Guide to Costing

Archives

This guide replaces:

- Cost Estimation for Capital Asset Acquisitions, Guideline on [2019-06-10]

- Costing, Guidelines on [2019-06-10]

- Cost Estimating, Guide to [2023-05-10]

Note to reader

The Guide to Costing takes effect on May 10, 2023 and replaces the Guide to Cost Estimating.

1. Effective date

This guide was published on May 10, 2023, and it replaces the Guide to Cost Estimating (June 10, 2019).

2. Objectives and expected results

This guide explains costing in the Government of Canada (GC) and outlines the principles and process, along with the corresponding approaches and techniques, used to develop costing information that is credible.

This guide sets out how to develop credible costing information that:

- provides contextual insight that supports decision-making

- improves the understanding of cost uncertainty, cost risk and cost drivers

- aligns with the objectives and expected government-wide results identified in the Policy on Financial Management and supports the assertions and conclusions of the chief financial officer, as required by the Guideline on Chief Financial Officer Attestation for Cabinet Submissions

- supports the obligations and requirements for external charging (fees) and internal charging identified in the Directive on Charging and Special Financial Authorities and the obligations and requirements for fees prescribed under the Service Fees Act

- supports assessing life-cycle costs for investment decisions, as identified in the Policy on the Planning and Management of Investments

- assists in the development of rough order of magnitude (ROM), indicative and substantive estimates that are required when seeking Treasury Board approvals or expenditure authorities for projects or programmes, as detailed in the Directive on the Management of Projects and Programmes

- supports the life-cycle management of real property, as described in the Directive on the Management of Real Property

- supports the management of procurements, as described in the Directive on the Management of Procurement

Costing has a role to play in many different policy areas in the GC, and the costing principles and process in this guide can be applied to inform decision-making in many different fields.

This guide can be used:

- as a resource to understand the credibility of recipient costing information under the Policy on Transfer Payments

- when analyzing the cost impacts of procurements that contribute to economic growth in Canada

- to analyze the life-cycle costs of investments when considering commitments made in the Greening Government Strategy

3. Context

Costing in the GC includes:

- cost accounting, which emphasizes the allocation of costs (for example, direct and indirect)

- cost estimating, which emphasizes forecasting costs and the associated level of uncertainty and risk

Credible costing information, as outlined in this guide, supports decision-making that is based on evidence and data. Developing costing information that is credible requires time and effort; there are several challenges to developing such information, including:

- data availability and quality limitations

- limited information about associated cost uncertainties and risks

- limited interaction between stakeholder groups (for example, project managers, financial officers, subject matter experts)

- resource constraints (for example, people, tools and time)

Despite these challenges, credible costing information can be produced if a standardized process that is rooted in internationally recognized best practice is followed. The principles and process described in this guide can be applied to all costing exercises in the GC.

4. Common applications

Decision-making in the GC requires credible costing information.

Costing exercises that apply the principles and process described in this guide produce credible costing information to support decisions in the GC. These decisions range from those made by Cabinet to those made internally within an organization. Some of the ways costing information can be applied to support various types of decisions are outlined in Appendix A.

Costing information supports:

- decisions between different courses of action

- legislative or policy changes

- decisions about offering a new initiative or activity

- level-of-service decisions

- charging and cost-recovery decisions

- investment decisions

- contracting and procurement decisions

- decisions about reorganizations

- assessments of results

While some common applications are described, the guide does not focus on how costing information can be used. These requirements are outlined in other legislation and policy instruments.

For example, the costing process in this guide can be used to develop credible costing information to support charging. However, the requirements for how the costing information is used in external charging (fees) and internal charging are identified in the Service Fees Act and the Directive on Charging and Special Financial Authorities.

5. Roles and responsibilities

Costing is a collaborative effort that involves multiple stakeholders who have a range of knowledge and expertise. This section outlines roles and responsibilities that may be assigned to stakeholders in order to enable the development of credible costing information.

The roles and responsibilities listed in this section are not exhaustive; the structure may vary by organization and additional responsibilities are outlined in the associated policy instruments.

Deputy heads

Deputy heads may support the following:

- establishing and maintaining appropriate governance and oversight structures to enable the production of credible costing information and support engagement with key stakeholders

- ensuring that costing exercises apply the GC’s costing process, that resulting costing information is credible, and that relevant costing information is disclosed for decision-making

Refer to relevant policy instruments for a complete list of deputy head responsibilities, such as subsection 4.1 of the Policy on Financial Management and subsection 4.1 of the Policy on the Planning and Management of Investments.

Chief financial officers

Chief financial officers may support the following:

- ensuring that their organization’s costing capacity is aligned with the level of complexity, risk and materiality of the initiatives

- coordinating the collection and retention of costing information and the provision of tools required to develop credible costing information

- ensuring due diligence in the application of the costing process and challenging the credibility of the costing information where necessary

- ensuring that key costing information, including the cost impact of key assumptions and the level of uncertainty and risk associated with the initiative, is disclosed by way of a chief financial officer attestation

Refer to relevant policy instruments for a complete list of chief financial officer responsibilities, such as subsection 4.2 of the Policy on Financial Management and section 3 of the Guideline on Chief Financial Officer Attestation for Cabinet Submissions.

Senior departmental managers

Senior departmental managers may support the following:

- ensuring that the appropriate resources (for example, people, tools, time) are assigned to develop and deliver credible costing information in a manner that is consistent with the level of complexity, risk and materiality associated with the initiatives

- encouraging collaboration with stakeholders throughout the development of the costing exercise

- ensuring that the key costing information (for example, quality of the data, impact of key assumptions and cost drivers, level of uncertainty and risk, quality assurance and validation efforts) is disclosed to the deputy head and chief financial officer, when applicable, to support obligations for accountability and strategic decision-making

Refer to relevant policy instruments for a complete list of the responsibilities of senior departmental managers, such as subsection 4.3 of the Policy on Financial Management.

In certain circumstances these responsibilities could apply to the roles of senior designated officials, as outlined in subsection 4.1 of the Directive on the Management of Procurement.

Manager of a program or investment

The manager of a program or investment (that is, the director or manager) may support senior departmental managers by:

- ensuring that costing practitioners have the information needed to develop credible costing information (for example, documentation, data and evidence, ground rules)

- engaging departmental costing expertise, costing practitioners and other stakeholders early and often throughout the initiative, so that costing practitioners have sufficient time to develop credible costing information

- ensuring that the development of costing information is clearly assigned in alignment with delivering results and includes establishing a work plan and schedule

- ensuring that key costing information is documented and communicated, including the quality of the data, impact of key assumptions and cost drivers, level of uncertainty and risk, and quality assurance and validation efforts

In certain circumstances these responsibilities may apply to the role of project and programme sponsors, as outlined in subsection 4.1.12 of the Policy on the Planning and Management of Investments.

