initiatives we will pursue over the planning period are listed in the following table.

Priority initiatives

Addressing non-compliance

Appeals (PA5)

Benefit to Canadians

Our commitment is to fairness, and our aim is to provide a timely redress process whereby taxpayers can dispute CRA decisions regarding their income tax, commodity tax, and CPP/EI files, or register their complaints about the services they have received from the CRA.

Planned spending by program activity

Program activity–Expected results and measures

Promoting compliance

Optimize redress workload distribution

The CRA's focus on aggressive tax planning has led to larger volumes of objections from those who participated in them, placing pressure on our business capacity. We will allocate more resources to ensure workloads flow effectively to existing capacity. We will take full advantage of our existing resource base, capitalize on established centres of expertise, and build on the recent business process change that allowed our less complex workload to be distributed nationally.

These steps will help to optimize workload distribution to ensure the best possible match is created between workloads and resolution capacity.

Resolve service complaints

The CRA Service Complaints Program provides taxpayers with a key point of contact within the CRA for service-related issues.

We are currently analyzing trends for service-related issues and this information, in conjunction with findings from the Taxpayers' Ombudsman, will help us to improve service to Canadians.

The program initiatives we will pursue over the planning period are listed in the following table.

Priority initiatives

Promoting compliance

Benefit programs (PA6)

Benefit to Canadians

Our aim is to make sure that timely and correct benefit payments are issued to eligible families and individuals through effective service delivery. In addition, we aim to reduce the overall cost of government through efficiencies obtained by reduced duplication in administration and delivery functions.

Planned spending by program activity

Program activity–Expected results and measures

Administering benefits

Maintain service to benefit recipients

The CRA is a leader in providing tax and benefit services, and we continually explore ways to improve service to Canadians. The telephone remains the most popular channel for benefit recipients to contact us. We will continue to offer timely and accessible telephone services to help them obtain their entitlements. Citizen expectations for public service delivery continue to rise, government program delivery is subject to increasing levels of scrutiny and accountability, and the pace of innovation and the complexity of our delivery infrastructures is increasing. We must address our aging benefit delivery IT infrastructure to continue meeting the evolving expectations of our recipients.

We will improve the functionality of My Account benefits pages and develop new communication products with special emphasis on newcomers to Canada. At the same time, we will explore new ways to provide services to persons with disabilities.

The Automated Benefits Application (ABA) service is one example of a CRA transformational service. Through this co-operative undertaking, which was introduced in 2009-2010 with three provinces and expanded to add two more provinces in July 2010, the CRA receives authorized birth information directly from provincial or territorial vital statistics agencies. This registers Canadian newborns for the federal and provincial benefit programs we administer. Since the ABA service eliminates the need for a separate application, processing time is reduced and recipients get their payments faster.

Over the planning period, we will continue our work with the provinces and territories that have not yet implemented ABA to promote the integration of the Canada Child Benefits application with the provincial and territorial birth registration process.

Manage partnerships

Our flexibility as an agency and the adaptability that we have built into our systems enable us to lever our federal delivery infrastructure to administer a range of programs and other services for client governments. The fact that most jurisdictions have already opted to use our delivery system strongly suggests that it offers important efficiencies in delivering benefits.

Over the planning period, we will maintain the current programs and services that we administer for federal, provincial, and territorial departments. In addition, we will expand our service and data exchange opportunities where possible to allow provinces and territories to deliver their programs more efficiently.

Ensure accurate payments

We are responsible for ensuring sound financial stewardship of the benefit and credit programs that we deliver. This means that the right recipients must get the right payments at the right time.

We carry out validation and control activities specifically targeting accounts identified as high-risk for potential overpayments or underpayments. We also validate information about marital status, children's care situations, and addresses. The information we provide to recipients during validation reviews helps to educate them about their eligibility and entitlement requirements. As well, our enforcement presence is enhanced by our successful efforts in moving cases of misrepresentation toward prosecution.

We have developed and refined a validation strategy over a number of years. It is based on research and risk assessment as well as investigation of trends within the benefits community. Over the planning period, we will continue to improve our targeting to achieve greater program effectiveness. We will also continue to quantify the results achieved by our validation program to make sure that we are applying our resources in the most efficient and effective way.

