ARCHIVED - Performance Reporting: Good Practices Handbook 2011

This page has been archived.

This page has been archived.

Archived Content

Information identified as archived on the Web is for reference, research or recordkeeping purposes. It has not been altered or updated after the date of archiving. Web pages that are archived on the Web are not subject to the Government of Canada Web Standards. As per the Communications Policy of the Government of Canada, you can request alternate formats on the "Contact Us" page.

Performance Reporting: Good Practices Handbook 2011

Table of Contents

- Performance Reporting: Good Practices Handbook

- Government of Canada Reporting Principles

- Principle 1: Focus on the benefits for Canadians, explain the critical aspects of planning and performance, and set them in context

- Principle 2: Present credible, concise, reliable, and balanced information

- Principle 3: Associate performance with plans, priorities, and expected results, explain changes, and apply lessons learned

- Principle 4: Link resources to results

- Contacts

Performance Reporting: Good Practices Handbook

Performance Reporting: Good Practices Handbook is a practical resource to be used in conjunction with the Guide to the Preparation of Part III of the Estimates to support federal organizations in preparating their respective Departmental Performance Reports (DPRs).

This handbook is structured according to the Government of Canada Reporting Principles, principles that have been developed to guide public performance reporting and serve as the conceptual foundation for the federal reporting context.

Government of Canada Reporting Principles

The following Government of Canada Reporting Principles, taken together, show the link between plans, performance, and achievements, and their application demonstrates a departmental commitment to managing for results.

Principle 1: Focus on the benefits for Canadians, explain the critical aspects of planning and performance, and set them in context.

- Clearly present the program activity architecture (PAA).

- Discuss priorities within the context of the Management, Resources and Results Structure (MRRS).

- Link to the whole-of-government framework.

- Demonstrate links to broader government priorities.

- Discuss challenges, risks, opportunities, and their impact on plans and performance.

- Discuss horizontal links.

- Describe delivery mechanisms.

- Include responses to parliamentary committees and findings of the Office of the Auditor General of Canada.

Principle 2: Present credible, concise, reliable, and balanced information.

- Use the MRRS as the basis of reporting.

- Report positive and negative aspects of performance.

- Provide factual, independently verifiable, evidence-based performance information.

- Provide informative financial tables.

- Use comparisons and trends.

- Provide links to further information.

Principle 3: Associate performance with plans, priorities, and expected results, explain changes, and apply lessons learned.

- Link performance to plans.

- Discuss lessons learned and corrective actions.

Principle 4: Link resources to results.

- Link resources to results.

- Discuss changes in resources.

To use and navigate this resource, explanations and illustrations of how to apply the Government of Canada Reporting Principles when preparing performance reports are provided. For each Government of Canada Reporting Principle and related criteria, a link to an example in a DPR is given that demonstrates a commendable and effective application of the Reporting Principle.

Principle 1: Focus on the benefits for Canadians, explain the critical aspects of planning and performance, and set them in context

Why should public performance reports focus on the benefits for Canadians? When preparing the DPR, it is important to recall why Reports on Plans and Priorities (RPPs) and DPRs are prepared, how they are used, and by whom. These reports are key accountability documents that present the government’s financial and non-financial plans and performance, and they are subject to parliamentarians’ scrutiny. The government is spending taxpayers’ money, and parliamentarians represent Canadians. Departmental reports should therefore demonstrate how the lives of Canadians will be and are improved by departments’ plans and results.

Focusing on the few critical aspects of planning and performance enhances the usefulness of public reports by providing a concise picture of the information parliamentarians need to know. Parliamentarians do not have unlimited time to read through RPPs and DPRs and need to be able to get clear messages about departmental planning and performance quickly. Too much information impedes the ability of parliamentarians to hold the government to account.

Identifying critical aspects of planning and performance involves assessing what is relevant and significant for each strategic outcome and program activity. Information in RPPs and DPRs should be relevant to members of Parliament and to Canadians, and such information should explain the benefits for Canadians that the department aims to achieve through its strategic outcomes and program activities. Reporting on other critical items that have an impact on plans or performance is recommended; it could include a description and a discussion of how such items are expected to, or did, affect departmental plans and performance.

Establishing the context of plans and performance is important because it helps readers understand the range of considerations that must be taken into account when planning and that affect performance. It also helps to establish reasonable parameters for assessing plans and performance.

To apply this principle:

- Clearly present the program activity architecture.

- Discuss priorities within the context of the MRRS.

- Link to the whole-of-government framework.

- Demonstrate links to broader government priorities.

- Discuss challenges, risks, opportunities, and their impact on plans and performance.

- Discuss horizontal links.

- Describe delivery mechanisms.

- Include responses to parliamentary committees and findings of the Office of the Auditor General of Canada.

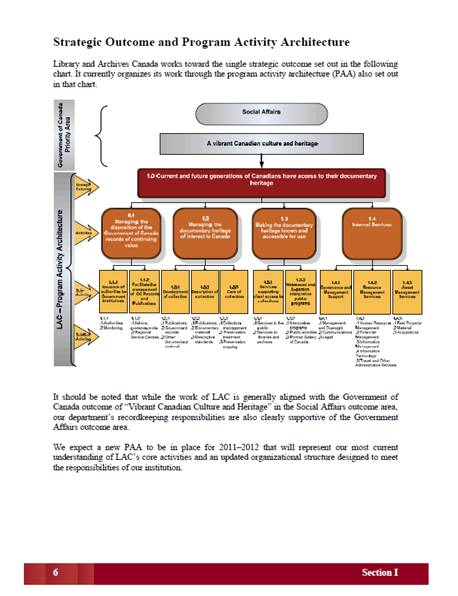

Clearly present the program activity architecture

Explaining the critical aspects of planning and performance begins with their identification. In large part, articulating the department’s core objectives and the key results to which it is committed will achieve this first step. Because the MRRS guides decision making and is the basis for managing for results, the strategic outcomes and program activity architecture (PAA) will serve as the framework through which to explain the department’s critical aspects of planning and performance.