Costing practitioners

Costing practitioners may support the manager of a program or investment by:

- ensuring that the roles and responsibilities and work plan for costing exercises are outlined in a manner that supports the delivery of results

- identifying and engaging stakeholders, including subject matter experts, early and often to establish assumptions, gather data and identify risks

- applying the costing process to produce credible costing information that supports the transparent disclosure of financial risk for decision-making

- clearly and concisely documenting the steps that were taken to develop the costing information

- ensuring that key costing information and detailed costing information are communicated

Since costing practitioners operate out of many different areas and may have different roles, they are defined as any individual who performs work related to costing. For example, the manager of a program or investment may also be a costing practitioner.

6. Credible costing information

Credible costing information supports informed decision-making in the GC by assessing the costs related to a decision. Credible costing information is the result of applying the costing process described below.

Credible costing information is defined by the following criteria.

Process-driven

Credible costing information is the result of a rigorous and repeatable process that includes the participation of a wide range of stakeholders.

Process-driven costing information ensures that:

- the purpose and deliverables of the costing exercise are well defined

- there is agreement on ground rules, assumptions and data sources

- stakeholders are engaged throughout the costing exercise

- errors are identified and corrected throughout the costing exercise

- the results of the costing exercise are clearly communicated to stakeholders

Comprehensive

Credible costing information has a defined scope that considers all cost elements related to the decision that the costing information supports. Costing exercises should include clearly defined boundaries in terms of time and scope and all related costs, such as inflation, internal services and life-cycle costs.

Comprehensive costing information ensures that:

- the boundaries of the costing exercise can be communicated to decision-makers and stakeholders

- all relevant cost elements are included in the costing exercise

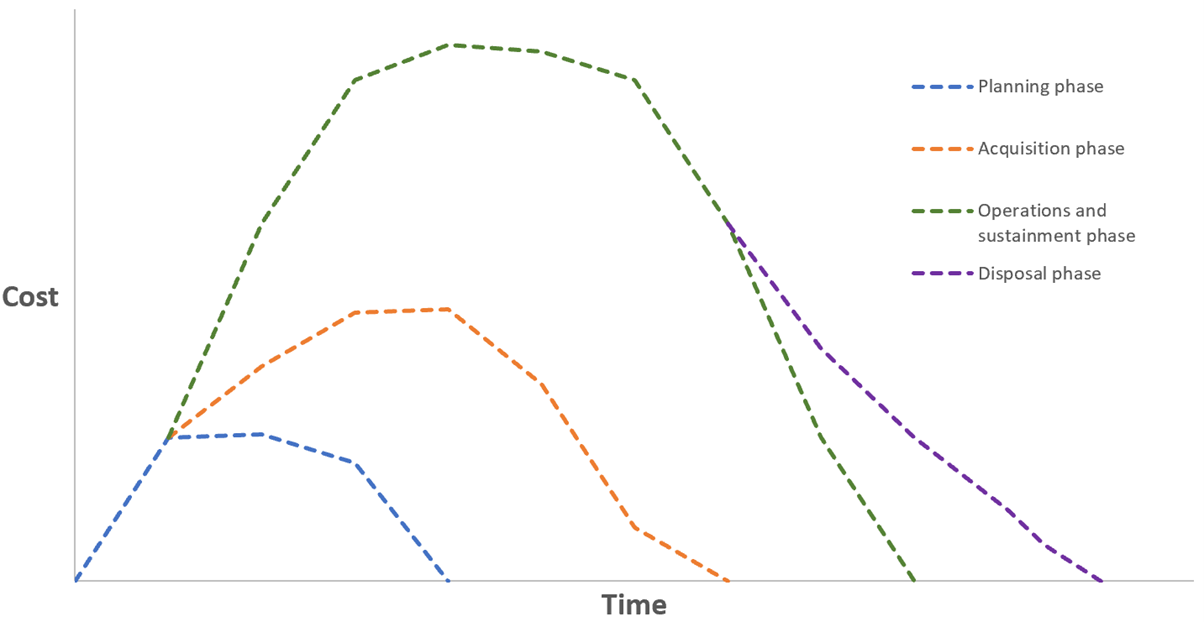

Figure 1 shows the evolution of costs over the life cycle of a project or programme.

Figure 1 - Text version

Figure 1 is a line graph. Time is indicated on the X-axis and cost is indicated on the Y-axis. The four lines on the graph represent the following phases: planning, acquisition, operations and sustainment, and disposal. The lines show when the costs for each phase occur and how they grow and decline over time.

Evidence-based

Credible costing information is supported by evidence and uses data as the basis for costs. Actual or historical data, which can include information in an organization’s financial system of record, is the foundation of evidence-based costing.

Evidence-based costing information ensures that:

- subjectivity in a costing exercise is reduced

- the costing information has a traceable source that can be examined and assessed by stakeholders and reviewers

- data analysis can be used to improve the application of costing techniques

Risk-assessed

Credible costing information considers the cost impacts of uncertainty and risk.

Risk-assessed costing information ensures that:

- costing exercises are more reliable as the uncertainty associated with the underlying data and assumptions has been considered

- contingency amounts:

- provide confidence that the estimate or budget is sufficient for the initiative or activity

- are based on an uncertainty and risk assessment

- financial risk is transparently disclosed to stakeholders and decision-makers

Validated

Credible costing information is comparable to past performance, similar initiatives or activities, or recognized benchmarks. Validated costing information ensures that decision-makers and other stakeholders have confidence that the costing information is reasonable.

Documented

Credible costing information is chronicled in sufficient detail such that an independent party could reproduce the results of the costing exercise.

Documented costing information ensures that:

- reviewers can understand how the costing information was produced

- the details of the costing exercise are transparent and traceable, including costs that were not included in the costing exercise

- the costing information can support scrutiny and audits

- information (for example, assumptions, ground rules and data sources) is stored in a location that is accessible to current and future costing practitioners

- lessons learned are recorded and used to inform best practices for future exercises

These criteria for credible costing relate to various policy areas in the GC.

For example, the criteria support the development of rough order of magnitude (ROM), indicative, and substantive cost estimates for programme or project approvals and expenditure authorities, as outlined in the Directive on the Management of Projects and Programmes. Moreover, ensuring costing information is credible supports other policy objectives, such as:

- ensuring oversight and sound stewardship of public resources, as identified in the Policy on Internal Audit

- making risk disclosure assertions, as explained in the Guideline on Chief Financial Officer Attestation for Cabinet Submissions

- using costing information to identify indicators, collect data and conduct evaluations, as outlined in the Directive on Results

7. Costing process

The costing process outlined below applies to all costing exercises in the GC. The level of effort associated with the development of costing information should be consistent with the purpose, complexity, risk and materiality of the costing exercise. The application of the costing process in organizations should be periodically reviewed to continually implement lessons learned.

Some actions may be required throughout the costing process, including stakeholder engagement, documentation and the collection of lessons learned. While the steps are presented in a logical order, they are not always sequential. Some steps may need to be executed simultaneously or iteratively. Additionally, early steps in the process may need to be revisited as the costing exercise progresses or more information is obtained about the initiative or activity. For example, ground rules, assumptions, uncertainties and risks are assessed as they relate to prior initiatives or activities and as the current initiative or activity evolves.