The program initiatives we will pursue over the planning period are listed in the following table.

Priority initiatives

Administering benefits

Internal services (PA7)

Enabling core business operations

The CRA delivers high-quality tax, benefit, and related services for governments across Canada. To fulfil our considerable mandate, the CRA uses modern management methods and practices that ensure we can comply with the accountability requirements of financial and administrative legislation, regulations, government policies, and directives; use effective human resources practices that keep us competitive in the labour market; make sure that communications at the CRA are consistently well managed and responsive to the information requirements of employees and the public; and sustain and advance our core information technology (IT) functions, which are critical to the delivery of all our programs.

Planned spending by program activity

To enable core business operations, the CRA: provides internal management services; develops and implements communications policies, programs, and services to meet the needs of a diverse public; levers our unique agency status to design and develop our own tailor-made framework and systems for staffing, classification, compensation, labour relations, collective bargaining, training, and human resources policy development; and works to ensure rigour in the CRA's reporting to Parliament, provinces, and territories.

Maintaining our human resources capacity

Plan for and acquire talent

Planning for our talent needs is always important, and even more so in the current environment where budgets are tight. The Agency Strategic Workforce Plan 2010-2011 to 2012-2013 was published in July 2010. It outlines the workforce goals and objectives the CRA will need to reach in this three-year period to support our business priorities. The plan will be updated annually to make sure that it responds to the current environment and business direction.

This integrated planning culture will also be deployed throughout the organization by the development of regional and branch workforce plans.

The implementation of the staffing pre-qualification processes completed last year will contribute to reducing the time to staff. In addition, the CRA will continue to work on e-Resourcing, and will encourage greater use of online assessment tools and standardized tools for external recruitment.

Strategic recruitment is crucial to make sure that we are positioned to recruit the best talent available, because the CRA will continue to compete with the private and public sectors for talent. We will review and analyze branch and regional workforce plans to identify national risk areas and develop a CRA-wide recruitment strategy.

Develop talent

Pending retirements create a risk of corporate knowledge loss since many future retirees are life-long CRA employees who have accumulated a wealth of technical knowledge and subject-matter expertise. There will be a focus on succession planning and knowledge transfer to mitigate that risk.

Knowledge transfer is not the only consideration in developing talent. Changes brought about by a global economy and an increased reliance on technology have an impact on the complexity of certain work performed within the CRA. The Agency Learning Priorities tool will address the competency gaps that surface in workforce plans.

Retain and mobilize talent

Our large organization creates many career opportunities for employees. Recent demographic data supports this: in 2009-2010, our internal mobility rate (including promotions, transfers, and lateral moves) was 14.7%. This demonstrates that employees seize the opportunities available to them and enhance their breadth of knowledge. The challenge lies in balancing the optimal amount of breadth with an acceptable level of depth that is crucial to maintaining our expertise in tax administration.

Sustain a healthy, respectful, and innovative workplace

A healthy and respectful workplace is crucial to keep employees. We have traditionally enjoyed a high retention rate (95%). However, this trend may change in the next years as society and the labour market evolve.

We must make sure that our workplace is representative of our values and that we maintain the trust and respect of the Canadian taxpayers. At the same time, we want to be at the forefront of workplace trends and offer an innovative work environment that embraces technology. This will support us in staying an attractive employer.

Transition of provincial employees to the CRA

As a result of agreements between the Government of Canada and the governments of Ontario and British Columbia to join the harmonized sales tax framework, the CRA has signed the human resources agreements with each of the provinces. Consequently, the CRA has committed to offering to up to 1,564 provincial employees, affected by tax administration changes in these provinces, meaningful employment within the CRA.

In November 2010, the CRA successfully integrated the first waves of provincial employees in Ontario and British Columbia. Next waves are scheduled for July 2011, March 2012, and July 2012.

IT responsiveness and sustainability

Today more than ever before, Canadians expect the tax and benefits delivery system to be interwoven with information technology. Processes key to the CRA's mission are dependent on automation and computerized processing. This reliance on technology will undoubtedly increase as the CRA continues to successfully implement its business strategies related to the up-take of electronic services. The CRA will continue to participate as a member of the Cyber Authentication Renewal Program to provide secure access and lay the groundwork for the continued expansion of the suite of electronic services the CRA offers.

