Guide to Debt Deletion

1. Date of publication

This guide was published on .

2. Application, purpose and scope

This guide applies to the organizations listed in section 6 of the Policy on Financial Management and to debts resulting from receivables as defined in the Directive on Public Money and Receivables.

The purpose of this guide is to provide departments with information on the deletion of debts owing to the Crown, in accordance with the Financial Administration Act (FAA).

This guide supports the debt deletion authorities provided in the FAA under the following four forms of debt deletion:

- write-off under section 25 of the FAA and the Debt Write-off Regulations, 1994

- remission under section 23 of the FAA

- forgiveness under section 24.1 of the FAA

- waiver or reduction of interest and/or administrative charges under section 155.1 of the FAA and sections 9 and 12 of the Interest and Administrative Charges Regulations

This guide complements the act, the regulations and the directive; it does not present new mandatory requirements.

This guide does not cover the following:

- debt arising from receivables recorded as a result of entry errors in accounting, or debts that have no legal basis; the required adjustments to a department’s receivables due to entry errors are administrative and do not require legislative or regulatory authority

- other acts of Parliament (for example, Bankruptcy and Insolvency Act, Income Tax Act, Service Fees Act) that provide the authority to ministers or an entity to approve the write-off, remission or forgiveness of specific debts, obligations or claims (which may involve conditions other than those specified in the FAA and/or the Debt Write-off Regulations, 1994)

Section 3 provides the context that led to the adoption of the controls required in the debt deletion process.

Section 4 provides details on how debts are defined and classified within the Government of Canada.

Section 5 discusses the different debt deletion authorities provided under the FAA.

Section 6 discusses special considerations regarding debt deletion:

- accrual of interest on outstanding receivables

- application of the Low-Value Amounts Regulations

- source of funds

- transfer payments

- statute-barred limitations

- fees and other charges owed to departments

- deleting a revolving fund’s accumulated deficit

Section 7 discusses the accounting and reporting for debt deletion transactions.

Appendix A provides a summary of the various debt deletion mechanisms.

Appendix B illustrates a debt deletion decision tree.

Appendix C provides additional guidance on the application of debt deletion authorities under the FAA.

3. Context

A debt owing to the Crown arises from a wide variety of transactions between the government and external parties. Such transactions may include tax and non-tax accounts receivable as well as amounts due from loans, investments and advances that have been made by the government. When it is determined that the debt cannot be settled in full (for example, it is determined to be uncollectible, unreasonable, unjust, or not in the public interest), departments are to take timely action to ensure that the amounts are deleted from the accounts of Canada.

There is a detailed system of statutory and regulatory controls that must be followed to ensure that:

- the debt deletion process is managed with due diligence

- receivables are not removed from the accounts of Canada without following the appropriate process

Various mechanisms for deleting a debt can be found in specific program legislation under which the debt was created (for example, the Income Tax Act) or the FAA. For additional guidance on the application of specific program legislation, departments may consult with their legal services unit.

It should be noted that the option to write off debts is reserved for the following:

- debts that are determined to be uncollectible

- debts for which the administrative expense of collection would not be justified in relation to the amount of the debt

- there is a compromise settlement for the debt, or when a present value payment has been accepted as full settlement of the debt

Since the requirements of the Debt Write-off Regulations, 1994 relate to the collectibility of the debt, write-off under the regulations is not appropriate if the reason for not collecting the debt is because collection would be considered unreasonable, unjust or not in the public interest. Other means of debt deletion (for example, remission or forgiveness) are available in such cases.

Further guidance is provided in Section 5.

4. Definition and classification of debt

This section provides the definition of a debt owing to the Crown, identifies when the debt deletion authorities under the FAA would apply, and explains how debts are classified within the Government of Canada.

Debt is generally defined as an obligation due to Her Majesty or a claim by Her Majesty.

4.1 When do the debt deletion authorities provided under the FAA apply?

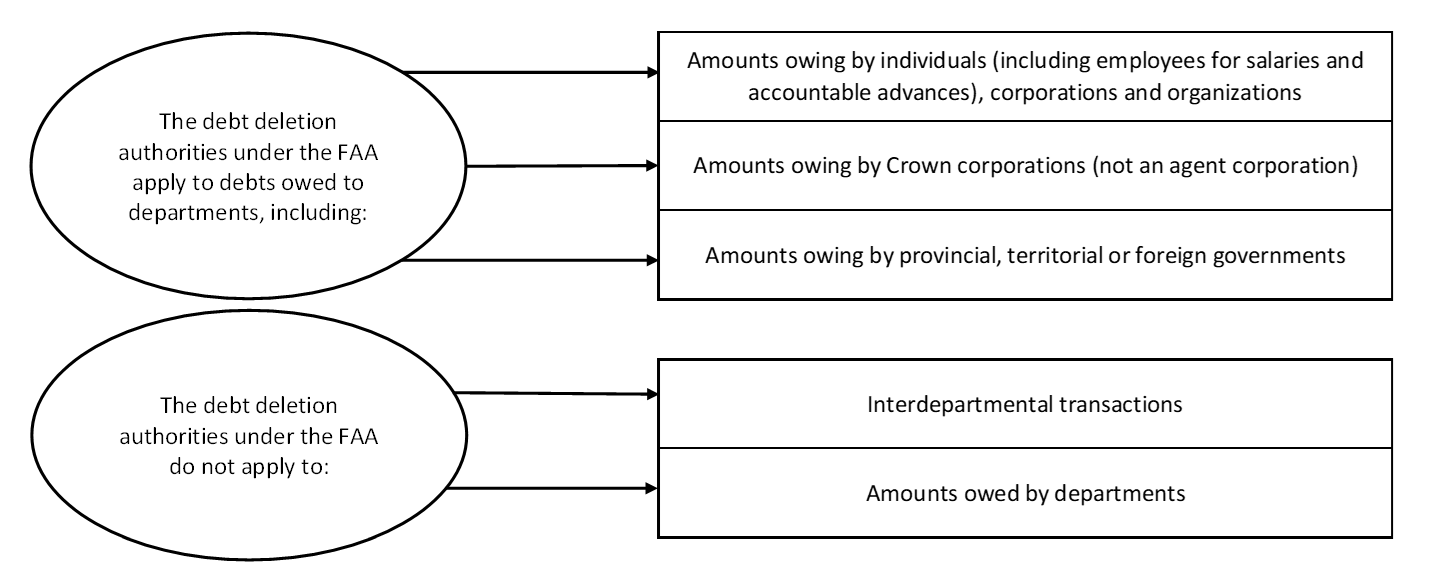

Figure 1 summarizes the application of the debt deletion authorities provided under the FAA (that is, what amounts would be considered a debt owing to the Crown versus amounts not considered a debt owing to the Crown). Explanatory information for Figure 1 is provided in subsection 4.1.1 and subsection 4.1.2.