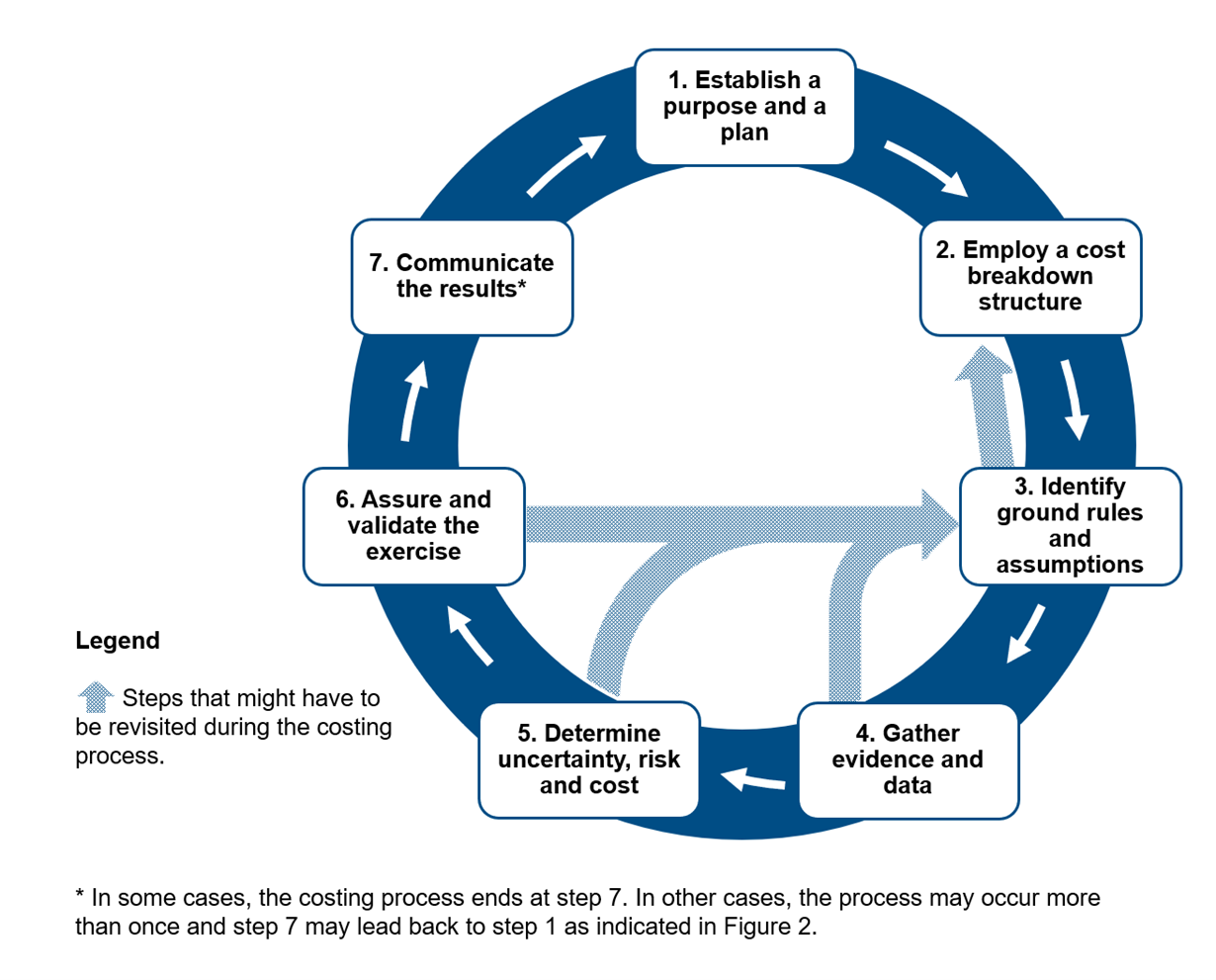

Figure 2 illustrates the steps in the costing process.

Figure 2 - Text version

Figure 2 is cycle graph. The seven steps of the costing process are shown:

- Establish a purpose and a plan

- Employ a cost breakdown structure

- Identify ground rules and assumptions

- Gather data and evidence

- Determine uncertainty, risk and cost

- Assure and validate the exercise

- Communicate the results*

Arrows indicate which steps might need to be revisited. At step 3, it may be necessary to go back to step 2. At steps 4, 5 or 6, it may be necessary to go back to step 3.

* In some cases, the costing process ends at step 7. In other cases, the process may occur more than once and step 7 may lead back to step 1 as indicated in Figure 2.

Step 1: establish a purpose and a plan

The purpose of the costing exercise is influenced by the decision that the costing information will support. Establishing a purpose and plan helps determine:

- which stakeholders to engage

- the cost elements to be established by the costing exercise

- the time frame covered by the costing exercise

- how to deliver the costing information

The plan for the costing exercise should include:

- reviewing lessons learned from previous costing exercises

- completing a work plan for each step of the costing process

- establishing a schedule to meet deadlines and communicate progress and delays

- specifying which stakeholders will be consulted and agreeing on how they will be engaged

- specifying and assigning responsibilities (stakeholders may need to be consulted)

Stakeholders who should be consulted

The chief financial officer should always be identified as a key stakeholder when a costing exercise is prepared for a Cabinet submission.

Other stakeholders may include:

- representatives from internal service groups

- managers who are responsible for the initiative or activity or are otherwise impacted

- employees engaged in the costing work, such as financial management advisors or other functional specialists

- employees who are responsible for data

- other departments, agencies or governmental organizations for cross-departmental initiatives or activities

Step 2: employ a cost breakdown structure

The scope of activities that are included in the costing exercise should be defined in consultation with stakeholders.

A cost breakdown structure (CBS) defines the scope by breaking down an initiative or activity into cost elements that will need to be assessed. A CBS should be selected or developed at the outset of a costing exercise.

A CBS is a hierarchical structure in which overarching or “parent” cost elements are subdivided into independent “children” cost elements. The sum of the children cost elements should amount to the value of the parent cost element. In this way, a costing exercise can capture costs comprehensively and prevent double counting. The subdivision should stop at the lowest level that adds value for the purpose of comparison or data analysis.

A CBS should be consistent across similar initiatives or activities. A consistent CBS organizes the gathered data and allows comparison, even if the initiatives or activities have different sizes or complexities. In instances where an initiative or activity already has a work breakdown structure (WBS) used for project management, the CBS is usually developed in conjunction with the WBS so that the breakdown of cost elements aligns with the planned tasks.

Step 3: identify ground rules and assumptions

Ground rules and assumptions establish the baseline conditions of a costing exercise. Ground rules and assumptions are necessary components of every costing exercise.

Ground rules are a prescribed set of conditions that provide guidance to the direction of a costing exercise. They often become constraints that define the boundaries and scope of the costing exercise. For example, a ground rule for a construction project may be that all materials are to be procured in Canada, which means that a costing exercise is limited to forecasting costs for domestic materials.