Consequently, presenting a clear PAA is key for putting this principle into practice. It should be clear in the report what the strategic outcomes and program activities are and how they are connected. Presenting the PAA visually and through discussion is an effective way of communicating this information to readers. The DPR should use the same PAA as the one presented in the corresponding RPP. In exceptional circumstances, a new PAA may be used, subject to Treasury Board approval. Should this occur, it is important to provide a crosswalk and discuss the impact on performance.

Good practice: Clearly present the PAA (i.e., development of a PAA along with its clear use).

PAAs have stabilized since the inception of the Policy on Management, Resources and Results Structures (MRRS) in 2005, with 90 per cent of departments presenting a clear PAA in the DPRs. The example below demonstrates the maturity of PAA reporting structures and the development of a PAA along with its clear use.

Why is the following a good practice? The DPR presents a clear inventory and logical relationship of its strategic outcome and program activities. The PAA is at a sufficient level of materiality to reflect how a department allocates and manages the resources under its control to achieve intended results.

Good practice example: Library and Archives Canada DPR 2009–10

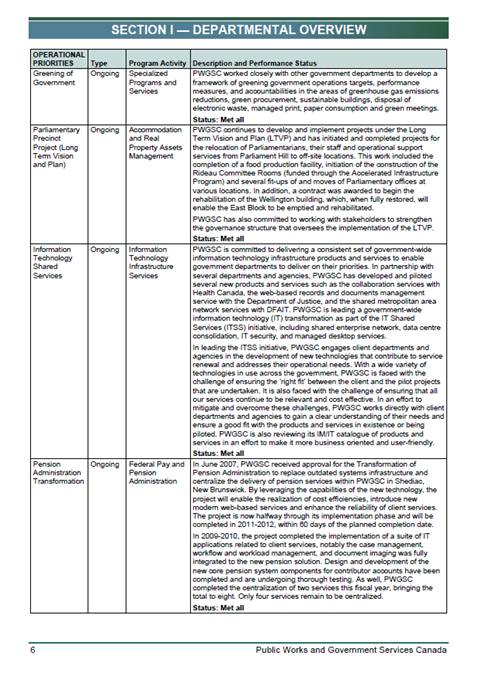

Discuss priorities within the context of the MRRS

Certain items may be identified as taking precedence over others in order for progress to be made toward the strategic outcomes; these may change from year to year or within a single reporting cycle. Any priorities identified in the RPP and DPR should be discussed within the context of the MRRS, and the linkages between priorities and program activities should be clearly demonstrated. Specifically, how the priorities are expected to contribute to the strategic outcomes should be discussed so that readers understand their relative importance.

Good practice: Discuss priorities within the context of the MRRS.

Why is the following a good practice? The linkages between priorities and program activities are clear. Detail is provided on the performance status for meeting expected results and the corresponding departmental priorities.

Good practice example: Public Works and Government Services Canada DPR 2009–10

Link to the whole-of-government framework

As a complement to departmental performance measurement and reporting, the Government of Canada has developed a whole-of-government framework for reporting to Parliament. This framework maps the financial and non-financial contributions of organizations receiving appropriations to a set of 16 Government of Canada outcome areas. These outcome areas are high-level results that the Government of Canada is aiming to achieve. The outcome areas are grouped according to the four Government of Canada spending areas: Economic, Social, International, and Government Affairs.

Because the alignment of program activities to the whole-of-government framework makes it possible to calculate spending by Government of Canada outcome area and also accurately calculate overall expenditures, a program activity should be aligned to only one Government of Canada outcome area. A grid is an effective visual means of showing how the department’s program activities are aligned with Government of Canada outcome areas.

The whole-of-government framework is the reporting structure used in Canada’s Performance, an annual report to Parliament on the federal government’s contribution to Canada’s growth and performance as a nation. This report aims to give parliamentarians and Canadians an understanding of how departments together contribute to the broader, government-wide outcomes that comprise the framework.

Good practice: Link to the whole-of-government framework.

Why is the following a good practice? The DPR discusses the contribution of program activities to the whole-of-government framework and broader Government of Canada outcome areas.

Good practice example: Parks Canada DPR 2009–10

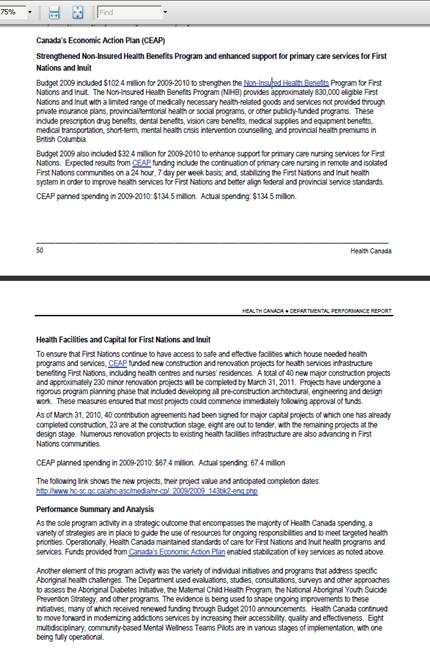

Demonstrate links to broader government priorities

In addition to the whole-of-government framework, another context in which to situate departmental outcomes is current government policy. The broader priorities and plans of the government are established at the beginning of a session of Parliament in the Speech from the Throne and annually in the federal budget. While Government of Canada outcome areas are meant to endure beyond the mandate of a particular government, the Speech from the Throne and the budget provide a picture specific to the current government.

Therefore, there should be an indication of how the department’s outcomes relate or contribute to the broader government priorities established in the Speech from the Throne or the budget. Other government-wide initiatives could also be referenced and discussed in terms of their impact on the plans and performance of the department.