Figure 1 - Text version

The debt deletion authorities under the FAA apply to debts owed to departments, including amounts owing by individuals (including employees for salaries and accountable advances), corporations and organizations, amounts owing by Crown corporations (not an agent corporation), and amounts owing by provincial, territorial or foreign governments.

The debt deletion authorities under the FAA do not apply to interdepartmental transactions and amounts owed by departments.

4.1.1 Application of the debt deletion authorities under the FAA

The following amounts would generally be considered as debts owing to the Crown and therefore would fall under the debt deletion authorities provided in the FAA:

- amounts owing by individuals, corporations and organizations: the debt deletion authorities under the FAA apply to amounts owed to departments by individuals (including outstanding overpayments made to employees related to salaries or any other employment-related allowances), corporations and organizations; the definition of “department” is provided in section 2 of the FAA

- amounts owing by Crown corporations (not an agent corporation): the debt deletion authorities under the FAA apply to amounts owed to a department by a Crown corporation that is not an agent corporation; Crown corporation and agent corporation are defined in section 83 of the FAA. Crown corporation means a non-agent corporation throughout this guide.

- amounts owing by provincial, territorial or foreign governments: the debt deletion authorities also apply to amounts owed to a department by a provincial, territorial or foreign government

It is strongly recommended that departments consult with their legal services unit to determine whether their situation would be subject to the debt deletion authorities under the FAA or if there is another act of Parliament that would apply.

4.1.2 When would the debt deletion authorities under the FAA not apply?

The following amounts would not be considered as a debt owing to the Crown, and therefore would not fall under the debt deletion authorities provided in the FAA:

- interdepartmental transactions: the debt deletion authorities under the FAA do not apply to interdepartmental receivables; any amount receivable by one department from another is not considered a debt owing to the Crown as it is an internal transaction (that is, there is no net impact or “new” debt created for the Crown as a result of these receivables)

- amounts owed by departments: the debt deletion authorities under the FAA do not apply when a department owes amounts to third parties, for example, for the payment of invoices from suppliers or the payment of salaries to employees; these transactions do not result in a debt owed to the Crown as they involve payments made by the Crown

4.2 Types of debt

When deleting a debt under the FAA, departments need to first determine the type of financial transaction that generated the debt. There are two types of transactions: budgetary and non-budgetary. In general, all expenditures must be approved by Parliament, and classifying debt into these two categories ensures that the proper authority is obtained for all spending. The distinction between budgetary and non-budgetary debts reflects the nature of the expenditure and does not stem from accrual accounting. In both cases, the transaction may result in a financial asset for financial accounting purposes. Further explanations are provided in subsection 4.2.1 and subsection 4.2.2.

4.2.1 Budgetary debt

Budgetary transactions affect the government’s annual surplus and deficit. Amounts owing to departments under budgetary transactions usually consist of debts resulting from departmental activities that are financed by departmental budgetary appropriations approved under an appropriation act (for example, operating, transfer payment or capital votes) or through a statutory authority pursuant to specific legislation. Such amounts may include both salary-related and non-salary-related amounts.

In other words, a budgetary debt usually arises as a result of the normal operations of the government that are financed through expenditure votes (for example, fees payable, taxes or amounts to be received under a contract), or where the amounts originated from an expenditure vote where the funds were generally not expected to be repaid to the department but become repayable in the future (for example, a salary overpayment).

4.2.2 Non-budgetary debt

Non-budgetary transactions affect the composition of the financial assets of the government. They usually consist of loans, investments and advances. The authority may be provided by voted appropriations (for example, a vote starting with the letter “L” is used to differentiate it from regular voted, budgetary funds). Like budgetary debts, such funds are authorized through an appropriation act or statutory authority pursuant to specific legislation. An example of these types of transactions include (but are not limited to) a loan that is expected to be repaid or an advance charged to a working capital advance account. A working capital advance account may be created as a non-budgetary authority by some departments to finance temporary advances to foreign missions or to departmental personnel (for example, salary, benefits, travel and other miscellaneous claims).

In other words, a non-budgetary debt is a disbursement of money that does not originate from an expenditure vote. The expenditure increases the financial assets of the government (for example, immigration loans for transportation and assistance). When a non-budgetary debt is deleted, it means that the financial asset will never be collected; therefore, there is no longer a future inflow of cash to the government, meaning that the funds are in essence spent. As a result, before a non-budgetary debt is to be deleted, it must be converted to a budgetary debt by including it as a budgetary expenditure in an appropriation act or other act of Parliament.

5. Types of debt deletion authorities provided under the FAA

This section outlines the debt deletion authorities available under the FAA and how they can be practically exercised. Appendix B includes a debt deletion decision tree that may be used as a preliminary step to help determine the appropriate debt deletion authority that may be used. Additional guidance on the application of debt deletion authorities under the FAA is provided in Appendix C.

5.1 Debt write-off

Debt write-off under section 25 of the FAA includes the removal of a debt in whole or in part from the accounts of Canada (for example, the accounts receivable ledgers, aging schedule). It does not legally extinguish the debt or obligation. This means that the Crown retains its rights to collect or recover the debt in the future and that the debt could be reinstated at any time, subject to applicable limitation periods. The only exceptions are compromise settlements, or when a present value payment has been accepted as full settlement of the debt. In these cases, the debtor is released from any obligation to pay the remaining balance (in other words, the debt is extinguished) by virtue of the arrangement entered into with the debtor.