Sustain our IT applications and infrastructure

Although the CRA identifies both IT sustainability and IT responsiveness as ongoing corporate risks, the CRA is confident there is oversight and accountabilities on the implementation of mitigation plans. The focus of the CRA continues to be excellence in IT program delivery, recognizing limitations of the current fiscal environment, as well as new demands to help meet appropriate levels of service.

Accountability, oversight, and operational efficiency

Certify the effectiveness of internal controls

The CRA is diligently working toward meeting the requirements of Treasury Board's newly established financial management policy framework and the new accounting officer provisions of the Financial Administration Act. In particular, the Treasury Board Policy on Internal Control requires that new information on the effectiveness of the CRA's internal controls over financial reporting be provided as part of the CRA's financial statements, beginning in 2010-2011. This information includes a revised statement of management responsibility signed by the chief executive officer and the chief financial officer, as well as a summary appended to the CRA's financial statements identifying weaknesses and management action plans to achieve the required improvements.

Implement the Emergency Management Program Strategy

The introduction of the Emergency Management Act 2007 and the Federal Policy for Emergency Management has prompted all federal organizations to refine and enhance their emergency management programs to align with the federal direction in building organizational resilience, and to strengthen their ability to mitigate, respond to and manage emergencies.

The CRA administers social benefits through its tax system on behalf of other federal departments and agencies, provinces, and territories, and is also committed to maintaining the integrated IT infrastructure that supports the Canada Border Services Agency border protection functions. These two critical services must be delivered with little or no disruption or downtime during an emergency. To effectively address this need, the CRA conducted a comprehensive review of emergency management practices and developed the Emergency Management Program Strategy 2009-2010 to realign the organization with the new federal requirements while continuing to strengthen the existing emergency management governance and capacity within the CRA.

Protection and management of information

Advance the Internal Fraud Control Program

All organizations face the risk of internal fraud because some individuals will be motivated to commit fraud given the opportunity. As part of its broader integrity framework, the CRA has always had in place a discipline policy applicable to all employees with prescribed corrective measures up to and including suspension and termination in cases of founded employee misconduct. In support of the new Internal Fraud Control Policy, the Agency is implementing a multi-year Internal Fraud Control Program.

The goal of this program, which is now in its third year, is to further ensure that the CRA continues to take all reasonable measures to safeguard the assets, resources, information and reputation of the organization. This will assist the CRA in meeting its stewardship responsibilities, and fostering and sustaining the trust of taxpayers in the CRA.

Advance the Identity and Access Management initiative

The CRA maintains one of the Government's largest repositories of personal information. Our data holdings are voluminous and highly sensitive. Given the size and nature of the CRA's operations, the Agency wants to ensure that there is no unethical behaviour by its employees resulting in inappropriate accesses, use and disclosure of information entrusted to the CRA.

The IAM will help continue to ensure that only authorized users have access to CRA systems, and that their application accesses are the appropriate minimum required to do their work, thus reducing the risk of improper access to taxpayer data and system resources.

In addition to enhancing security, the IAM will continue to ensure compliance with legislative requirements, provide auditing and monitoring capabilities, contribute to cost containment of IT administration and service desks, and increase user accountability and productivity.

Develop and Implement a CRA solution for the storage and management of physical records

Governed by a Memorandum of Understanding with CRA, Library and Archives Canada stores and manages 550,000 cubic feet of semi-active CRA paper records. Library and Archives Canada will discontinue the provision of these services and is working on a transition timeline of two to four years. This will alter records management services related to the CRA's T1, T2, T3, and GST returns. The CRA is in the process of identifying requirements and developing options to manage its record storage requirements and the results will be brought forward to senior management in spring 2011.

Protect and Manage our IT and information assets

Since the CRA's ability to maintain trust, transparency, and accountability is paramount to our integrity, the IT community has a collective responsibility for keeping IT assets current and secure.

Given that the CRA has a significant Internet presence and also manages confidential taxpayer data, we will strive to meet higher standards of security and service and be the leader in achieving operational excellence with regard to protecting our data and IT assets. We will evolve our IT security program to make sure that the CRA continues to be at, or above, the IT security recommendations set out by the Government of Canada. In a continuous effort to maintain our high degree of security distinction, we will continue to implement a multi-year Secure Data Network and Assets Program.