Assumptions are the underpinning hypotheses upon which a costing exercise is built and from which the costing requirements are drawn. Assumptions use evidence to make judgments to fill the gaps between input data and the results of the costing exercise. Assumptions are deemed to be true in the absence of facts and supported by data when possible. An example of an assumption might be that a new digital service can be delivered using existing information technology infrastructure.

Ground rules and assumptions enable the determination of costs when evidence and data may not be available for all cost elements. Ground rules and assumptions should be documented so that the basis of a costing exercise can be clearly demonstrated. Furthermore, documentation helps costing practitioners ascertain when the ground rules, assumptions and subsequent results are no longer valid, and provides a clear rationale for revisiting a costing exercise.

Step 4: gather evidence and data

Evidence and data are required to determine costs. The data used in a costing exercise should be the best available. In the absence of actual or historical data, qualitative evidence from subject matter experts can be transformed into data by using robust qualitative and quantitative research techniques, as described in Further considerations.

After data is collected, it should be normalized for consistency and comparability. Normalization adjusts for differences between the historical data and the initiative or activity that is the subject of the costing exercise. Some common forms of normalization are adjustments to the value of money over time (for example, inflation) and differences in purchase location (for example, foreign exchange or regional price differences).

Data that is collected and normalized should be stored in an accessible location for future use. Contextual information associated with the data should also be saved so that the data can be interpreted correctly in the future.

Step 5: determine uncertainty, risk and cost

This step applies costing approaches to the gathered data and evidence to determine costs.

A deterministic estimate, sometimes known as a point estimate, should be established using one of the costing approaches.

A deterministic estimate is a single value that:

- represents the total expected cost of an initiative or activity within a range of potential outcomes

- does not consider the uncertainty and risk associated with the cost elements

The uncertainty and risk associated with the cost elements should also be determined to identify the range of cost impacts and their associated likelihood.

Cost uncertainty stems from fluctuations in costs that will occur. The exact impact of cost uncertainty is unknown due to imperfect information. An example of cost uncertainty is the future foreign exchange rate for materials or services procured in foreign currency.

Cost risk is something that may or may not occur and that may increase or decrease cost. An example of cost risk is the cost impact of a potential mechanical breakdown in a manufacturing environment.

A cost uncertainty and risk analysis helps assess whether an estimate for an initiative or activity is realistic. The analysis quantifies the cost impact of the uncertainty and risk associated with the initiative or activity. The results of this analysis are more useful to decision-makers than a deterministic estimate alone because the results communicate the range of potential costs and the likelihood and impact of cost fluctuations.

Sensitivity analysis is a related tool that can be applied to show how individual cost elements or assumptions influence the overall cost.

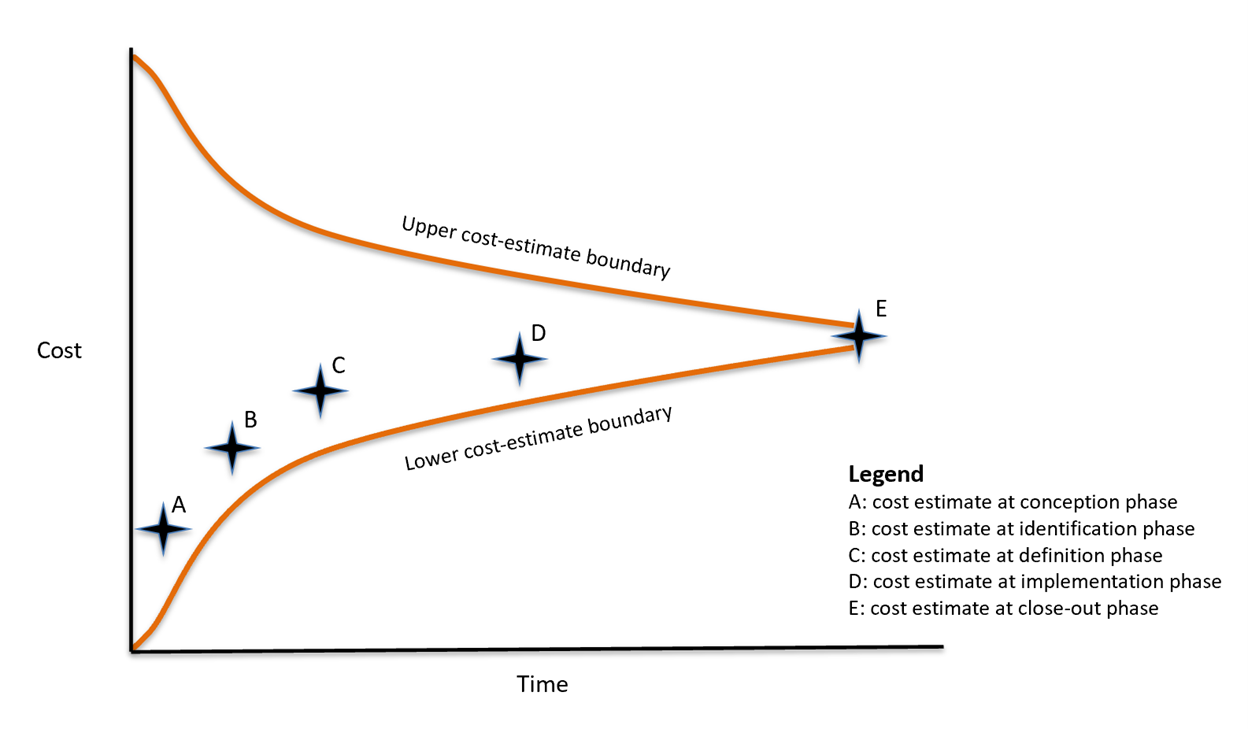

In general, an initiative or activity has greater cost uncertainty during the early stages when there is less information available. As the initiative or activity matures, the uncertainty associated with the estimated costs decreases. For example, an initiative at the Memorandum to Cabinet stage will have many more unknowns than an initiative at the Treasury Board submission stage.

Figure 3 illustrates this concept for a project or programme using the cone of uncertainty, where over time, two distinct costing trends are noted:

- uncertainty decreases (represented by the narrowing boundaries) as requirements become more concrete and risks either materialize or are mitigated

- estimates change (represented by points A through E) as the level of effort to achieve objectives is better understood and some risks materialize

Figure 3 - Text version

Figure 3 is a graph. Time is indicated on the X-axis and cost is indicated on the Y-axis. There are two bands: one that represents the upper cost-estimate boundary and another that represents the lower cost-estimate boundary. Cost estimates at different phases are labelled as follows:

- A: cost estimate at conception phase

- B: cost estimate at identification phase

- C: cost estimate at definition phase

- D: cost estimate at implementation phase

- E: cost estimate at close-out phase

Over time, the space between the bands narrows. The upper and lower cost-estimate boundaries practically meet at E, the cost estimate at close-out phase.

Uncertainty and risk can be assessed qualitatively or quantitatively according to the complexity of the costing exercise and the availability of data and evidence. For complex cost estimates, quantitative statistical methods, such as Monte Carlo or methods of moments analysis, should be used to determine cost uncertainty and risk.