It is recognized that the Speech from the Throne and the budget are overarching documents and that it may be difficult for some organizations (particularly smaller ones) to link their mandates to these documents.

Good practice: Demonstrate links to broader government priorities.

Why is the following a good practice? Throughout the DPR there are references to the government’s broader priorities, including discussions of key activities at the sub-program activity level (pages 50 and 51) that received the direct attention of budget announcements.

Good practice example: Health Canada DPR 2009-10

Good practice (example 2): Demonstrate links to broader government priorities (Economic Action Plan reporting).

Why is the following a good practice? Given the high-priority status of the Economic Action Plan (EAP), reporting focused on making clear links between program activities and departmental contributions to outcomes related to the EAP. A summary is provided on page 11 in Section I, and program activity links are consistently made throughout Section II.

Good practice example: Infrastructure Canada DPR 2009–10

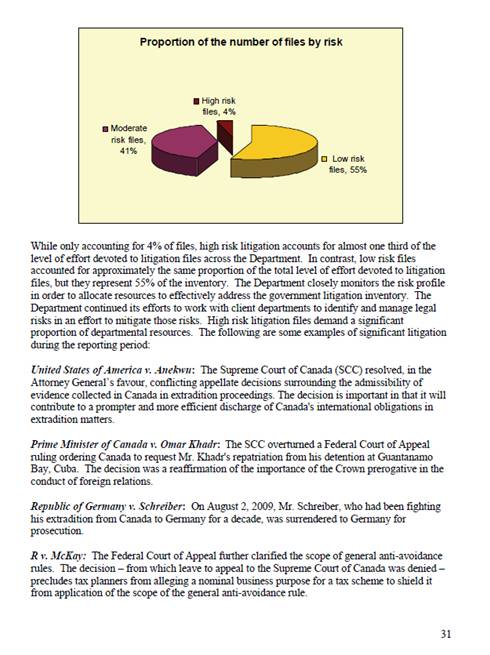

Discuss challenges, risks, opportunities, and their impact on plans and performance

Description and analysis of the operating environment and the strategic context for the reporting period provide a frame of reference for readers to understand and assess the plans and results of the department.

Internal and external challenges, risks, and opportunities (including management and human resources capacity considerations) should be identified at the departmental level. Explanations of how these will affect plans and performance and how they will be addressed in delivering program activities or key programs and services are also essential.

Good practice: Discuss challenges, risks, opportunities, and their impact on plans and performance.

Why is the following a good practice? The risk analysis section provides a clear sense of the organization’s operating environment. Section I presents the key challenges, trends, and risks that shaped and impacted the department’s work. Section II of the DPR provides additional details on the specific risks that were addressed throughout the year.

Good practice example: Department of Justice DPR 2009–10

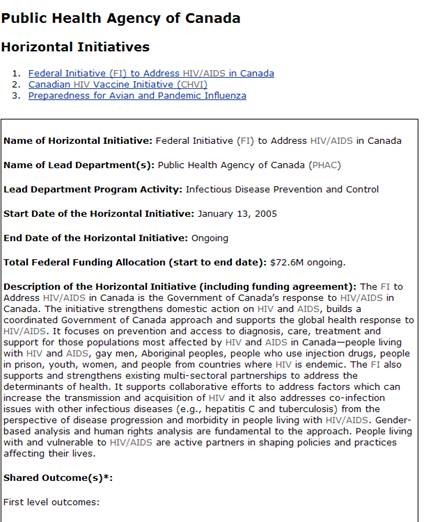

Discuss horizontal links

Increasingly, the work of federal organizations is done through horizontal partnerships and initiatives. Indicating the department’s involvement in horizontal partnerships and initiatives contributes to an understanding of the operating environment and guides readers to other sources of information on topics and issues of interest.

Important horizontal linkages and involvement in government-wide initiatives should therefore be identified, and their planning and performance implications should be explained.

Good practice: Discuss horizontal links.

Why is the following a good practice? In this example, the agency comprehensively presents horizontal initiatives for which it is the lead. Shared outcomes and targeted results to be achieved by all partners involved are itemized.

Good practice example: Public Health Agency of Canada DPR 2009–10 (Horizontal Initiatives Table).

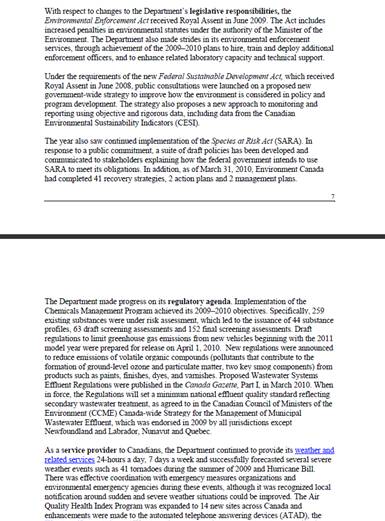

Describe delivery mechanisms

Delivery mechanisms are the ways in which programs and services are supplied to Canadians. These include (but are not limited to) policies, programs and services, regulations, and grants. In large part, this is how Canadians will see themselves in public performance reports. Clearly describing this interface provides key contextual information regarding the benefits gained by Canadians in the delivery of programs and services, and it illustrates how their tax dollars are put to use.

The extent to which delivery mechanisms are appropriate, equitable, and properly managed, including the sound stewardship of resources, should be concisely demonstrated in both the planning and performance reports, using links to further information as required.

Given the range of mechanisms available, the department should also indicate why its choice of public policy instrument is the most appropriate and effective for achieving policy objectives. Service improvement activities that affect the department’s delivery mechanisms should also be part of the discussion.

Good practice: Describe delivery mechanisms.

Why is the following a good practice? In this example, the department identifies the principal means by which its programs and services are delivered to Canadians, for example, its role in legislation, regulation, and service delivery. Clearly describing this interface provides key contextual information regarding the benefits gained by Canadians in the delivery of its programs and services. It also illustrates how the department goes about spending public tax dollars.