The CRA collects and processes huge volumes of information such as tax returns and benefit applications. We also create information such as publications for Canadians, corporate reports, and the many e-mails shared internally in the course of doing business. The CRA has a duty to ensure that the information in our care support not only our operational business activities, but also serves as evidence of our decisions and actions. We must also ensure that the information is of good quality and meets the needs of the many programs across the and other government organizations that use the information. Our ability to effectively manage the information has a direct impact on knowledge management within the CRA.

The CRA has identified the improvement of record keeping as a key focus for the management of business information. We will continue to advance the maturity of our record keeping by making progress on the delivery of the Information Management guidance, products, services and tools necessary to cost-effectively manage paper and electronic documents and email, in accordance with legislative and policy requirements.

CRA Sustainable Development (SD) Strategy 2011-2014

Within the context of a socio-economic mandate, successive SD strategies at the CRA have focused on augmenting our accountability for our environmental responsibilities. Since its first SD strategy in 1997, the CRA has been proactive in pursuing targets to green its internal operations. This has placed us in a favourable position to achieve the federal strategy targets, which are:

- achieve six green procurement targets;

- recycle all surplus electronic and electrical equipment in an environmentally sound manner;

- reduce internal paper consumption per employee by 20%;

- achieve a 8:1 ratio of employees to printing units;

- adopt a guide for greening meetings and events; and

- reduce greenhouse gas emissions from fleet vehicles by 17% by 2020 from 2005-2006 levels.

For additional information on the CRA's targets for greening government operations, please refer to Section III of the RPP.

The goals of the CRA strategy will position the SD program to provide greater support to CRA business objectives, and to further integrate SD into our corporate culture by:

- measuring and communicating the SD benefits of CRA programs and services;

- using the SD message to promote the CRA as a great place to work; and

- further integrating SD into the CRA accountability processes.

The Internal Services initiatives we will pursue over the planning period are listed in the following table.

Priority initiatives

Maintaining our human resources capacity

IT responsiveness and sustainability

Accountability, oversight, and operational efficiency

Protection and management of information

Section III: Supplementary Information

Financial Highlights

The future-oriented financial highlights presented within this Report on Plans and Priorities are intended to serve as a general overview of the Canada Revenue Agency's (CRA) financial position and operations. These future-oriented financial highlights are prepared on an accrual basis to strengthen accountability and improve transparency and financial management.

Future-oriented financial statements can be found on the CRA's website.

| Assets | ||

| Financial assets | ||

| Non-financial assets | ||

| Total | ||

| Liabilities | ||

| Net Liabilities | ||

| Total |

Capital assets totalling $485.5M comprise most of the Agency's assets for 2011-2012, with software ($441.5M) being the largest asset class, as the CRA looks to take advantage of the newest technology in delivering its programs and services to Canadians. Net liabilities represent liabilities incurred by the Agency which are expected to be funded by appropriations in future years, as they are paid.

|

|

|

|

|

| Total Expenses | |||

|

|

|

|

|

| Total Non-Tax Revenues | |||

| Net Cost of Operations |

The chart below outlines the Agency's future-oriented total expenses for 2011-2012. It is projected that total expenses will be $4,682.2M for the coming fiscal year.

Most of these expenses ($3,150.8M) will be directed at enhancing the CRA's capability to achieve its first strategic outcome: Taxpayers meet their obligations and Canada's revenue base is protected. The CRA will focus on Tax Integrity and Strengthening Services. Tax Integrity will be achieved by making it harder to be non-compliant by actively and consistently addressing the promotion of non-compliance and improving communication and information-sharing with federal and international stakeholders to permit rapid response to emerging compliance threats. Strengthening Service will be achieved by making it easier for taxpayers to comply by carrying out the CRA's Service Strategy to expand self-service options, optimize telephone service, and fine-tune the outreach and communication efforts.