Cost uncertainty and risk should be considered for every costing exercise. The level of effort associated with assessing cost uncertainty and risk should be proportional to the complexity, risk, and materiality of an initiative or activity. Costing exercises should present a range of potential cost outcomes based on an uncertainty and risk analysis, as well as on a deterministic estimate, unless the range is insignificant. If the range is insignificant, the rationale for not assessing cost uncertainty and risk should be documented.

For example, in many cost accounting applications, the data and evidence used to determine costs is very reliable and provides confidence that there is little uncertainty or risk in the results.

One response to a cost uncertainty and risk assessment is contingency, which is sometimes included in a cost estimate. Contingency should be based on a cost uncertainty and risk analysis, as well as on the risk tolerance of decision-makers, which can vary by initiative or activity. As a response to cost uncertainty and risk, contingency may not reduce the residual risk completely, but it should provide confidence to decision-makers that the initiative or activity can be implemented.

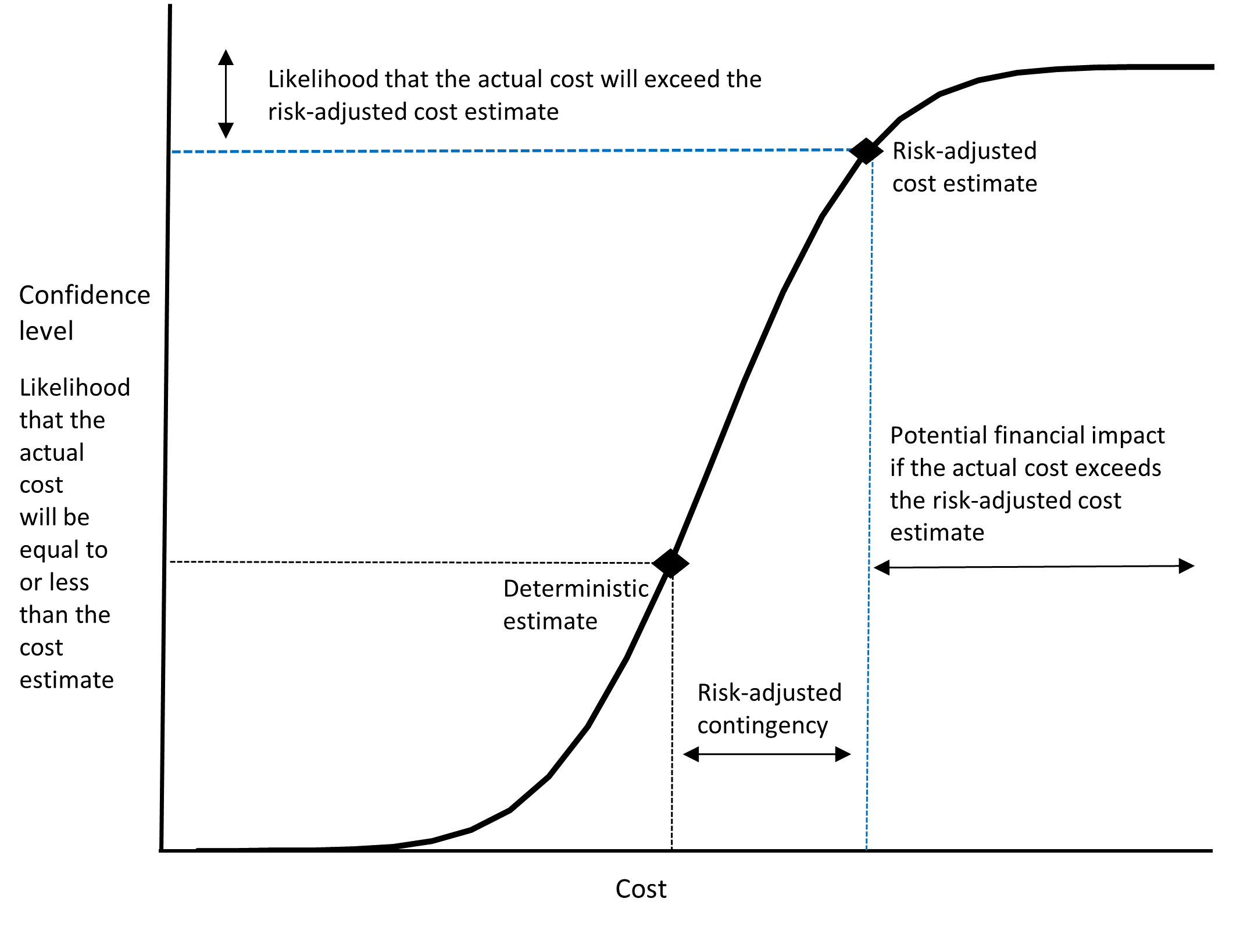

Figure 4 is an S-curve that demonstrates the estimated cost range of a project or programme at a specific point in time. A point along the S-curve identifies a confidence level that describes the probability that a project or programme will finish at or below a given cost. The range of potential cost outcomes is based on the uncertainty and risk faced by the project or programme. This information can be used to inform a given risk-adjusted cost estimate and contingency and help make decisions about trade-offs.

Figure 4 - Text version

Figure 4 is a graph. Cost is indicated on the X-axis and confidence level is indicated on the Y-axis. The confidence level refers to the likelihood that the actual cost will be equal to or less than the cost estimate.

There are two points indicated on the S-curve:

- deterministic estimate

- risk-adjusted cost estimate

The space between the deterministic estimate and the risk-adjusted cost estimate along the X-axis represents the risk-adjusted contingency. The space along the X-axis after the risk-adjusted cost estimate represents the potential financial impact if the actual cost exceeds the risk-adjusted cost estimate.

The space along the Y-axis above the risk-adjusted cost estimate represents the likelihood that the actual cost will exceed the risk-adjusted cost estimate.

Step 6: assure and validate the exercise

Assuring and validating a costing exercise provides confidence in the rigour of the application of the costing process and the quality of the results. The level of effort employed in this step should be consistent with the level of effort required for the costing exercise.

Quality assurance provides confidence that:

- the results are trustworthy in that they reflect the ground rules, assumptions and requirements of the costing exercise

- there are no calculation errors

Validation ensures that the results reflect the real world by demonstrating that the results are reasonable when compared to past performance, comparable or historical examples, independent estimates, or recognized benchmarks.

Some activities that can form part of this step are:

- checking for calculation errors and inconsistencies

- assessing whether the costing process was applied appropriately

- reviewing and challenging the assumptions used to generate the results

- comparing the data and results from similar initiatives, activities or data sources

- cross-checking the costing exercise against recognized benchmarks or authoritative sources and explaining material differences

- performing an independent estimate

For Cabinet submissions, the chief financial officer attestation, as outlined in the Guideline on Chief Financial Officer Attestation for Cabinet Submissions, forms an important part of this step.