Both budgetary and non-budgetary debts can be written off. However, according to the Debt Write-off Regulations, 1994, debt write-off is reserved for:

- debts that are determined to be uncollectible

- debts for which the administrative expense or other costs of collecting the debt are not justified in relation to the amount of the debt, or in cases where there is a compromise settlement or a present-value amount is accepted as full settlement of the debt

5.1.1 Authority to write off debts

The requirements of the regulations and the FAA must be complied with before a debt can be written off. There are different requirements depending on whether the debt is salary-related or non-salary-related and whether it is budgetary or non-budgetary.

Budgetary non-salary debt consists of amounts owed to the Crown that are not associated with expenditures related to salaries or other employment-related advances (such as a travel advance). Such debt may include amounts owed to the Crown from the sale of goods, the provision of services or the use of facilities.

A budgetary non-salary debt can be written off (including any related outstanding interest) under section 4 of the regulations in accordance with subsection 4(2), 4(3) or section 6. Treasury Board approval is not required to write off a budgetary non-salary-related debt.

Budgetary salary debt and accountable advances consist of amounts owed to the Crown that are related to overpayments of salaries and other employment-related allowances made to an employee, as well as accountable advances as defined in the Accountable Advances Regulations. Such advances may include amounts paid to an employee at the incorrect salary rate, or the outstanding balance of an unused travel advance issued to an employee.

Budgetary salary-related debts and accountable advances (and any related outstanding interest) can be written off under section 4 of the regulations in accordance with subsections 4(2) or 4(3) or section 6. However, these debts are also subject to the additional requirement in subsection 5(1) of the regulations which provides that Treasury Board approval is required.

However, as set out in subsection 5(2) of the regulations, Treasury Board approval is not required if the employee’s debt was discovered after their employment was terminated and all termination benefits have been paid.

Non-budgetary advances, loans and investments consist of amounts owed to the Crown that have resulted from a loan, advance or investment. These may include, for instance, loans issued through a departmental program that provides financial assistance to Canadians for a specific purpose.

Non-budgetary salary-related debts and accountable advances (and any related outstanding interest) can be written off under section 4 of the regulations in accordance with subsection 4(2) or 4(3) or section 6 (for example, if a debtor defaults on all or a portion of the repayment of a loan, advance or investment). However, these debts are also subject to the additional requirement in subsection 25(2) of the FAA. Subsection 25(2) of the FAA requires non-budgetary debts to be included as a budgetary expenditure in an appropriation act (that is, a new budgetary vote must be created in the Estimates), or any other act of Parliament before it is written off. In practice, the new budgetary vote is most often included in an appropriation act. Treasury Board approval is required to include the amount of the debt and any related outstanding interest in an appropriation act.

5.1.2 Under what circumstances can a debt be written off?

The authority to write off a debt stems from section 4 of the Debt Write-off Regulations, 1994 and provides that all or a portion of a debt may be written off if one or more of the situations below exist.

-

The debt has been determined to be uncollectible: Subsection 4(1) applies when a debt is considered uncollectible and if all three of the following criteria under section 6 of the Debt Write-off Regulations, 1994 are met:

- There is evidence that recovery of the debt was unsuccessful after all reasonable collection action has been taken and all possible means of collection have been exhausted.

- There is no possibility of any additional recoveries through set-off against future amounts that would be owing to the debtor (for example, income tax refund, any other government-issued payment).

- There are no other means to enforce further recovery actions and at least one of the nine conditions listed under subsection 6 (c) applies. Such instances include but are not limited to the following: debtor cannot be located, debtor is deceased and there is no estate, debtor is bankrupt, or debt is considered statute-barred.

It is important to note that if no collection efforts were made, the debt would not be eligible for write-off under section 4(1) of the regulations unless collection actions are not possible or are unreasonable. “Unreasonable” in this context is normally interpreted to mean extraordinary measures (such as commencing legal proceedings in foreign jurisdictions). In most cases, asking a debtor to pay an outstanding debt would not be considered an unreasonable collection action.

- The cost of collecting the debt outweighs the amount of the debt or the probability of collection: Subsection 4(2) applies when the cost to collect the debt (for example, legal fees, collection agency fees) is greater than the amount of debt that could be recovered. When exercising this authority, departments are expected to have a rigorous cost-benefit analysis that documents and justifies the application of subsection 4(2).

- The department has agreed to a full settlement on the present-value payment of the debt: Subsection 4(3)(a) applies when a present-value payment has been accepted as full settlement of the debt. The debtor is released from any obligation to pay the remaining balance (in other words, the debt is extinguished) and the remaining balance of the debt is then eligible to be written off. Additional information can be found in subsection 7.2.6 of the Guide to Managing Receivables.

-

There is a compromise settlement for the debt: Subsection 4(3)(b) applies when the debtor has negotiated a compromise settlement with the government pursuant to an applicable authority where they are required to repay only a partial amount (or none) of the debt owing. Compromise settlements are appropriate only if the cost of litigation outweighs the amount that is expected to be recovered. If any other factors are driving the decision, then remission or forgiveness is more appropriate.

When a compromise settlement is reached, the debtor is released from any obligation to pay the remaining balance (in other words, the debt is extinguished), and the remaining balance of the debt is then eligible to be written off. Additional information can be found in subsection 7.2.7 of the Guide to Managing Receivables.

It is strongly recommended that departments consult with their legal services unit when considering the negotiation of a compromise settlement.

Note that the requirements of the regulations relate to the collectibility of the debt. Write-off under the regulations is not appropriate if the reason for not collecting the debt is because collection would be considered unreasonable, unjust or not in the public interest. Other means of debt deletion (for example, remission or forgiveness) are available in such cases.

5.1.3 Oversight of debt write-off

Procedures for the control and write-off of a debt

Sections 7 and 8 of the regulations provide the procedures that must be followed for the control and write-off of a debt.

- All debt must be controlled through regular reporting to management (including the balance, age, amount collected to date, accrued interest and credit information and risk) and in the appropriate department’s accounts until they are either collected or written off.

- A formal review process must be established by the appropriate departmental minister or deputy head on behalf of the minister.