Good practice example: Environment Canada DPR 2009–10

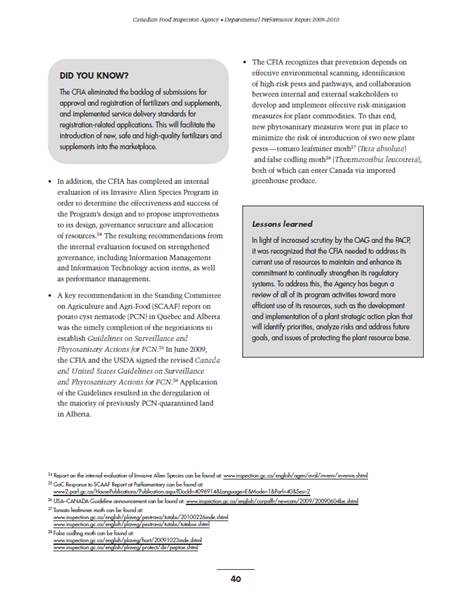

Include responses to parliamentary committees and findings of the Office of the Auditor General of Canada

The relationship between departments and Parliament is integral to Canada’s system of government and is not limited to the annual tabling of RPPs and DPRs. All interaction between the department and Parliament, including responses to parliamentary committees and findings of the Office of the Auditor General of Canada, who is an officer of Parliament, should be clearly documented in the report.

The report should include summaries of findings and responses and, keeping in mind the goal of comprehensive but succinct reports, provide Web links to the full versions. Information about how the department intends to take (specific) action can also be provided via Web links; this information may already be part of the response. Identifying actions to be taken illustrates an approach to management that incorporates lessons learned and demonstrates how the relationships between Parliament and departments produce positive change.

It should be noted that this good practice is also one of the recommendations (Recommendation No. 18) put forth in the sixth report of the House of Commons Standing Committee on Government Operations and Estimates, released in September 2003.

Good practice: Include responses to parliamentary committees and findings of the Office of the Auditor General of Canada.

Why is the following a good practice? In this example, the agency discusses a report by the Office of the Auditor General to Parliament. Specific actions are described, and a link to the full departmental response is included.

Good practice example: Canadian Food Inspection Agency DPR 2009–10

Principle 2: Present credible, concise, reliable, and balanced information

There is a common perception among users of public performance reports that the objectivity of such reports is questionable, which consequently puts into question their usefulness to parliamentarians. Concern over the reports containing only positive news means they are not seen as valuable tools to help parliamentarians in their work of holding the government to account and of communicating with their constituents how Canadians benefit from government programs and services.

It is important that a coherent, sound, and balanced picture of performance be presented in the DPR, ideally through a combination of qualitative and quantitative data, so that readers can be confident of the validity and reliability of the information presented. This requires departments to acknowledge where performance did not meet expectations, provide the necessary explanations as to why, and describe the corrective actions that will be taken in the future. Acknowledging performance that did not meet expectations and explaining why shows that an organization is willing to adapt.

The role of evaluation in applying this principle should be highlighted. Evaluation provides evidence-based, neutral assessments that are required to produce reporting that is credible, reliable, and balanced.

Concise reporting is a key element of this principle because of its potential for increasing the usefulness of performance reports. A concise style of reporting focused on the critical aspects of departmental planning and performance will provide parliamentarians with the information required to consider departmental spending plans and performance.

To apply this principle:

- Use the MRRS as the basis of reporting.

- Report positive and negative aspects of performance.

- Provide factual, independently verifiable, evidence-based performance information.

- Provide informative financial tables.

- Use comparisons and trends.

- Provide links to further information.

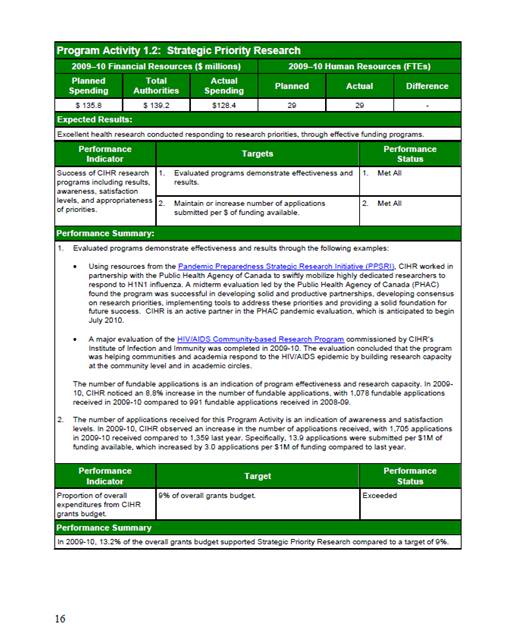

Use the MRRS as the basis of reporting

For performance information, both financial and non-financial, the MRRS establishes a common approach for its collection, management, and reporting. The MRRS also provides a standard basis for the activities of planning, managing, and reporting. It is a logical organization of the programs being delivered (described by the PAA) and the benefits to Canadians that departments are working to achieve (i.e., strategic outcomes). A key to the success of the Policy on Management, Resources and Results Structures is the development of systems for producing credible and reliable performance information as indicated in the Performance Measurement Framework (PMF).

The performance story presented in the report should be framed within the context of program activities and how they contribute to the progress made on achieving strategic outcomes. Reporting on a key sub-activity is acceptable when discussed within the context (and in support) of reporting on program activity performance.

Reporting on the basis of the MRRS enables parliamentarians to follow the story—from plans to actual spending to actual results.

Good practice: Use the MRRS as the basis of reporting.

Why is the following a good practice? The overall basis of reporting is the PAA. The agency includes program activity performance indicators and targets from the agency’s approved MRRS. Performance indicators and targets measure progress toward the success of the program activity.