Step 7: communicate the results

Effective communication is crucial to the success of a costing exercise as it explains the results to audiences unfamiliar with the initiative or activity, thereby promoting informed decision-making and the transparent disclosure of financial risk. Communication tools may include briefing notes and slide decks that incorporate visuals, such as figures 1, 3, and 4 of this guide.

The costing process and results should be documented. One common form of documentation is a cost report. A cost report describes the costing process, ground rules, assumptions, data sources and results. Its audience may include future costing practitioners and those responsible for challenge functions, evaluations, and audits.

A cost report also ensures that lessons learned can be captured and retained to improve future costing exercises, as well as periodic reviews of the implementation of the costing process across an organization.

The documentation should communicate any limitations of the analysis and uncertainty or subjectivity about source data and assumptions.

8. Costing approaches and techniques

When considering how to determine uncertainty, risk and cost in step 5 of the costing process, it is important to weigh the benefits of the costing information against the time and effort required to produce this information.

The tools used to calculate costs can range from a simple table of expected annual costs to a complex computer model that uses cost estimating relationships to assess the results of thousands of scenarios. Data availability and the maturity of an initiative or activity can influence the costing approach or technique selected.

Costing approaches describe different ways that costing techniques are applied to determine costs. Costing techniques describe the basic methods that are used to determine the value of a single cost element. A single costing exercise may use multiple approaches and multiple techniques.

Costing approaches

The following are three types of costing approaches, which apply costing techniques to produce credible costing information.

Top-down

A top-down approach assesses the total costs of an initiative or activity and divides the assessed costs into smaller cost elements. A top-down approach is often used when costing information is most appropriately assessed at the highest level compared to lower levels. For instance, at the early stages of an initiative or activity, it may be difficult to gather the data and evidence required to calculate the value of cost elements in more detail. Furthermore, a top-down approach may require less effort and be just as credible.

An example of a top-down approach is estimating the cost of a project management office at an early stage of a project, where it is assumed to be a percentage of total project cost based on other analogous data.

Bottom-up

A bottom-up approach determines the cost of each cost element, the sum of which is the total cost of the initiative or activity. This approach involves using costing techniques to determine a cost for each cost element based on actual data. Bottom-up approaches are best employed when determining the costs at later stages of an initiative or activity when detailed information is available.

An engineering build-up approach may sometimes be considered a bottom-up approach.

An example of a bottom-up approach could be estimating the cost of a project management office by determining all the individual salary and non-salary cost elements and estimating a cost for each of them.

Activity-based costing

An activity-based costing (ABC) approach uses actual or historical data and applies costing techniques to allocate costs. An ABC approach captures all costs related to an initiative by breaking down costs by activity and related resources consumed to produce costing information. Once the relevant breakdown is determined, costs may be described as direct, indirect, variable, fixed and/or step.

ABC supports decision-making by organizing and improving the visibility of costs, which identifies the resource requirements of a given activity and links them to a department’s overarching objectives and results. Another benefit of the approach is that activities are linked to cost drivers, so the impact on resources due to changes to activities can be readily assessed.

How approaches can be combined

Multiple approaches may be combined in a costing exercise to determine the costs of an initiative or activity.

For example, a new initiative to deliver a capital asset (such as a bridge) may use:

- a top-down approach to determine design and construction costs

- a bottom-up approach to determine detailed project management requirements (for example, full-time equivalent costs and non-salary costs)

- an activity-based costing approach to determine the internal services required to enable successful delivery

Costing techniques

There are two primary techniques used to determine the cost of a cost element.

Analogous technique

An analogous technique uses data from a comparable initiative, activity or cost element as the basis for determining costs. Adjustments are then made using scaling parameters that represent differences in size, performance, technology, complexity and other factors.

An analogous technique is best used when historical data is available and is closely aligned to cost elements. It is often used during the early stages of an initiative or activity when there is little data and evidence to inform the use of more advanced techniques. It is best to use a parametric technique for complex initiatives, activities or cost elements that do not have straightforward analogies.

An analogous technique often relies on expert opinion to adjust historical costs so that they approximate the total cost of an initiative or activity. If possible, the adjustments should be quantitative rather than qualitative to avoid subjective judgments.

The costing practitioner should document the assumptions and data sources used with this technique.

Parametric technique

A parametric technique applies statistical analysis to data from similar initiatives and activities to develop a cost estimating relationship (CER) that is used to generate costing information. A CER is an equation that determines the numerical value of a given cost element using an established relationship with one or more independent cost drivers. The relationship may be mathematically simple, such as a proportion, ratio or rate, or it may involve a complex equation or method, such as a regression analysis. CERs should be applicable to the cost element and appropriate for the range of data being considered.

A parametric technique in costing relies on data from many initiatives or activities. In general, a parametric technique should be applied when there is data available from several historical initiatives, activities or cost elements that have relationships based on cost drivers. A parametric technique is often used when an initiative or activity has progressed beyond the early stages and detailed information is known about cost drivers.

The costing practitioner should document the related mathematical methods, statistics, assumptions, normalization processes and data sources used for this technique.