- If the amount to be written off is greater than $25,000 (or any other lower threshold set by the departmental minister or deputy head), it must be referred to a review committee, who will then make recommendations to the minister (or other officer authorized by the minister) regarding the proposed write-off.

- A review committee shall consist of at least three public officers, at least one of whom is not involved in the creation, establishment or any collection actions of the debt that is proposed to be written off.

Retention of information and records

Section 9 of the regulations addresses the record retention requirements for debt being written off. All information and records need to be retained until:

- all audit procedures are completed and other administrative requirements with respect to the debt write-off are satisfied

- there is no longer any probability of future set-off

- the limitation period for initiating any legal action regarding the determination of the amount or recovery of the debt has expired

5.2 Debt remission

Remission under section 23 of the FAA legally extinguishes the debt (including any related outstanding interest), waives the right of the Crown to reinstate the debt, and allows both the Crown and the debtor to permanently remove the debt from their accounts.

Remission under section 23 of the FAA relates to a broad category of debts but excludes non-budgetary expenditures. Non-budgetary expenditures are subject to forgiveness under section 24.1 of the FAA (or write-off under section 25 of the FAA, if applicable).

Debts owed by a Crown corporation to a department are also subject to forgiveness under section 24.1 of the FAA. However, budgetary debts owed by a Crown corporation are not specifically excluded from the application of section 23 of the FAA. As a result, budgetary Crown corporation debts can be forgiven under section 24.1 of the FAA or by a remission order under section 23 of the FAA.

A remission is operationalized through an order-in-council that is published in the Canada Gazette, Part II. As a result, remissions can be precedent-setting from a policy standpoint, and a rationale is needed for each decision (for example, if two debts of a similar nature are subject to different treatment); otherwise, the decision could seem arbitrary and may be subject to legal challenge.

5.2.1 Under what circumstances can a debt be remitted?

Under section 23 of the FAA, remissions apply only to budgetary debts, including the following:

- taxes, penalties and associated interest

- other debts (including salary-related or non-salary-related) and associated interest

Section 23 of the FAA also provides the criteria under which a debt can be remitted. The criteria include situations where collection of the amounts would be considered:

- unreasonable or unjust, which may apply in any of the following instances:

- compassionate reasons (severe hardship)

- equity (unfairness resulting from errors)

- legislative or regulatory considerations (anticipation of a change in the law)

- policy considerations (unfairness or unintended results), or

- not in the public interest, which usually involves federal–provincial relationships, or relationships with Indigenous groups, or items that have broader public relations or public policy implications rather than the specific impact on a particular individual

5.2.2 Authority to remit debt

Section 23 of the FAA provides that taxes, penalties and associated interest may be remitted by the Governor in Council on the recommendation of the appropriate minister. A Governor in Council submission is required. Other debts and associated interest may be remitted by the Governor in Council on the recommendation of the Treasury Board.

Where a recommendation from the Treasury Board is required, departments must prepare a Treasury Board submission and a Governor in Council submission. Once made, the Order and associated explanatory note must be published in the Canada Gazette, Part II.

5.3 Debt forgiveness

Forgiveness under section 24.1 of the FAA legally extinguishes the debt (and any related outstanding interest), waives the right of the Crown to reinstate the debt, and allows both the Crown and the debtor to permanently remove the debt from their accounts.

Debt forgiveness only applies to non-budgetary debts and debts owing by a Crown corporation to a department. Before a non-budgetary debt can be forgiven, a budgetary appropriation must be charged for the amount of the debt and associated interest.

5.3.1 Under what circumstances can a debt be forgiven?

There are no set criteria in the FAA for determining when a debt may be forgiven. This is because it is Parliament’s decision to forgive the debt, and Parliament must have the authority to do so under whatever circumstances it deems appropriate. However, in practice, departments who wish to seek debt forgiveness should be guided by the criteria for remission under section 23 of the FAA (that is, collection would be unreasonable, unjust or not in the public interest, as set out in subparagraph 5.2.1 of this guide).

5.3.2 Authority to forgive debt

Forgiveness under section 24.1 of the FAA requires parliamentary approval through legislation such as an appropriation act or any other act of Parliament. In practice, forgiveness is most often included in an appropriation act. Treasury Board approval is required to include the amount of the debt and any related outstanding interest in an appropriation act.

Forgiveness under section 24.1 of the FAA may be used for the following types of debt:

- Non-budgetary debt that is defined as a debt included in the Statement of Assets and Liabilities where forgiveness would require a charge to a department’s budgetary appropriations. For example, such debt may include outstanding loans, advances or investments owed to a department, or non-budgetary debts owed by a Crown corporation to a department.

- Budgetary debt owed by a Crown corporation to a department. For example, a department may perform services for which a fee is charged to all users, such as individuals and Crown corporations. If the services used and provided in order to generate the fee were paid from budgetary funds (that is, voted expenditures through appropriations), then any fee owed by the Crown corporation to the department would be considered a budgetary debt.

5.4 Waiver or reduction of interest and/or administrative charges

Interest and/or administrative charges related to dishonoured instruments (for example, non-sufficient funds (NSF) cheques) may be waived or reduced by the appropriate departmental minister (or any public officer authorized by that minister in writing) in certain situations as set out under sections 9 and 12 of the Interest and Administrative Charges Regulations. Additional information can be found under section 9 of the Guide to Interest and Administrative Charges.

6. Special considerations

6.1 Accrual of interest on outstanding receivables

The Interest and Administrative Charges Regulations developed under subsection 155.1(6) of the FAA prescribe the rates and the general conditions under which departments must charge interest on overdue non-tax receivables and charge administrative fees where any instrument payable by any individual or business to the Crown is dishonoured (for example, a dishonoured cheque due to insufficient funds).

The Interest and Administrative Charges Regulations apply when no other act, regulation, order, contract or arrangement is in place that covers the payment of interest to the Crown. When an instrument is silent on the payment of interest on overdue accounts or for late payments, the regulations automatically apply. Where the regulations apply, interest must be accrued on overdue receivables starting from their due date (subject to any applicable exceptions).