Good practice example: Canadian Institutes of Health Research DPR 2009–10

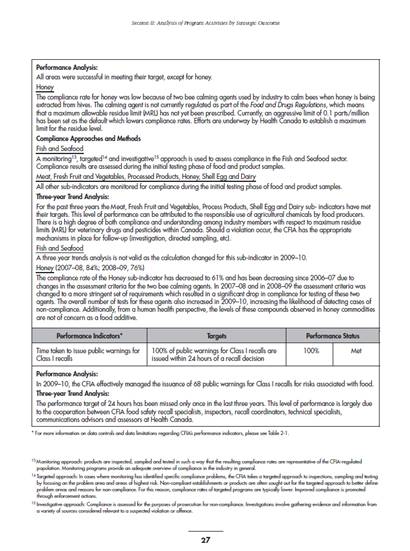

Good practice (example 2): Use the MRRS as the basis of reporting (trend analysis).

Why is the following a good practice? The DPR provides a rigorous performance analysis based on the supporting performance measurement framework (pages 27 and 28), including three-year trend analyses.

Good practice example: Canadian Food Inspection Agency DPR 2009–10

Report positive and negative aspects of performance

Balanced reporting enhances the credibility of reporting. Moreover, reporting on both the positive and negative aspects of performance meets the intention of public performance reporting, i.e., to provide the necessary information for scrutiny and decision making.

Performance information is not fairly presented when the information is limited to successes and minimizes, or even avoids, discussion of matters that did not unfold as planned. In order for reporting to be fair, key information must not be omitted. When discussing results achieved, departments should discuss what went according to plan as well as cases where things did not go according to plan but risks were mitigated. Departments should also discuss results that were not achieved, noting how and why plans were not implemented as intended. It is also important to include explanations of how the department uses both positive and negative results to make adjustments and improvements toward achieving its strategic outcomes. Findings that emerge from evaluations are important sources of information in framing these discussions.

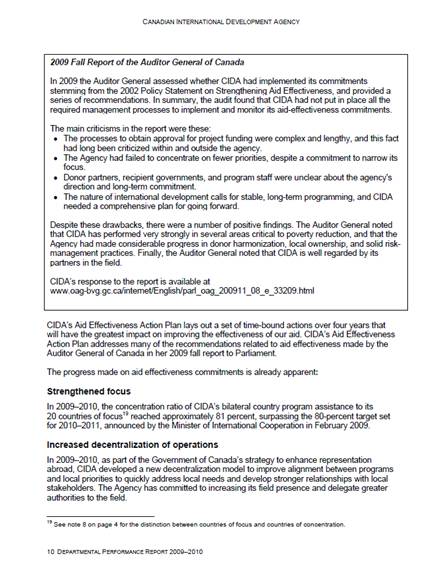

Good practice: Report positive and negative aspects of performance.

Why is the following a good practice? The DPR’s discussion of performance exhibits a transparent approach to reporting. Up front is a discussion (page 10) of shortfalls and results of an audit.

Good practice example: Canadian International Development Agency DPR 2009–10

Provide factual, independently verifiable, evidence-based performance information

Discussion of the department’s performance should be substantiated with factual, independently verifiable, evidence-based information. Balanced, evidenced-based reporting leads to realistic conclusions about the department’s performance and gives readers confidence in those conclusions.

In order for readers to have confidence in the methodology and data used to substantiate reported performance, an indication of the validity and credibility of data used should be provided. This can be achieved by indicating the source of the information, particularly if graphs or tables are presented. A brief discussion of the measures taken to ensure the reliability of the data upon which the performance report is based is also important, whether for data from internal sources or for data collected from external partners. Both qualitative and quantitative data are sources of valid performance information. Limitations or problems with the underlying data and any caveats regarding proper interpretation of the information reported should also be noted.

Identifying sources of data (information) is critical to establishing credibility. It offers readers the opportunity to directly validate what has been included in the report and provides a reference point when seeking further information.

For example, when presenting survey data in performance reports, providing information on the quality and limitations of survey results helps substantiate performance claims. The importance of this criterion is highlighted in the 2005 November Report of the Auditor General of Canada,Chapter 2, “The Quality and Reporting of Surveys.”[1]

Findings presented in approved evaluation and audit reports can be a key credible source of performance analysis. Departments should reference any significant findings, explain the relationship to departmental performance, and identify the next course of action to improve departmental results.

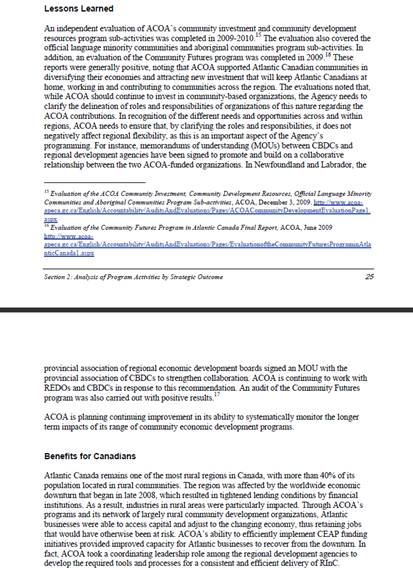

Good practice: Provide factual, independently verifiable, evidence-based performance information (use findings of audits and evaluations in performance discussions).

Why is the following a good practice? Throughout the DPR, numerous references are made to evaluations and internal management reviews. Results of an evaluation are discussed in the context of redesigning program delivery.