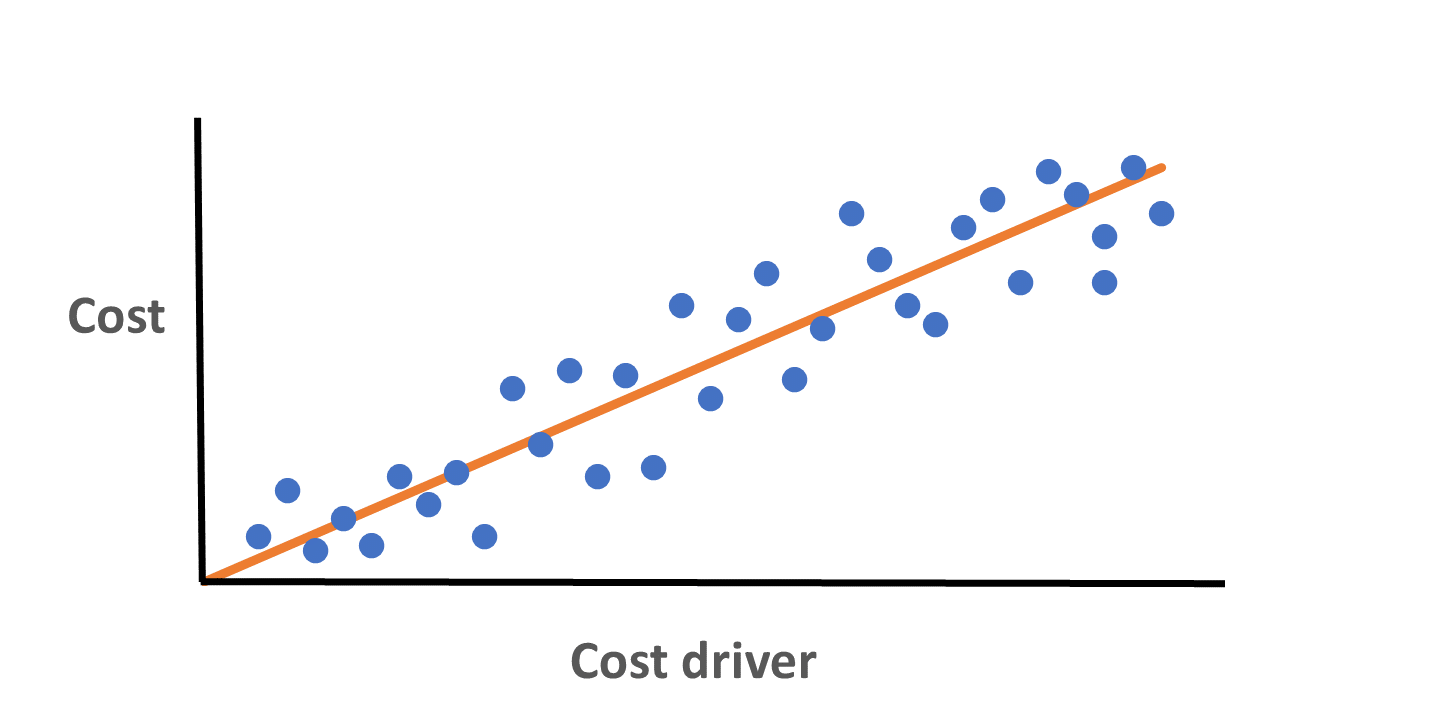

Figure 5 shows the cost estimating relationship between a cost driver and cost. The graph shows that the cost driver has a direct influence on cost such that an increase in the quantity of the cost driver results in an increase in cost.

Figure 5 - Text version

Figure 5 is a scatter plot graph. A cost driver is indicated on the X-axis and cost is indicated on the Y-axis.

The scatter plot is populated with dots that represent data points and a line of best fit. The line is positively and strongly correlated with the data points, which tightly surround the line of best fit in an upward fashion.

Further considerations

Costing practitioners often use data from other initiatives and activities and apply analogous or parametric techniques in order to determine cost. However, at times, actual data about costs or trends can be used to determine future costs for the same initiative or activity. In these cases, the analogous or parametric technique may also be known as extrapolation from actuals.

An example of extrapolation from actuals using an analogous technique is an assumption that the cost to perform an activity in the future will be the same as the cost of the activity in the past. An example of extrapolation from actuals using a parametric technique is an “estimate at completion” from earned value management.

Expert opinion

Expert opinion uses an expert or group of experts to determine costs without a basis in an identifiable data source. Expert opinion tends to produce subjective costing information and produces results that are less reliable than other costing techniques due to an increased risk of cognitive bias. When possible, costing practitioners should favour techniques that use actual or historical data instead of expert opinion.

Expert opinion can be useful in the absence of other viable alternatives. The subjectivity of expert opinion can be mitigated through comparisons to other initiatives or activities, independent estimates, or an uncertainty analysis. Qualitative evidence from subject matter experts can be transformed into data by using robust qualitative and quantitative research techniques.

When expert opinion is used to determine costs, the costing practitioner should document the method used to obtain the expert opinion (for example, interviews) along with the credentials, experience, and position titles of the experts consulted.

The use of experts to interpret and provide context to data can improve the quality of the analogous or parametric technique used. It is good practice to engage experts when using costing techniques. When experts inform the use of data-driven techniques, consulting experts is not considered using an expert opinion.

9. References

Costing is an essential component of many GC activities and, consequently, is related in some way to most policy instruments in the GC. The following sets out key references that should be read in conjunction with this guide:

- Directive on Charging and Special Financial Authorities

- Directive on the Management of Materiel

- Directive on the Management of Procurement

- Directive on the Management of Projects and Programmes

- Directive on the Management of Real Property

- Greening Government Strategy

- Guideline on Chief Financial Officer Attestation for Cabinet Submissions

- Policy on the Planning and Management of Investments

- Policy on Results

- Framework for the Management of Risk

- Service Fees Act

- Treasury Board Submissions

10. Community of practice

The Costing Community of Practice GCpedia page (accessible only on the Government of Canada network) exists to connect, support and engage costing practitioners across the GC.

Additional guidance, tools, templates and training that expand on the concepts presented in this guide are available:

- on the Costing Community of Practice GCpedia page

- through professional associations, academic institutions and other GC publications

11. Enquiries

Members of the public may contact the Treasury Board of Canada Secretariat (TBS) Public Enquiries at questions@tbs-sct.gc.ca if they have questions about this guide.

Individuals from departments, agencies, or other governmental organizations should direct enquiries about this guide to the relevant unit in their organization.

For interpretation of this guide, relevant units should contact the Costing Centre of Expertise at CCE-CEEC@tbs-sct.gc.ca.

Appendix A: common applications

The following are some of the ways that costing information can be applied to support various types of decisions and assessments.

Decisions about different courses of action

Costing information can support decisions about whether to:

- purchase, develop, subcontract, or lease an asset or service

- retain, dispose or divest of an asset

- retain or replace an existing service provider

- purchase an asset off-the-shelf, engage in a contract with the supplier to modify an off-the-shelf asset, or design a new asset

- continue (status quo), adjust, or terminate an initiative or activity

For example, a costing exercise could support an options analysis in a Memorandum to Cabinet that compares the cost of developing a new case management system with the cost of customizing and maintaining an existing commercial off-the-shelf asset.

A legislative or policy change

When decision-makers are considering a change in legislation or policy, they can use costing information to:

- assess different delivery, design and implementation options

- understand the cost impact of the change

- consider whether adequate resources are available to implement and sustain the change

For example, a costing exercise could be used to estimate the cost of changing the eligibility criteria for a social program or benefit.

Decisions about offering a new initiative or activity

When decision-makers consider whether to offer a new initiative or activity, they can use costing information to:

- identify new costs

- identify existing costs that would be impacted

- identify the life-cycle costs of supporting assets and services

- inform affordability and cost effectiveness analyses

For example, a costing exercise could be used to estimate how offering a new service might increase the cost of internal services, such as communications and legal services.

Level-of-service decisions

When decision-makers consider what level of service to provide or whether to discontinue a service, they can use costing information to:

- understand the cost implications of a new service, changes to an existing service or of maintaining the same level of service (status quo)

- inform cost-benefit analyses

For example, a costing exercise could be used to estimate the cost of reducing wait times at border crossings.

Charging and cost-recovery decisions

Decision-makers can use costing information to help identify the full cost of delivery. The full cost of delivery informs how much to charge.

When decision-makers must make determinations about cost recovery, they should consider the costs involved in the:

- provision of a service

- use of a facility

- conferral, by means of a licence, permit or other authorization, of a right or privilege

- provision of a product

- recovery, in whole or in part, of costs that are incurred in relation to a regulatory scheme

For example, a costing exercise could inform the amounts to charge for:

- interdepartmental enterprise services

- patent application processing and patent administration

Investment decisions

When decision-makers consider whether to undertake an investment, they can use costing information to understand the long-term financial implications of their decision. Costing information also supports the understanding of the financial obligations imposed by the investment and the cost variances that are incurred over the entire life cycle of an asset or service.