Under certain limited circumstances, interest accrued or administrative charges imposed under the Interest and Administrative Charges Regulations can be waived or reduced. When a waiver is not possible, the debt may be deleted by leveraging one of the other debt deletion authorities mentioned above, if applicable.

Detailed guidance on applying the Interest and Administrative Charges Regulations is provided in the Guide to Interest and Administrative Charges.

6.2 Are the low-value amounts thresholds applicable?

Amounts owed to the Crown are subject to the provisions for small amounts set out in section 155.2 of the FAA and in the Low-Value Amounts Regulations. The regulations have broad applicability and generally take precedence over any other act, regulation, contract or arrangement, with a few exceptions (for example, debts under the Income Tax Act, the Excise Tax Act, amounts owed to Crown Corporations by persons other than the Crown).

The regulations prescribe that any amount owed to the Crown with a value of less than $2 (with exceptions as set out in the Low-Value Amounts Regulations) is deemed nil. In those cases, no debt deletion mechanism is needed because the debt is simply deemed to have a value of zero.

Detailed guidance on applying section 155.2 of the FAA and the Low-Value Amounts Regulations is provided in the Guide to Administering Low-Value Amounts.

6.3 Source of funds

A source of funds is required to ensure that all inflows and outflows in the Consolidated Revenue Fund are properly accounted for. The deletion of a debt has a fiscal impact on the federal government because cash inflows will now be lower than originally expected. As a result, regardless of the nature of the debt (for example, budgetary, non-budgetary) or the debt deletion authority used, a source of funds will be needed in most cases when a debt is deleted in order to compensate the amount to the fiscal framework.

The default source of funds is the organization’s reference levels. The source of funds is generally confirmed through the establishment of a lapsing frozen allotment that is equivalent to the amount of the debt being deleted. More information on permanent frozen allotments can be found on the Treasury Board of Canada Secretariat’s (TBS’s) Commonly Sought Authorities page. Should an organization be unable to manage this pressure from its existing reference levels, they should contact their program analyst at TBS to discuss options, which could include a request for a central source of funds provided by a funding decision.

A source of funds should not be mistaken as an allowance for doubtful accounts or bad debts, which are separate accrual accounting considerations based on a department’s estimated receivables expected to be uncollectible. The goal of a source of funds is to set funds aside in the fiscal framework; an allowance for doubtful account or bad debts does not accomplish the same thing. Additionally, the source of funds analysis is independent of the creation of a new vote in the Estimates needed to delete a non-budgetary debt. Creation of a new vote is a legal requirement to ensure that Parliament’s approval is obtained and has no direct funding impact.

6.4 Transfer payments

In cases where a transfer payment program may create a return of funds that could result in a receivable being established in the accounts of Canada under the applicable accounting rules set out in the Financial Information Strategy Accounting Manual, it is recommended that departments analyze each case on an individual basis before entering into funding agreements. This analysis should be done in consultation with the department’s centre of expertise on transfer payments, its legal services unit and accounting operations team to determine whether a debt will exist from a legal standpoint and the authorities available for potential deletion.

6.5 Statute-barred limitations

Although the Treasury Board does not set a time limit for collecting debts, a debt can become statute-barred based on section 32 of the Crown Liability and Proceedings Act . Under the Crown Liability and Proceedings Act, unless another period has been provided in federal legislation, the Crown has six years after a debt has been incurred (not when it was discovered) to take recovery actions where the debt arises otherwise than in a province. Where the debt arises in a province, provincial limitation periods apply, which may be shorter (for example, two or three years).

While some steps can still be taken to pursue a debt after the limitation period has expired, they are legally unenforceable. Therefore, certain actions such as commencing legal proceedings and set-off may not be available.

Given the legal complexities of determining and applying limitation periods, departmental legal services should be consulted in order to determine the applicable period for each situation, including if and how the limitation period can be reset, as well as to prevent debts from inadvertently becoming statute‑barred.

6.6 Fees and other charges owed to departments

Many departments charge fees for the services they deliver (for example, service fees) or as a result of other activities related to their business (for example, rent). Fees, rent or any other charges owed to the department are recorded as debts until they are fully collected. These debts will generally be budgetary because the costs incurred to generate the revenue are most often funded through operating appropriations.

The reduction or waiver of fees and other charges due to the department will generally be considered as a debt deletion transaction where a remission or a write-off may be pursued as outlined in the FAA. This debt remission is not to be confused with the remissions required under the Service Fees Act, which are applied to different scenarios and are also subject to separate criteria. Additionally, other acts of Parliament may provide the authority to remit, reduce or waive specific fees. Those authorities are applied independently from the FAA debt deletion sections; they may also follow a different set of criteria to the ones discussed in this guide.

6.7 Deleting a revolving fund’s accumulated deficit

Revolving funds are a specific financial authority used by a few departments where a program is fully or partly financed by revenue collections and where the operations have a significant cyclical nature (for example, years where there is a surplus finance years where there is a deficit).

There are cases where a revolving fund may be in a net deficit position and, after performing a thorough analysis, will find itself unable to break even within its business cycle as a result of an unexpected event (for example, one-time shocks, unpredictable demand, changing requirements). In those cases, the department may wish to delete all or part of the balance of the fund’s accumulated deficit as a way to fully or partially restore its drawdown authority. This deletion can be sought through the Main Estimates or Supplementary Estimates following Treasury Board approval and will require the identification of a source of funds. For more information about this process, departments should contact their program analyst at TBS.

Although this process may be referred to as a “write-off” or a “forgiveness” in other documents (for example, former Treasury Board policies), the process is not to be confused with the authorities described in this guide that deal with debt deletion. An accumulated deficit from a revolving fund is not a debt owed to the Crown, and the deletion of the balance would be done under the authorities provided by the Directive on Charging and Special Financial Authorities and other relevant sections in the FAA.

7. Accounting and reporting for debt deletion transactions

The deletion of a debt results in the removal of the amount from the accounts of Canada. The accounting and reporting for the debt deletion may vary depending on whether the debt is budgetary or non-budgetary and will determine whether a charge to an appropriation is required.