$152.3M in expenses will be used to meet the CRA's second strategic outcome: Eligible families and individuals receive timely and correct benefit payments. To maintain a strong performance in benefit programs delivery, the CRA's focus will mostly be on Strengthening Service and Benefits Validation. Strengthening Service will be achieved by improving communications and enhancing electronic service offerings. Benefits validation will be achieved by creating a credible enforcement presence and by educating benefit recipients about their rights and obligations.

$3.8M in expenses will be used to support the CRA's third strategic outcome: Taxpayers and benefit recipients receive an independent and impartial review of their service-related complaints with the Taxpayers' Ombudsman activity.

Finally, $1,375.3M in expenses will be used in support of internal services. Internal services activities are those that apply across the organization and not to a specific program. These include activities such as Management and Oversight Services; Communications Services; Legal Services; Human Resources Management Services; Financial Management Services; Information Management Services; Information Technology Services; Real Property Services; Materiel Services; Acquisition Services; and Travel and Other Administrative Services.

The chart below outlines the CRA's future-oriented total non-tax revenues for 2011-2012. It is projected that total non-tax revenues will be $606.7M for the coming fiscal year. The majority, 52%, of these non-tax revenues ($316.8M) are revenues credited to Vote 1 and are expected to come from the administration of the Employment Insurance Act ($177.2M) and the Canada Pension Plan ($139.6M). While 38% ($230.6M) are non-tax revenues available for spending and are expected to come from service fees to other government departments ($154.6M), administration fees for provincial programs ($72.1M), ruling fees to taxpayers ($1.6M), and other miscellaneous respendable fees and changes ($2.3M). The remaining 10% ($59.3M) are non-tax revenues not available for spending and will come from the recovery of employee benefit costs relating to non-tax revenues credited to Vote 1 and revenues available for spending ($56.9M) as well as other miscellaneous non-respendable non-tax revenues ($2.4M).

List of Tables

The following tables are available electronically on the Treasury Board of Canada Secretariat's Web site.

Details on Transfer Payment Programs

Sources of Respendable and Non-Respendable Non-Tax Revenue

The following tables are available electronically on the CRA Web site.

Agency Planned Spending and Full-Time Equivalents

Greening government operations

For more information on greening government operations at the CRA, please go to the Treasury Board of Canada Secretariat's Web site.

Internal audits and evaluations

For more information on the CRA's Internal Audits and Evaluations, please go to the Treasury Board of Canada Secretariat's Web site.

Section IV :Other Items of Interest

Strategic Environmental Assessments

Given its administrative mandate, the CRA has not conducted Strategic Environmental Assessments (SEA) to date. If required, the CRA will conduct SEAs, with the support of the Canadian Environmental Assessment Agency.

Additional information is available electronically as follows:

- complete details on the FSDS

- the CRA's contribution to the FSDS and other SD initiatives – refer to the Greening Government Operations Supplementary Tables on the Treasury Board Secretariat website.

- information on the CRA SD Strategy 2011-2014 and our SD Performance Report

- details on CRA activities that relate to the environmental, economic, and social pillars of sustainable development – please visit the CRA SDWeb site.

Service Standards at the CRA

Our service standards regime is a vital and integral part of our planning, reporting, and performance management processes. Meeting our service standards targets demonstrates that we are responsive to the needs of taxpayers and benefit recipients. This helps establish credibility in our operations and contributes to increasing the level of confidence that Canadians can place in government.

For more information on our Service Standards, please visit the CRA Web site.

Service Standards

Table 1: Taxpayer and Business Assistance (PA1) (Enquiries and Information Services)

Table 2: Taxpayer and Business Assistance (PA1) (Legislative Policy and Regulatory Affairs)

Table 3: Assessment of Returns and Payment Processing (PA2)

Table 4: Accounts Receivable and Returns Compliance (PA3)

|

NONE Footnote 1

|

|

|

Table 5: Reporting Compliance (PA4)

Table 6: Appeals (PA5)

Table 7: Benefit Programs (PA6)

Table 8: Internal Services (PA7)

Three-Year Plan for Transfer Payment Programs

Under section 6.6.1 of the Policy on Transfer Payments (PTP), deputy heads are required to provide to the Treasury Board Secretariat (TBS) by April 1 of each year a three-year plan for their transfer payment programs (TPPs). For more information, please go to the CRA Web site.