For example, a costing exercise could be used to estimate the cost of a building that is constructed and maintained by the Government of Canada.

Contracting and procurement decisions

When decision-makers must decide which option represents best value, they can use costing information to inform contract negotiations and the contracting authority required.

For example, a costing exercise could be used to estimate the cost uncertainty and risk associated with a particular initiative or activity, which would subsequently inform price negotiations and risk-sharing considerations.

Decisions about reorganizations

When decision-makers consider a reorganization that impacts existing organizations or the creation of a new organization, they can use costing information to inform the:

- parties involved about the cost implications

- resulting reference levels

For example, a costing exercise could be used to estimate the cost of transferring responsibility for a program, including the costs of a program, as well as the indirect costs of internal services that support the program.

Assessments of results

When assessing the impacts of an initiative or activity, both financial and non-financial elements should be considered. As part of the assessment, costing information can inform:

- evaluations that assess the efficiency of an initiative or activity

- ongoing monitoring of an initiative or activity

Appendix B: definitions

- assumptions

- The underpinning hypotheses upon which a costing exercise is built and from which the costing requirements are drawn. Assumptions use evidence to make judgments to fill the gaps between input data and the results of the costing exercise. They are deemed to be true in the absence of facts and supported by data when possible. An example of an assumption might be the size of the team required to manage a program before an organizational chart is approved.

- complexity

- The degree to which an initiative or activity is difficult to understand, analyze, verify and assess, or the degree to which it consists of many different and connected parts.

- contingency

- An amount that is established in a costing exercise to allow for items, conditions, or events for which the state, occurrence, or effects are uncertain, and that experience has shown would most likely result in additional costs. The objective of establishing a contingency is to inform realistic budgets based on the risk assessment and the risk tolerance of decision-makers, which can vary by initiative or activity.

- cost

- The monetary value of the resources (for example, human, physical) consumed to achieve a certain end.

- cost breakdown structure (CBS)

- A hierarchical structure that is used to break down costs into lower levels of detail so that the total cost related to an initiative or activity can be produced. To construct a CBS, overarching cost elements are subdivided into smaller cost elements to produce multiple levels of hierarchy. The subdivided cost elements are called “children” and they should be equal to the sum of the related cost elements at the next level up, which is called the “parent.”

- cost driver

- A variable that has a significant influence on the cost of an initiative or activity. From a cost-modelling perspective, cost drivers represent the input variables that have the greatest impact on the output cost. When applicable, cost drivers are used as the input parameters for cost estimating relationships.

- cost estimating relationship (CER)

- A mathematical relationship that defines cost as a function of one or more parameters, such as performance, operating characteristics and physical characteristics. A CER uses cost drivers as input parameters to predict a future cost.

- cost report

- A report that describes the costing process, ground rules, assumptions, data sources, results, and lessons learned for future costing practitioners, challenge functions, evaluators, performance measurement practitioners and auditors. Cost reports should be prepared for all costing exercises.

A cost report should:

- provide a thorough understanding of how the costing information was produced

- allow readers to assess the credibility and maturity of the costing information

- be able to withstand scrutiny and an audit

- allow a third party to reproduce the results

- costing

- Costing consists of the calculation of resources (for example, human, physical, financial) consumed to achieve a certain end. Costing is used to support decision-making, such as determining the cost of providing a service or the cost of acquiring capital equipment. Costing in the Government of Canada includes:

- cost accounting, which emphasizes the allocation of costs (for example, direct and indirect)

- cost estimating, which emphasizes forecasting costs and the associated uncertainty and risk

- costing exercise

- The use of a standardized process and the application of costing approaches and techniques to determine costs.

- costing information

- The value of the resources (human, physical or financial) consumed to serve a specific purpose. The most useful costing information is credible, as defined in Credible costing information in this guide.

- costing practitioner

- A person who performs work related to costing.

- cost risk

- Cost risk is something that may or may not occur and that may increase or decrease cost. Considering cost risk involves assessing the probability of a risk materializing and the impact on cost if it does. An example of cost risk is a potential mechanical breakdown in a manufacturing environment.

- cost uncertainty

- Cost uncertainty stems from fluctuations in costs. The exact impact of cost uncertainty is unknown due to imperfect information. However, uncertainty can be estimated using data. An example of cost uncertainty is the future foreign exchange rate for materials or services procured in foreign currency.

- deterministic estimate (point estimate)

- A single value that represents the proposed cost of an initiative or activity selected from within a range of potential outcomes. A deterministic estimate can be adjusted for cost uncertainty and risk by adding a contingency based on a cost uncertainty and risk analysis. A deterministic estimate is also known as a point estimate.

- expert opinion

- A claim, made by an individual or group asserted to be sufficiently knowledgeable in a subject, that provides reliable testimony on the issue at hand. Expert opinion as a costing technique tends to produce subjective costing information, but it may be useful in the absence of other viable alternatives. Expert opinion may also be referred to as subject matter expert opinion.

- ground rules

- A prescribed set of conditions that provide guidance to the direction of a costing exercise. Ground rules often become constraints that define the boundaries and scope of the costing exercise. For example, a ground rule for a construction project may be that all materials are to be procured in Canada

- independent estimate

- A costing exercise conducted by a third-party reviewer who uses different methods and sources of data to develop an estimate and compare it to the primary estimate. An independent estimate is prepared by an entity that is not under the supervision, direction, advocacy or control of the people responsible for developing or acquiring the initiative or activity. An independent estimate is conducted with objectivity, and such an estimate should preserve the integrity of a costing exercise by prioritizing the credibility.

- life-cycle costs

- All the costs associated with an initiative or activity over its life cycle, which includes the costs from initial conception and during any operational periods (for example, operations and maintenance) until the end of the initiative or activity or the disposal of any assets.

- materiality

- The degree to which something is important, relevant or significant. From a decision-making perspective, an item of information or an aggregate of items is material if it is probable that the item’s omission or misstatement could influence or change a decision. For example, a component that costs $1,000 and is part of a $1 million initiative is not likely to be considered material. However, a $1 million initiative would be material for an organization that has a budget of $20 million.

- normalization

- The process of removing the effects of external influences from a set of data to improve consistency and comparability. For example, adjusting data for inflation or the value of money over time.

- quality assurance

- An action that includes a verification of the ground rules, assumptions and requirements of the costing exercise, as well as a quality check on the calculations in the costing exercise. Quality assurance is focused on the integrity and appropriateness of the process used to develop the costing information.

- sensitivity analysis

- The repetition of an analysis with different quantitative values for selected assumptions or cost drivers for the purpose of comparing the results with the basic analysis. If a small change in the value of an assumption or cost driver results in a large change in the results, the results are sensitive to that assumption or cost driver. Sensitivity analysis provides an analysis of the impact that a change in the most influential cost drivers or assumptions will have on the overall costs of an initiative or activity.

- validation

- An action to ensure that the results of an analysis reflect the real world by demonstrating that the results are reasonable when compared to past performance, comparable or historical examples, independent estimates or recognized benchmarks. Validation is focused on the appropriateness and accuracy of the result.