Supplementary reporting of debt deletions is shown in section 2 of Volume III of the Public Accounts. This reporting requirement stems from section 24.2 of the FAA for forgiveness, subsection 24(2) of the FAA for remissions, and subsection 25(4) of the FAA for write-offs.

For guidance on accounting for debt deletion transactions, refer to the “Debt Deletions” section of the Financial Information Strategy Accounting Manual .

8. References

Legislation and regulations

Related policy and guidance instruments

- Policy on Financial Management

- Directive on Public Money and Receivables

- Guide to Managing Receivables

- Guide to Interest and Administrative Charges

- Guide to Administering Low-Value Amounts

- Commonly Sought Authorities

- Financial Information Strategy Accounting Manual

- Directive on Charging and Special Financial Authorities

9. Enquiries

Members of the public may contact Treasury Board of Canada Secretariat Public Enquiries if they have questions about this guide.

Individuals from departments should contact their departmental financial policy group if they have questions about this guide.

Individuals from the departmental financial policy group may contact Financial Management Enquiries for interpretation of this guide.

Appendix A: Debt deletion summary table

| Write-Off | Forgiveness | Remission | Waiver | |||||||

|---|---|---|---|---|---|---|---|---|---|---|

|

Notes

|

||||||||||

| Type of debts |

Budgetary non-salary debts (for example, supplier overpayments, service fees) |

Budgetary salary debts and accountable advances (for example, salary overpayments, temporary travel advances) |

Non-budgetary debts (for example, advances, loans, investments) |

Debt owed by a Crown corporation to a department may be budgetary or non-budgetary, depending on the nature of the debt. Both can be forgiven and budgetary debts owed by a Crown corporation can also be remitted. |

Non-budgetary debts (for example, advances, loans, investments) |

Budgetary debts (includes taxes and penalties) and other debts (for example, salary and non-salary debts) and budgetary debts of Crown corporations. |

Budgetary and non-budgetary debts for interest and budgetary debts for administrative charges that are charged in accordance with the Interest and Administrative Charges Regulations |

|||

| Authority |

Subsection 25(1) of the FAA and the Debt Write-off Regulations, 1994 |

Subsection 25(1) of the FAA and the Debt Write-off Regulations, 1994, including section 5 if applicable |

Subsection 25(2) of the FAA and the Debt Write-off Regulations, 1994 |

Section 24.1 of the FAA |

Section 23 of the FAA |

Section 155.1 of the FAA and the Interest and Administrative Charges Regulations |

||||

| Approval level required |

|

|

|

|

|

|

||||

| Effect |

The debt is removed from the department’s accounts but is not legally extinguished (that is, it can be reinstated). |

The debt is removed from the department’s accounts and legally extinguished (that is, it cannot be reinstated). |

||||||||

| Reporting |

Reported in the Public Accounts of Canada |

Reported in the Canada Gazette, Part II, and the Public Accounts of Canada |

Reported in the Public Accounts of Canada |

|||||||

| Appropriation Impacts |

Does not result in a charge to an appropriation |

Results in a charge to an appropriation |

Does not result in a charge to an appropriation |

Results in a charge to an appropriation |

Does not result in a charge to an appropriation |

Does not result in a charge to an appropriation |

||||

| Criteria |

As set out in sections 4 and 6 of the Debt Write-off Regulations, 1994, debts may be written off when (must meet at least one of the following criteria):

|

As set out in section 24.1 of the FAA, no debt or obligation may be forgiven in whole or in part otherwise than by an act of Parliament, including an appropriation act. No criteria have been set for determining when debts may be forgiven. However, in practice, the criteria for remissions are used for guidance purposes as both authorities (remission, forgiveness) entail the “forgiving” of a debt. |

As set out in section 23 of the FAA, debts may be remitted when collection is deemed:

|

|

||||||

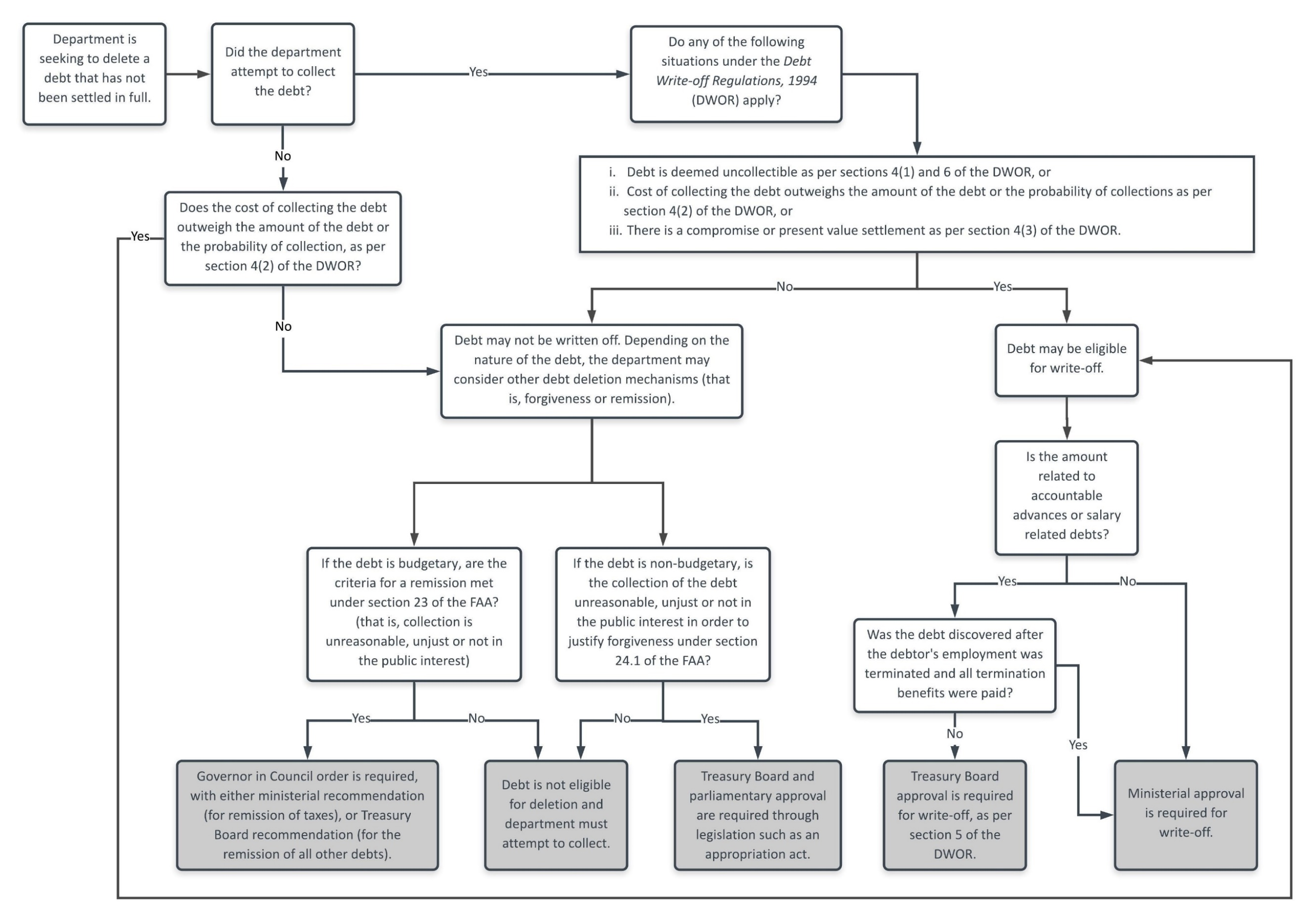

Appendix B: Debt deletion decision tree

Figure 2 - Text version

This decision tree presents an overview of the process to help determine the appropriate debt deletion mechanism to use when a department is seeking to delete a debt that has not been settled in full.

The first step is to determine if the department attempted to collect the debt.

If collection was attempted, the department may determine if any of the following three situations under the Debt Write-off Regulations, 1994 (DWOR) apply:

- Debt is deemed uncollectible as per sections 4(1) and 6 of the DWOR, or

- Cost of collecting the debt outweighs the amount of the debt or the probability of collections as per section 4(2) of the DWOR, or

- There is a compromise or present value settlement as per section 4(3) of the DWOR

If one of these three situations applies, then the debt may be eligible for write-off as follows:

- If the amount is not related to accountable advances or salary related debts, then Ministerial approval is required for write-off.

- If the amount is related to accountable advances or salary related debts and was discovered before the debtor’s employment was terminated and all termination benefits were paid, then Treasury Board approval is required for write-off, as per section 5 of the DWOR. If the amounts were discovered after employment was terminated and all termination benefits were paid, then Ministerial approval is required for write-off.

If one of these three situations does not apply, then the debt may not be written off. Depending on the nature of the debt, the department may consider other debt deletion mechanisms (that is, forgiveness or remission)

- If the debt is budgetary, the department may determine if the criteria for a remission are met under section 23 of the FAA (that is, collection is unreasonable, unjust or not in the public interest)

- If yes, then a Governor in Council order is required, with either ministerial recommendation (for remission of taxes), or Treasury Board recommendation (for the remission of all other debts)

- If no, then the debt is not eligible for deletion and the department must attempt to collect

- If the debt is non-budgetary, the department may determine if collection of the debt is unreasonable, unjust or not in the public interest in order to justify forgiveness under section 24.1 of the FAA

- If yes, Treasury Board and parliamentary approval are required through legislation such as an appropriation act

- If no, then the debt is not eligible for deletion and the department must attempt to collect

If collection was not attempted, the department may determine if the cost of collecting the debt outweighs the amount of the debt or the probability of collection, as per section 4(2) of the DWOR.

- If yes, then the debt may be eligible for write-off as follows:

- If the amount is not related to accountable advances or salary related debts, then Ministerial approval is required for write-off.

- If the amount is related to accountable advances or salary related debts and was discovered before the debtor’s employment was terminated and all termination benefits were paid, then Treasury Board approval is required for write-off, as per section 5 of the DWOR. If the amounts were discovered after employment was terminated and all termination benefits were paid, then Ministerial approval is required for write-off.

- If no, then the debt may not be written off. Depending on the nature of the debt, the department may consider other debt deletion mechanisms (that is, forgiveness or remission)

- If the debt is budgetary, the department may determine if the criteria for a remission are met under section 23 of the FAA (that is, collection is unreasonable, unjust or not in the public interest)

- If yes, then a Governor in Council order is required, with either ministerial recommendation (for remission of taxes), or Treasury Board recommendation (for the remission of all other debts)

- If no, then the debt is not eligible for deletion and the department must attempt to collect

- If the debt is non-budgetary, the department may determine if collection of the debt is unreasonable, unjust or not in the public interest in order to justify forgiveness under section 24.1 of the FAA

- If yes, Treasury Board and parliamentary approval are required through legislation such as an appropriation act

- If no, then the debt is not eligible for deletion and the department must attempt to collect

- If the debt is budgetary, the department may determine if the criteria for a remission are met under section 23 of the FAA (that is, collection is unreasonable, unjust or not in the public interest)

Notes

- The decision tree does not cover the waiver or reduction of interest and/or administrative charges.

- Not all situations may fit within the decision tree as it is a starting point for departments to determine the appropriate debt deletion mechanism. Every debt deletion situation must be assessed on a case-by-case basis, and departments are encouraged to consult with their financial policy group.

Appendix C: Additional guidance on the application of debt deletion authorities under the Financial Administration Act

C.1 Write-off

All debt write-offs are subject to the conditions and criteria provided in the Debt Write-off Regulations, 1994 (the regulations).

In order for the Treasury Board or the appropriate departmental ministers (or officers authorized by that minister in writing) to be able to assess whether the write-off criteria have been met for each debt, departments should determine the rationale to justify the write-off, as detailed below.

Where Treasury Board approval is required, and depending on the volume and the amount of the debt(s) being written off, departments may choose to include the rationale or justification details as a narrative directly in the body of the Treasury Board submission or in a table format as part of an appendix.

The examples below are provided for illustrative purposes only and may not apply to all departments or situations.