Good practice example: Atlantic Canada Opportunities Agency DPR 2009–10

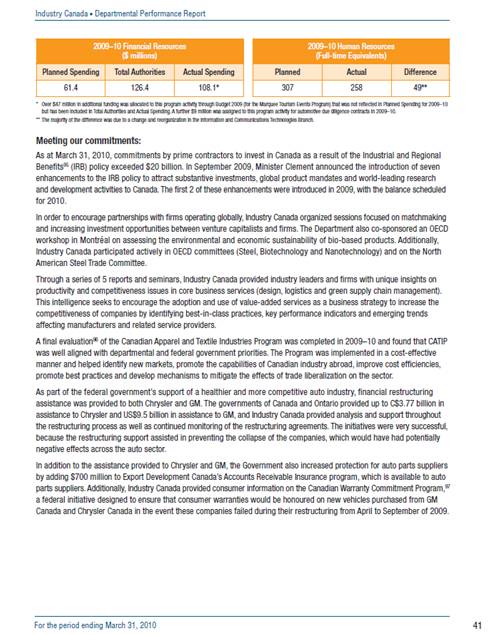

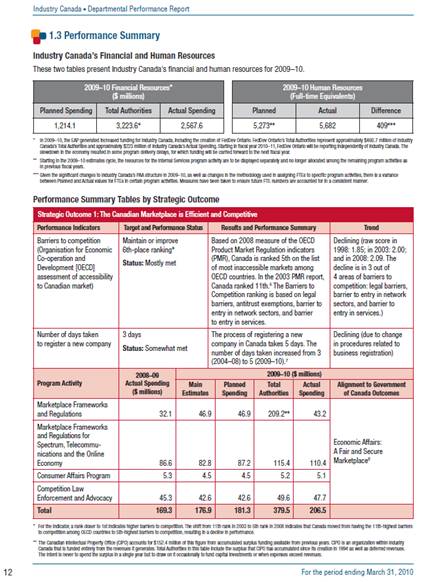

Good practice (example 2): Provide factual, independently verifiable, evidence-based performance information (data).

Why is the following a good practice? The DPR discloses the level of assurance on the reliability and relevance of performance information. The reader has a clear understanding of where and how the information was obtained. The DPR identifies sources of data, and any limitations or problems with underlying data are reported.

Good practice example: Industry Canada DPR 2009–10

Provide informative financial tables

Basic to performance reporting is linking resources to results (to be discussed in more depth under Principle 4); therefore, an accurate and thorough presentation of financial tables (i.e., resources) is key for ensuring accountability to Parliament. In addition, financial tables illustrate the link to the appropriations given to departments through the supply process. The content, layout, and format of financial tables need to be clear and easy to understand and interpret, thereby contributing to the user-friendliness of the report.

Immediately following financial tables should be a discussion of their content. Just as the tables should be easy to understand and interpret, explanations of their content should be clear, simple, and effective so that a layperson can interpret the information, see links between resources and results, and make informed conclusions.

There should also be a hyperlink in the report that brings the reader directly to the departmental financial statements.

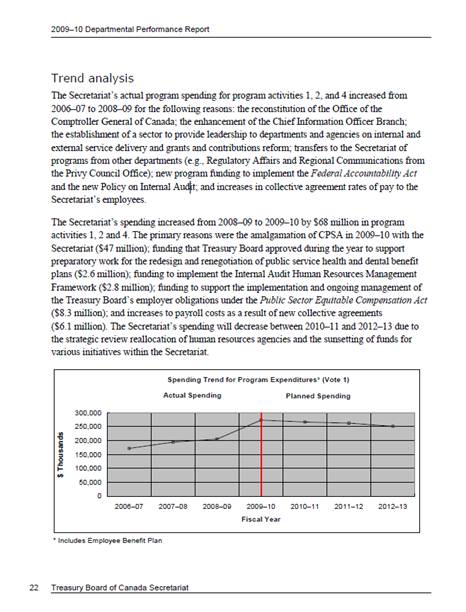

Good practice: Provide informative financial tables (Expenditure Profile).

Why is the following a good practice? The financial tables in this DPR are presented clearly and are easy to understand. Included is a discussion of the financial trends that emerge from an analysis of the data. Explanations are effective in integrating financial tables to non-financial performance discussions in the report. Altogether, financial information underpins non-financial performance.

Good practice example: Treasury Board of Canada Secretariat DPR 2009–10

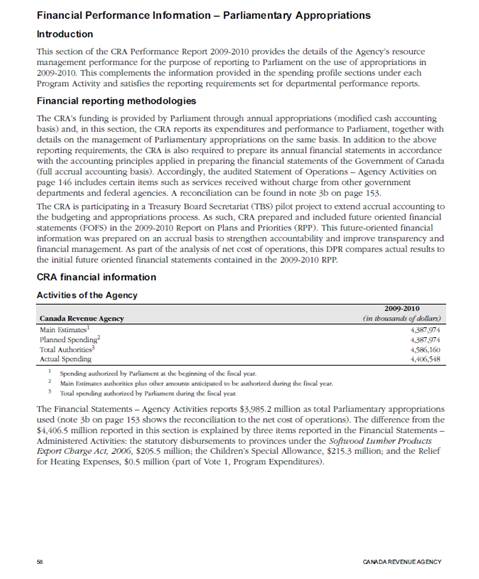

Good practice (example 2): Provide informative financial tables (financial highlights).

Why is the following a good practice? Expenditure tables and financial information are clear throughout the report, with good explanations of variances in the expenditure profile found on pages 23 to 25. Text supporting the tables and graphics is at a level of reporting that conveys meaningful understanding of the agency’s financial position and costs of operations; for example, the report provides the program-level reasons that influenced changes in its costs of operations (pages 58 and 59). The DPR also includes the analysis of its costs of operations in the context of a comparison with its future-oriented financial statements.

Good practice example: Canada Revenue Agency DPR 2009–10

[1]. 2005 November Report of the Auditor General of Canada

Use comparisons and trends

Comparisons of performance by similar organizations or between jurisdictions add credibility to performance data collected by the department. Use of comparisons can help readers better understand achievements and shortcomings in performance. The comparisons chosen should be relevant and informative. For example, they might include the following:

- Comparisons of the same organization between years and over time (trend information);

- Progress made at the program activity level as compared with changes at the strategic outcome level;

- Indicators (e.g., prenatal health practices versus infant mortality rate); and

- Actual performance against baseline information, targets, service standards, and benchmarks.

Good practice: Use comparisons and trends.

Why is the following a good practice? Comparative information is consistently presented throughout the DPR to assess actual performance. In this example, comparative information is provided against indicators, including an assessment of trends.

Good practice example: Industry Canada DPR 2009–10

Provide links to further information

A results-focused style of reporting that explains the critical aspects of departmental planning and performance will provide parliamentarians with the information they require throughout the supply process. One way of achieving this concise style is to include electronic links in the report, which is an effective way of providing readers with additional information without adding unnecessary length. Supplying electronic links allows stakeholders who are interested in the finer details of the performance story to read the particulars.

Overall, an increased focus on a concise style of reporting will ensure that accountability and performance information is at the forefront of the DPR while improving the clarity and user-friendliness of the document.

Good practice: Provide links to further information.

Why is the following a good practice? The department directs readers to its website to allow readers to drill down to supplementary electronic data. This is a good example of the use of the Web layer to capture sub-program activity details.

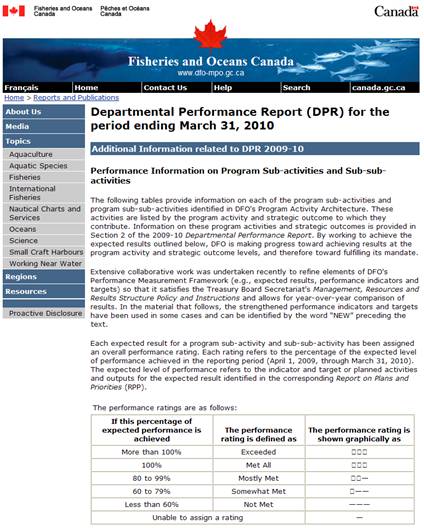

Good practice example: Department of Fisheries and Oceans DPR 2009–10

Principle 3: Associate performance with plans, priorities, and expected results, explain changes, and apply lessons learned

The core elements of a performance report are descriptions of what an organization planned to accomplish, how the actual results compare with those plans, an explanation of any significant differences, and identification of lessons learned. Information contained in the RPP and the DPR should facilitate comparisons between reports and over time.

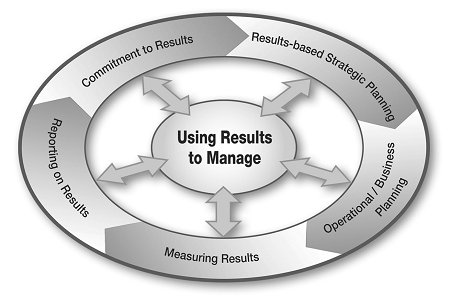

This touches on the essentials of results-based management. Results-based management is a life-cycle approach to management that integrates strategy, people, resources, processes, and measurements to improve decision making, transparency, and accountability. The approach focuses on achieving outcomes, implementing performance measurement, learning and changing, and reporting performance, as illustrated in the following diagram:

Text Version: Using Results to Manage

Planning involves the articulation of strategic choices in light of past performance and includes information on how an organization intends to deliver on its priorities and achieve associated results.

Measurement and assessment are practices through which progress is determined. Performance measurement and evaluation present valuable opportunities to learn and adjust so that the intended results may be achieved.

The final stage of the life-cycle approach involves reporting on results through the presentation of integrated financial and non-financial information. Results-based information is used for both internal management purposes and for external accountability to Parliament and Canadians. The reporting phase also provides managers and stakeholders with the opportunity to reflect on what has worked and what has not, a process of learning and adjusting that feeds into the next planning cycle.

To apply this principle:

- Link performance to plans; and

- Discuss lessons learned and corrective actions.

Link performance to plans

At its most basic, linking performance to plans means ensuring that the RPP and DPR are consistent in terms of form and content. Reporting on the basis of the MRRS will go a long way in ensuring a common framework (strategic outcomes and program activities) for the two reports and generating a cohesive planning and performance story.

Readers should not have to question the consistency between the reports. Changes to plans and how those changes affected expected results need to be explained. Plans presented in the RPP but not discussed in the DPR are misleading, as are restatements of the expected results from the RPP in different terms in the DPR.

Linking performance to plans should consist of reporting performance against plans and expected results. This can be accomplished by using performance indicators and measures and reporting against targets, service standards, baselines, benchmarks, etc. In addition, for each expected result, a status should be assigned, based on performance against those indicators and measures, as a means to validate performance.

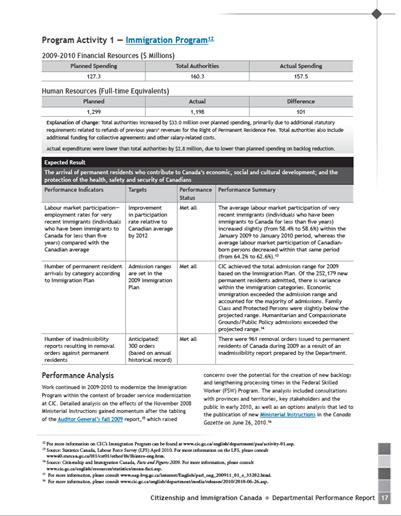

Good practice: Link performance to plans.

Why is the following a good practice? The DPR assesses performance against the planned results and performance expectations set out in the RPP. Performance is discussed in relation to expected results, indicators, and targets. The performance summary and analysis supports the performance status assigned.

Good practice example: Citizenship and Immigration DPR 2009–10

Discuss lessons learned and corrective actions

Revising and improving plans are indications of sound management practices. Departmental plans are expected to change in response to, among other things, lessons learned from past performance. Changes resulting from lessons learned during the reporting period should therefore be explained. The effect of these changes on actual planning and performance, and in measuring and reporting on performance, should also be discussed.

The first thing to do is identify the lessons learned and actions taken as a result. Departments should demonstrate to readers that lessons learned are systematically tracked and, in turn, purposefully applied in order to adjust plans. This shows a commitment to continuous learning and improvement. For example, the RPP identifies corrective or strategic actions to be taken as a result of lessons learned discussed in the previous DPR; the DPR then reports on those actions. The DPR should also communicate new lessons learned over the reporting period. Other details to include in the discussion are the sources of any lessons learned (e.g., an audit, an evaluation, performance measurement data), innovative ways of identifying and using lessons learned, evidence of using good practices to improve managing for outcomes, and evidence of integrating lessons learned into plans and discussing the result of their adoption on performance.

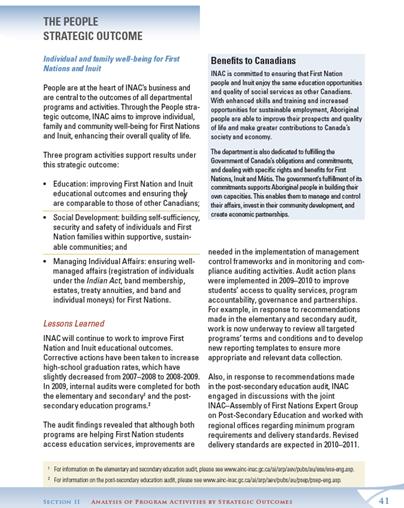

Good practice: Discuss lessons learned and corrective actions.

Why is the following a good practice? Throughout the DPR, the department discusses lessons learned and explains actions that will be taken to address missed targets and plans. Sources of lessons learned are provided. In this example, lessons learned are reported at the program level.

Good practice example: Indian and Northern Affairs Canada DPR 2009–10

Principle 4: Link resources to results

From a public reporting perspective, accountability fundamentally means explaining what has been accomplished with the resources entrusted to the department in relation to what was planned and demonstrating whether performance represents a responsible, efficient, and effective use of public funds. In order to assist parliamentarians in their accountability roles, their decisions about the funding of programs should be informed and influenced, in part, by program results.

Resources and expenditures (on a near-cash basis, both planned and actual) for program activities are displayed in a number of expenditure management documents, such as the Main Estimates and the RPP. The DPR therefore needs to discuss departmental results on the same basis, i.e., both resources and results should be presented at the program activity level so that parliamentarians and Canadians can track planning and performance information from one report to another and see the full picture of performance in relation to spending. In addition, the DPR should include accrual financial statements that are informative and give as complete a picture as possible of financial performance in relation to the non-financial performance discussed above.

As departments explain how program activities contribute to strategic outcomes and what influence they expect to have on longer-term outcomes through their actions, it is important that parliamentarians understand the cost.

To apply this principle:

- Link resources to results; and

- Discuss changes in resources.

Link resources to results

Planned and actual spending should be outlined in sufficient detail for readers to understand how the department performed financially. Notes to financial tables should be clear and understandable.

The relationship between planned and actual spending and expected and actual results should be explained in order to provide a full account of each program activity’s financial and non-financial resources that contributed to performance. Explanations could include, where appropriate, a discussion of actual results in relation to the actual expenses outlined in the department’s financial statements.

For each program activity in the RPP, it should be clear what the department intends to spend and what it intends to achieve over the next three years. In the DPR, it should be clear what the department spent for each program activity and what was achieved as a result of that spending, how actual spending compared with planned spending, and whether it represented value for money.

Human resources—planned and actual—should also be linked to results. An understanding of the workforce required to deliver programs and services to Canadians and to support the operations of government is essential.

Good practice: Link resources to results.

Why is the following a good practice? Throughout the DPR, the department discusses the extent to which expected results were achieved and at what cost. Tables help illustrate resource levels and the value of the actual results achieved. The discussion of the strategies employed provides an understanding of the nature of the expected results and the corresponding level of spending.

Good practice example: Infrastructure Canada DPR 2009–10

Discuss changes in resources

It is important to demonstrate that resources are being used efficiently and effectively and that expenditures correspond, in relevance and importance, to the outputs and short-term results achieved and the strategic outcomes being pursued.

Significant internal reallocations to meet emerging internal priorities or higher government priorities, or to better sustain progress toward the achievement of the strategic outcomes, should be discussed (i.e., amounts and areas affected, including the source of funds for the reallocation, the implications for human resources, and the identification of the program or initiative that received the funding). Appropriate references should also be made in the financial tables.

The report should discuss the impact of reallocation, expenditure review, or restraint exercises on the organization’s performance at the program activity level and their ability to contribute to the strategic outcome. Doing so will make the report more credible.

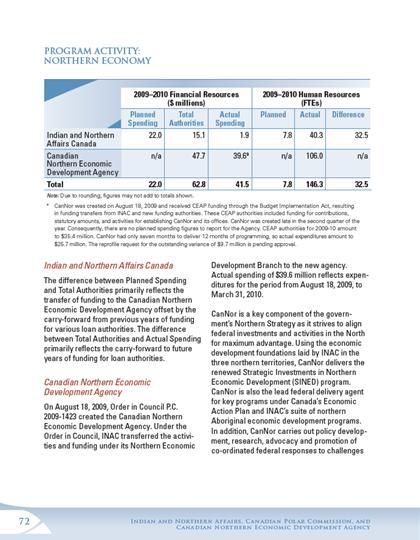

Good practice: Discuss changes in resources.

Why is the following a good practice? In this example, the DPR provides a detailed explanation of why and how resource changes took place and what programs and activities (pages 72 and 73) were responsible for carrying them out.

Good practice example: Indian and Northern Affairs Canada and Canadian Polar Commission DPR 2009-10

Contacts

Departmental Performance Reports

Reports on Plans and Priorities

Policy on Management, Resources and Results Structures

Canada’s Performance and whole-of-government reporting

canadasperformance_rendementducanada@tbs-sct.gc.ca

Policy on Evaluation