The level of analysis expected remains the same regardless of the level of approval required (that is, Treasury Board, the appropriate departmental minister, or the officer authorized by that minister in writing).

C.1.1 Write-off under subsection 4(1) of the regulations

- The amount of the debt, including any applicable interest

- The circumstances leading to the debt (for example, when the debt was discovered, when and why the debt occurred)

- Whether and how all reasonable collection actions were undertaken (for example, collection letters sent to the debtors, any possible legal actions pursued, use of private collection agencies where applicable), as required under subsection 6(a)

- Whether all possibilities to set off have been explored (for example, if it is a budgetary salary debt, was set off against the employee’s salary considered?), as required under subsection 6(b)

- Whether and how any of the criteria under subsection 6(c) are met, and

- What is being done to prevent these debts from happening in the future (for example, what additional internal controls are being implemented?)

Example 1

Department A is seeking to write off a debt resulting from an uncollectible accountable advance under subsection 4(1) and subject to sections 5 and 6 of the regulations.

Details of the debt

- Amount: $20,000 (including $2,000 in interest)

- Date of discovery: June 2017

- Type of debt: Accountable advance related to a relocation

- Origin of the debt: The employee became indebted to the Crown as a result of an unspent accountable advance of $18,000 issued for the purposes of an employment-related relocation that occurred in May 2017. Immediately after the discovery of the debt, the employee terminated his employment with the federal government.

Details on how the debt write-off meets the requirement under subsection 4(1) and all three criteria under section 6 of the regulations

- Collection actions taken under subsection 6(a): Collection letters were sent to the employee and a repayment agreement was reached in July 2017 that met the requirements outlined in the Accountable Advances Regulations. However, the employee filed for bankruptcy shortly after and the full repayment could not be made. An outstanding debt of $18,000 remained, on which $2,000 of interest accrued. As confirmed with departmental legal counsel and the bankruptcy trustee, the employee is bankrupt and no further payments to the departments are foreseen. As a result, no other collection actions can be taken.

- Set-off under subsection 6(b): The repayment agreement with the employee included an immediate repayment through a cheque. As there were no grounds to doubt that the payment would be received, set-off through the Canada Revenue Agency or otherwise was not initiated at that time. Partial collection via a set-off from termination entitlements or benefits was not possible due to the short notice provided by the employee. Given that the employee is bankrupt, and the trustee has certified in writing that no other payments to the department are foreseen, no other set-off actions are possible.

- Other criteria under subsection 6(c): The debtor is an undischarged bankrupt individual and the trustee has certified in writing that no further payments are foreseen. This is in line with subparagraph 6(c)(vii)(B) of the regulations.

To prevent these types of debts from happening in the future, the department is working closely with Public Services and Procurement Canada (PSPC) to implement changes that avoid similar errors to the extent possible. These changes include providing extra lead time for staffing actions and performing regular reviews of pay files.

C.1.2 Write-off under subsection 4(2) of the regulations

- The amount of the debt, including any applicable interest

- The circumstances leading to the debt (for example, when the debt was discovered, when and why the debt occurred)

- How the department deemed the costs to collect are higher than the amount or probability of collection (for example, which cost elements were considered to determine collection costs?)

Example 2

Department B is seeking to write off a non-budgetary debt under subsection 4(2) of the regulations.

Details of the debt

- Amount: $100 (including $20 in interest)

- Date of discovery: August 2015

- Type of debt: Program payment

- Origin of the debt: The individual became indebted to the Crown as a result of an overpayment of government benefits that were received in February 2015.

Details on how the debt write-off meets the requirement under subsection 4(2) of the regulations

Cost-benefit analysis: A detailed analysis was performed to determine the cost to collect and the probability of collection. It is summarized as follows:

- Cost to collect: $80 including the cost to send letters ($10), set-off actions ($20) and hiring a private-sector collection agency ($50).

- Probability of collection: After consultation with the legal services unit and the Canada Revenue Agency, it was determined that in the best-case scenario, the department could collect $70 given the specific situation of the debtor.

- Conclusion: Given that the costs ($80) are greater than the amount the department expects to collect ($70), the debt was determined to be eligible for write-off under subsection 4(2) of the regulations.

C.1.3 Write-off under subsection 4(3) of the regulations

- The amount of the debt, including any applicable interest

- The circumstances leading to the debt (for example, when the debt was discovered, when and why the debt occurred)

- Whether and how subparagraphs 4(3)(a) or 4(3)(b) are met (for example, provide details on the determination of the present value or the circumstances explaining the compromise settlement)

Example 3

Department C is seeking to write off a budgetary debt under subparagraph 4(3)(b) of the regulations.

Details of the debt

- Amount: $6,000 (including $500 in interest)

- Date of discovery: July 2019

- Type of debt: Debt from to third-party recipient

- Origin of the debt: Stemming from litigation related to a service contract with a third party.

Details on how the debt write-off meets the requirement under subsection 4(3) of the regulations

The department entered into a service contract with a third party. During the execution of the contract, a dispute arose relating to the timelines of the work done. The department was of the view that it was owed $10,000 (including interest) while the third party claimed that there had been a breach of contract by the department and therefore nothing was owed. On the advice of the department’s legal services unit, a settlement was reached for $4,000 between the parties. The balance of $6,000 (principal and interest) is being written off under subparagraph 4(3)(b) of the regulations.

C.2 Remission or forgiveness

Where the remission or forgiveness of debts under the FAA require Treasury Board recommendation or approval respectively, a Treasury Board submission must be prepared as detailed under subsection 5.2 and subsection 5.3 of this guide.

In order for the Treasury Board to be able to assess whether the remission or forgiveness criteria have been met for each debt, departments should include the details below as applicable:

- the amount of the debt, including any applicable interest

- the circumstances leading to the debt (for example, nature of the debt, when the debt was discovered, when and why the debt occurred)

- whether any collection actions have been undertaken

- rationale on why no collection actions have been undertaken

- rationale on whether collection is unreasonable, unjust or not in the public interest

- future impact of the decision (for example, other debts of a similar nature that could be impacted, possible changes in business practices in the future that would avoid similar debts)

Examples of debt remissions include: