ARCHIVED - Audit of Leave and Overtime - Audit Report

This page has been archived.

This page has been archived.

Archived Content

Information identified as archived on the Web is for reference, research or recordkeeping purposes. It has not been altered or updated after the date of archiving. Web pages that are archived on the Web are not subject to the Government of Canada Web Standards. As per the Communications Policy of the Government of Canada, you can request alternate formats on the "Contact Us" page.

Audit of Leave and Overtime

Audit Report

Table of Contents

- Assurance Statement

- Executive Summary

- Introduction

- Overview

- Audit Results

- Overall Conclusion

- Appendices

Assurance Statement

Internal Audit and Evaluation (IAE) has completed a compliance audit of leave and overtime. The objective of the audit was to assess the adequacy and effectiveness of internal controls related to the administration of leave and overtime. The audit approach and methodology followed Treasury Board's Policy on Internal Audit and the Institute of Internal Auditors Standards for the Professional Practice of Internal Auditing.

The examination was conducted during the period of April through June 2008, and covered leave and overtime transactions processed for the fiscal year ending March 31, 2007.

The audit consisted of a review of applicable authorities, process walkthroughs, interviews, and an examination of overtime and leave transactions using a risk-based statistical random sampling methodology. The audit evidence gathered is sufficient to provide senior management with reasonable assurance of the results derived from this audit.

We concluded with a high level of assurance that overall, leave and overtime expenditures for the fiscal year ending March 31, 2007 within the Treasury Board Secretariat were managed in accordance with applicable laws, policies and collective agreements. However, opportunities exist to improve current practices and processes. Please see the detailed report for an assessment of each audit criterion.

In the professional judgment of the Chief Audit Executive, sufficient and appropriate audit procedures have been conducted and evidence has been gathered to support the accuracy of the opinion provided in this report. The opinion is based on a comparison of the conditions, as they existed at the time of the audit, against pre-established audit criteria. The opinion is only applicable for the entities examined and for the time period specified.

Executive Summary

Background

The audit of leave and overtime is an assurance engagement that is part of the approved Treasury Board of Canada Secretariat (Secretariat) Three Year Risk Based Audit Plan (Fiscal Year 2007-2008 to 2009-2010).

Leave is defined as an authorized absence from duty. The collective agreements and the Terms and Conditions of Employment Policy set out employees' paid and unpaid leave entitlements. Overtime is defined as time worked by an employee in excess of the standard daily or weekly hours of work and for which the employee may be entitled to compensation.

The management of leave and overtime is governed by the Public Service Employment Act, the Financial Administration Act (FAA), and a series of Treasury Board (TB) policies and collective agreements. TB Circular 1977-37: Pay Administration clarifies the overall responsibility for pay administration by assigning departments the responsibility for the integrity of the overall pay process. As well, all payments and settlements must be verified and certified pursuant to section 34 (s.34) of the FAA as governed by Treasury Board's Policy on Account Verification.

As at November 2007, the Secretariat had 1,199 full-time employees (FTE) in 13 occupational groups represented by seven different collective agreements. The Departmental unaudited financial statements for 2006-2007 reported annual salary and employee benefits of $105,488,000 as part of operating expenses. Total (Net) pay in lieu of leave amounted to $466,762. Overtime paid in cash and overtime hours worked and compensated in leave in lieu of cash payment were $1,068,892 and 4,620 hours respectively.

Objective and Scope

The objective of the audit was to assess the adequacy and effectiveness of internal controls related to the administration of leave and overtime. Specifically, the audit assessed the extent to which the control framework ensured the effective and efficient processing of leave and overtime.

This audit was primarily a compliance audit, focused on the appropriateness and effectiveness of the existing management framework in place to support leave and overtime activities and compliance with relevant regulations and departmental policies.

The audit covered the 2006-2007 fiscal year (FY) and the examination phase was conducted between April and June 2008.

Key Findings

The audit found that the Secretariat's administration of leave and overtime was compliant with applicable laws, policies and collective agreements. However, opportunities exist to strengthen the management control framework to articulate roles and responsibilities for overtime and leave management, and to include a monitoring and risk assessment exercise. As well, a more consistent and inclusive approach to overtime costs and overtime forecasts, improvement to management and authorization of leave and overtime, changes to user functionality in the PeopleSoft Human Resources Management System (HRMS), and development of formal and approved guidelines in the administration of leave and overtime would be beneficial.

Introduction

The Audit of Leave and Overtime is part of the approved Secretariat's Risk Based Audit Plan (2007-2008 to 2009-2010).

This audit was selected based on risks associated with the complexity of the regulatory environment, including laws, policies, directives, and collective agreements applicable to leave and overtime. Secretariat employees only became subject to collective agreements on April 1, 2005. In addition, the Financial Statement Readiness Report, Phase II, indicated that the external auditors were unable to assess the adequacy of business process controls for leave and overtime because key manual and automated controls were not identified. Finally, no internal audits of leave and overtime were previously conducted.

Overtime (extra-duty pay) is defined as time worked by an employee in excess of the standard daily or weekly hours of work and for which the employee may be entitled to compensation pursuant to the provisions of the relevant collective agreement or Treasury Board authority. [1] These authorities require that overtime work be approved prior to the employee working the extra hours. Upon completion of the overtime work, the employee completes the Extra Duty Pay and Shift Work form (GC179) to claim compensation for the time worked. The employee may request either a cash payment or compensatory time off in lieu of payment. The manager authorized to sign s.34 of the FAA then signs the claim. The claim is then forwarded to Compensation and Benefits (CAB), Human Resources Division (HRD) of the Corporate Services Branch (CSB) for verification and entry into the Regional Pay System (RPS) for payment or entry into PeopleSoft HRMS for time off in lieu of cash payment.

Leave is defined as an authorized absence from duty. [2] The collective agreements and Terms and Conditions of Employment Policy set out employees' paid and unpaid leave entitlements. Departmental employees and supervisors use PeopleSoft HRMS, a human resources information management system, to process and record leave. Leave without pay and leave cash-outs require written authorization and approval by a manager authorized to sign s.34 of the FAA. The claim is then forwarded to CAB for verification and input into the RPS.

The Public Service Employment Act, the FAA, and a series of Treasury Board policies and collective agreements govern the management of leave and overtime. TB Circular 1977-37: Pay Administration clarifies the overall responsibility for pay administration by assigning departments the responsibility for the integrity of the overall pay process. As well, all payments and settlements must be verified and certified pursuant to s.34 of the FAA as governed by the Treasury Board's Policy on Account Verification.

CAB administers and provides advice on leave and overtime and has functional responsibility for ensuring the accurate inputting and processing of overtime claims, while the Financial Management Directorate (FMD) within CSB has functional responsibility for ensuring accurate accounting and financial reporting of these expenditures.

Audit Objective and Scope

The objective of the audit was to assess the adequacy and effectiveness of internal controls related to the administration of leave and overtime. Specifically, the audit assessed the extent to which the control framework ensured the effective and efficient processing of leave and overtime.

This audit was primarily a compliance audit, focused on the appropriateness and effectiveness of the existing management framework in place to support leave and overtime activities and compliance with relevant departmental regulations and policies.

The audit covered the FY 2006-2007 and the examination phase was conducted between April and June 2008.

The scope of the audit did not include an assessment of the effective use of leave and overtime. Also excluded from the scope were maternity and parental leave, because they are part of the Internal Audit of Pay and Benefits currently in progress. In addition, the audit did not validate internal controls within related business applications. Given that management leave for executives is governed by a separate series of authorities, it was also excluded from the scope.

Audit Criteria

The audit criteria and audit tests were developed based on policies, procedures, collective agreements and the Office of the Comptroller General's Guide on Core Management Controls, which focus on the federal government's Management Accountability Framework (MAF) in the following three categories:

- Governance and Human Resource Management

- Internal Control and Policy Compliance

- Risk Management

These audit criteria were used to assess the adequacy and effectiveness of the Secretariat's management control framework and are presented in Appendix 1.

Approach and Methodology

The audit approach and methodology is risk-based and is consistent with the International Standards for the Professional Practice of Internal Auditing and Treasury Board's Policy on Internal Audit. These standards require that the audit be planned and performed in such a way as to obtain reasonable assurance that the audit objective is achieved. The audit was conducted in accordance with an audit program that defined audit tasks to assess each criterion.

The approach used in carrying out the audit included the following:

- Review of applicable legislation, policies, procedures, and other information related to the processing of leave and overtime and to related management practices;

- Interviews with management and staff of CSB;

- Walkthroughs to observe the process and controls for reviewing, authorizing and processing overtime payments;

- Mapping and analysis of the leave and overtime business processes;

- Selection of three sectors with high dollar volume overtime expenditure subject to detailed examination.

- Review of a random sample of 40 overtime transactions from the overtime data for the three selected sectors with high users of overtime and vouching them to original documents for compliance with the control framework;

- Review of 59 transactions of selected leave types based on risk assessment and client feedback. Judgemental and random sampling methodologies were used in the selection of this sample; and

- Interviews with three sector heads, four managers with s.34 authority and eight employees within the sectors that had a high number of overtime claims.

Overview

CSB provides service and support to the Secretariat for human resources, financial and administrative management, information management and information technology and security.

As at November 2007, the Secretariat had 1,199 FTEs in approximately 13 occupational groups represented by seven different collective agreements. The departmental unaudited financial statements for 2006-2007 reported annual salary and employee benefits of $105,488,000 as part of operating expenses.

The Secretariat's leave and overtime expenditures for FY 2006-2007 are as follows:

| TBS: Leave and Overtime Expenditures for FY 2006-07 | |

|---|---|

| Total (Net) pay In lieu of leave (Indeterminate) | $423,113 |

| Total (Net) pay in lieu of leave (term, casual, part-time) | $43,649 |

| Total | $466,762 |

| Overtime (indeterminate) – paid in cash | $1,068,892 |

| Overtime hours worked and compensated in leave (in lieu of cash payment) (Indeterminate) [3] | 4,620 |

| Salaries and employee benefits per the Secretariat's unaudited financial statements [4] | $105,488,000 |

| Overtime percentage (of above) [5] | 1.01% |

The extent of overtime as a percentage of salaries could not be accurately calculated because the numerator does not include overtime hours compensated in time-off in lieu of payment. These overtime hours are not translated into monetary amounts by CSB for financial reporting purposes. In addition, the denominator includes salaries, wages and benefits of those employees who were not entitled to claim overtime pursuant to their terms and conditions of employment. Consequently, this understates total overtime as a percentage of salary dollars.

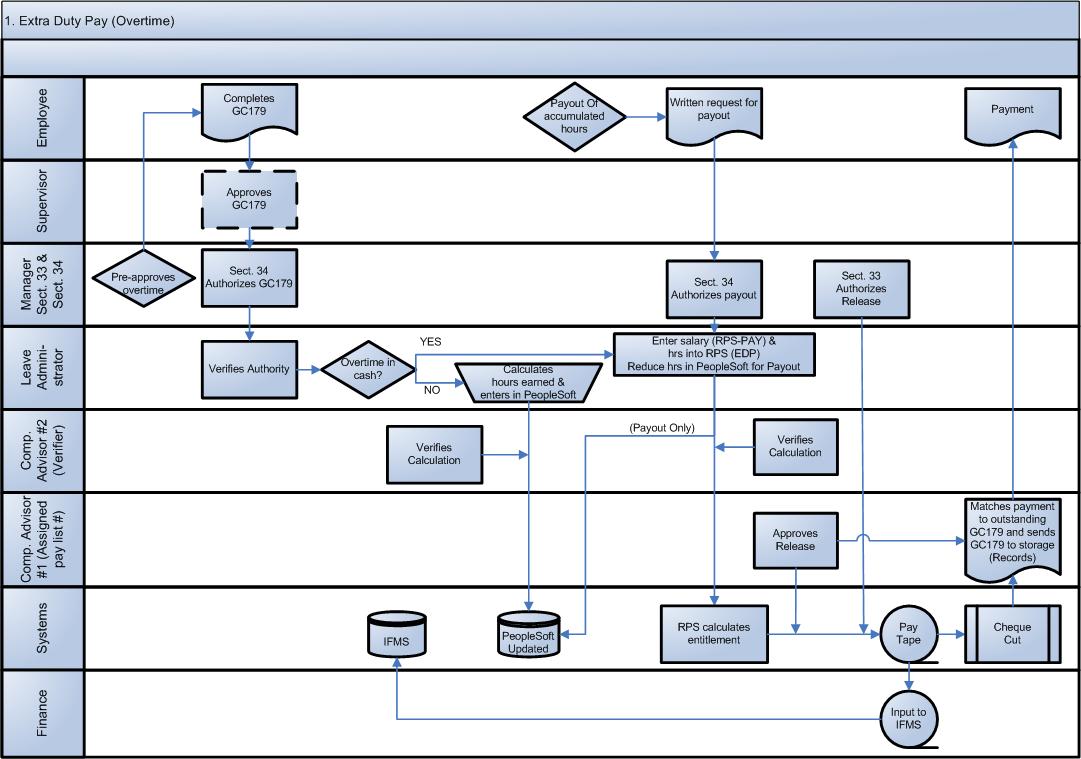

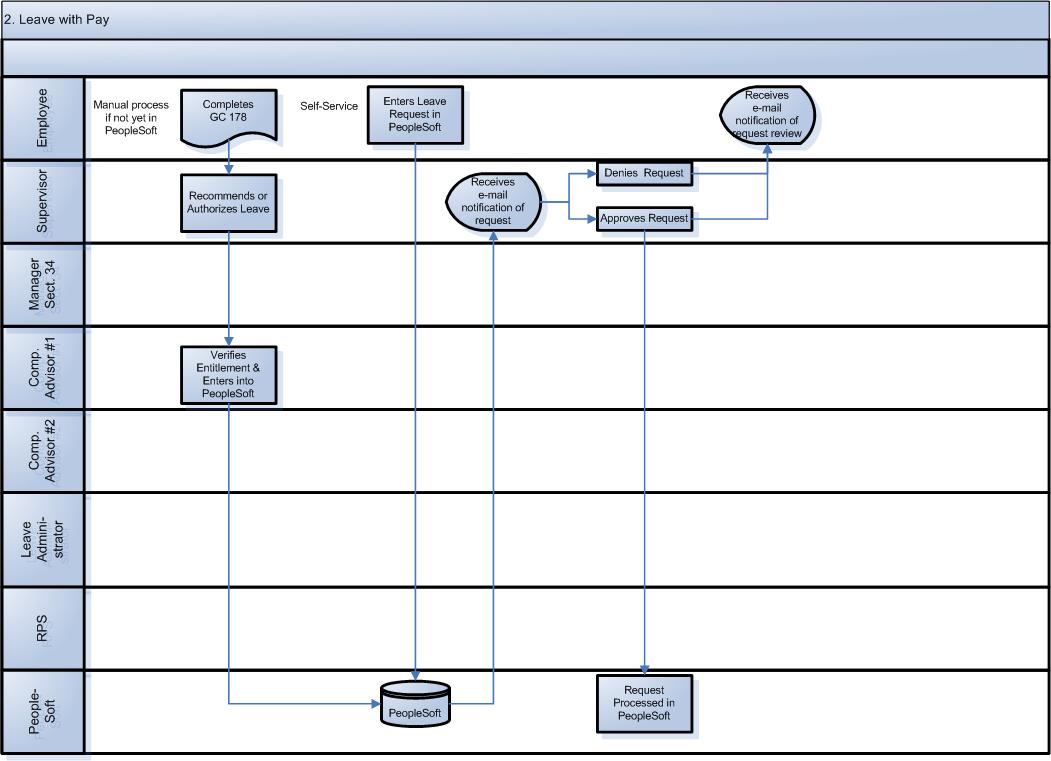

Leave and overtime data flows through the following systems (see workflow represented in Appendix 2):

- PeopleSoft – a non-financial HRMS for storing employee data and tracking leave;

- Online Pay – the gateway to the Public Works and Government Services Canada's RPS that calculates pay for federal government employees and issues cheques; and

- Integrated Financial and Materiel System (IFMS) – SAP R/3 represents the general ledger and records all salary and expense transactions.

Audit Results

1. Governance and Human Resources Management

1.1 Accountability, Roles and Responsibilities

An overall management framework for leave and overtime is in place but accountabilities, roles and responsibilities could be clearly articulated.

A key control for any program or activity is that related authorities, responsibilities and accountabilities are clear and well communicated.

The audit found that there was no complete picture of accountabilities, roles and responsibilities. While individual operational units within CSB know their own roles and responsibilities, there was little integration of operational responsibilities within CSB regarding leave and overtime and little documented knowledge of workflows.

In addition, CSB and Secretariat sectors interviewed did not communicate roles and responsibilities for leave and overtime. For example, CAB indicated that sector management is responsible for monitoring and analyzing leave and overtime for their areas of responsibility while sector management believes that it is CAB's role. In fact, CAB is only conducting this review at the corporate/departmental level.

Recommendation:

- 1. Assistant Secretary, Corporate Services Sector (CSS) in consultation with Secretariat officials should ensure that accountabilities, roles and responsibilities are clearly defined and formally communicated to managers, employees and key stakeholders involved in the leave and overtime process.

1.2 Learning and Training

While there is a framework for a formal training program for compensation advisors, it is currently incomplete and not formally in place.

Those involved in the administration of leave and overtime should receive a sufficient level of training to ensure full compliance with policies and requirements. A training program on compensation and benefits is in place and employees are expected to complete the program in 48 weeks. However, it lacks certain necessary elements such as desktop procedures that would provide a fully effective learning experience to compensation advisors.

The audit also found that there is a high turnover rate among CAB employees with knowledge of who is responsible for what and how the process works. For example, four of the six senior compensation advisors left the department during FY 2006-2007. All five new hires engaged in September and October 2006 had left by June 2007.

There were no written procedures for processing leave and overtime at the planning phase of this audit – only tools, checklists and calculation sheets. Desktop procedures are currently being developed. Formal desktop procedures and a comprehensive training program will help offset the effects of having a high turnover rate among employees who have corporate knowledge and are members of a highly mobile classification group.

Recommendation:

- 2. Assistant Secretary, CSS should ensure that written procedures for processing leave and overtime are complete, approved, and included in the updated training program for new CAB compensation advisors.

2. Internal Control and Policy Compliance – Overtime

2.1 Business Processes and Controls

Overtime Reporting

The full cost and impact of employee overtime is not known.

The cost of overtime incurred in both cash and compensatory time off should be reported in order to reflect the true (actual and implied) cost of doing business.

Currently, the reporting of overtime costs is inconsistent. Overtime is an operating cost. When overtime is compensated in cash the calculation and reporting of the cost is straightforward: it is the amount paid to the employee. When overtime is compensated in leave, it is reported by unit of time and not translated into a monetary value for comparative purposes. During FY 2006-2007, compensatory leave earned and used amounted to approximately 4,620 and 4,050 hours respectively.

Although outside the scope of this audit, it was noted that unrecorded overtime exists and is not being consistently managed at the Secretariat. Unrecorded overtime refers to the time worked which is not reported on GC179 and not recorded in PeopleSoft HRMS and for which an employee has the right to be compensated under a collective agreement. Unrecorded overtime does not refer to the normal flexibility that is expected from professionals.

Because the unrecorded overtime does not leave a management trail, it is difficult to detect and consequently difficult to measure. The extent of unrecorded and unreported overtime could not be estimated in the absence of objective, quantifiable and verifiable information. According to the results of the 2005 Public Service Employee Survey, 57 per cent of the 450 respondents stated that they could not always complete their work during regular working hours, 44 per cent stated that they were either partially compensated or not compensated at all for the overtime hours worked in the previous year, and 37 per cent felt that they could not claim overtime for hours worked.

Historically, overtime incurred and compensated in compensatory time off during the fiscal year was not recognized as a cost of doing business. In the auditors' opinion, this distorts the true picture of the cost of doing business and may affect the ability of managers to effectively understand the impact of overtime and plan workload requirements. In addition, fund centres where overtime is compensated in cash during the fiscal year, are perceived to have operated less efficiently and economically than those fund centres where overtime is compensated in time. This could negatively affect managerial and employee sense of fairness and in turn could increase staff turnover levels.

Recommendation:

- 3. Assistant Secretary, CSS in consultation with the Secretariat should consider developing a consistent and inclusive approach for corporate reporting of overtime that reflects the true value of the total cost of doing business.

Overtime Forecasting

The salary forecasting system is not used consistently resulting in system reports that display a wide variation between estimated and actual overtime expenditures.

One of the goals of the Financial Information Strategy is to provide high quality, timely information to decision makers in both departments and central agencies. Good data quality is critical for accurate reporting, for reliable budget forecasts, and for effective decision-making.

The audit noted that annual forecasting of overtime activity and cost, as recorded in the salary forecasting system, has been significantly underestimated the past two fiscal years. It should be noted that the forecast for FY 2007-2008 appeared to be underestimated as well. A large part of the reason for this discrepancy is that some organizations are monitoring their overtime outside of the formal system.

Fund centre managers interviewed said they use the prior year's overtime estimates and actual expenditures to forecast the overtime requirements for the coming fiscal year. This approach to forecasting is prescribed by the FMD. They also stated that it would always be difficult to estimate unplanned or unusual workload that arises from events such as the passing of the Federal Accountability Act, which put a high demand on employees, and parliamentary and cabinet requirements.

Employees interviewed indicated that overtime is related to the specialized nature of the business and driven by the need to accommodate parliamentary demands and schedules as well as cyclical peak periods of heavy workload and deadlines.

Managers interviewed indicated that effort is made to see that overtime is minimized and equitably distributed to ensure work-life balance. The audit noted that management uses contract, casual and temporary help when appropriate. However, due to a requirement for specialized knowledge of many positions, overtime is unavoidable.

Tools for accurately forecasting overtime are not adequately used. Not all overtime forecasts are entered into the salary forecasting system. Overtime forecasts tracked separately are not rolled up on a corporate level, which results in global forecasts that are not accurately projecting actual year end overtime costs.

Recommendation:

- 4. The Secretariat in consultation with FMD, should forecast overtime requirements by using the salary forecasting system and taking into consideration historical trends, the likelihood of unusual events recurring every year and lessons learned from gaps in previous years' forecasts.

2.2 Policy Interpretation and Compliance

Errors in the completion of overtime forms could be avoided.

Overtime earned and taken should be in accordance with applicable authorities. Areas of concern or dispute over policy should be properly raised, formally resolved, and communicated by responsible authorities in a clear and timely manner.

The audit found that overtime forms are prepared manually by the employee and once approved are submitted to CAB for processing. A leave administrator (or a compensation advisor trainee) then manually reviews overtime forms for completeness, accuracy and adherence to collective agreements. For cash payment, the leave administrator will input the overtime hours earned into RPS at the applicable rate along with the relevant employee salary information. From that input, RPS automatically calculates the overtime payment. For compensatory leave, overtime hours earned are entered into PeopleSoft under the applicable entitlement code. These transactions are peer reviewed by a compensation advisor for accuracy, and then authorized for processing and payment by a s.33 manager.

Overall, 26 of 40 overtime forms reviewed (65 per cent) required the leave administrator or compensation advisor who inputs or verifies the form to make at least one correction to the data entered by the employee. These errors included incorrect dates worked, incorrect entitlements, incorrect arithmetic and unclear manager approvals.

Minor errors were found in 3 of the 40 overtime claims that the audit examined. One of the claim forms reviewed had an input error made by CAB and the other two had errors made by the employees who filled them out that were not corrected by CAB.

Most overtime claimants interviewed were comfortable with the overtime form, although some felt it could be made easier to understand. Overall, there was no formal training provided on overtime entitlements and completing the overtime form. The audit noted that many employees were not aware of their entitlement to a meal allowance after working continuously for a specified number of hours after their regular workday.

Only occasionally, employees or managers will receive calls from compensation advisors to clarify an overtime claim. According to the managers interviewed, issues concerning policy interpretation rarely arise, but when they do, managers refer to the collective agreements and will consult with CAB.

Based on the interviews conducted, the majority of overtime is approved in advance whenever possible. Most pre-approval is done verbally, some is done through e-mail and a small number of employees have a blanket pre-approval due to the nature of their work.

As manual forms and procedures will always be subject to human error, it is important that compensation advisors continue to conduct a thorough peer review to ensure the accuracy of overtime claims processed. As well, it is important that employees and managers accurately complete overtime forms because inefficiency results when compensation advisors have to correct errors on the submitted forms or supply omitted information.

Refer to Recommendation 6.

2.3 Expenditure Authorization and Certification

Controls for fulfilling responsibility under s.33 and s.34 of the FAA are not adequate.

The Policy on Delegation of Authorities states that departments must delegate payment authority (s.33) to positions classified as “financial officer” who can independently verify how other officers exercise their spending authority (s.34). Also, departments must establish adequate controls to ensure that a specimen signature document is prepared as soon as a new employee is appointed to a position with delegated authorities. Specimen signature documents and delegation documents must be available in all locations where the signatures will have to be recognized and honoured.

In CAB, compensation advisors processing overtime claims are not validating the s.34 signatures against the signature cards of managers authorizing the overtime claims. The audit team examined 40 processed overtime claims and was able to verify 83 per cent of signatures in the on-line Financial Signing Authority System. The remaining 17 per cent of signatures could not be found under the fund centres assigned to the transactions and therefore could not be verified.

As well, supervisor signatures and/or s.34 signatures that approved and authorized overtime claims were not always legible. Neither were these signatures supported by a supervisor's or manager's printed or typed name to validate the signature, as the overtime claim form does not prescribe it.

Without access to signature cards, compensation advisors cannot validate s.34 authorities before payments are made. There is potential risk that that the delegation of authority has been withdrawn or that claims are approved and charged to a fund centre where a supervisor does not have a s.34 authority. In addition, failing to authenticate the s.34 signature against delegation documents is in contravention of procedural requirements under the Treasury Board's Policy on Delegation of Authorities and does not comply with s.33 and s.34 of FAA certification.

Furthermore, the Policy on Account Verification includes a guideline stating that departments should develop and publish specific policies and procedures for staff to follow when verifying accounts pursuant to s.34 and for the quality assurance review when gauging the adequacy of s.34 account verification.

The audit examination of 40 overtime payment transactions revealed that all overtime expense claims and payment information were properly filed in the employees' personnel files and were available for review purposes. However, the claims themselves contained inconsistent information for account verification purposes. For example:

- 30 per cent of overtime forms did not identify a reason code for the overtime worked; and

- 58 per cent of overtime forms did not have a supervisor's signature for authorizing the overtime worked.

Recommendation:

- 5. Senior Financial Officer, Secretariat should ensure that access to the appropriate financial signing authority system is granted to compensation advisors so that s.34 signatures can be verified before s.33 authorizes the payment.

- 6. Assistant Secretary, CSS should ensure that guidelines are developed for filling out overtime forms. The guidance documentation should articulate roles and responsibilities, definitions and terms, and should include common examples to assist both management and staff.

3. Internal Control and Policy Compliance – Leave

3.1 Business Processes and Controls

PeopleSoft HRMS

Controls in the PeopleSoft HRMS to manage leave transactions in keeping with existing policies and requirements are weak.

The Secretariat uses PeopleSoft, an automated human resource system to manage leave activities. It operates in a self-service environment in which employees enter and update their leave transactions and verify the accuracy of their various leave balances.

The audit found a number of data control and processing concerns with the current version of PeopleSoft that affect the reliability of leave events and leave balances.

- Employees have access to a complete list of leave codes in the system from which to pick, irrespective of entitlements under their specific collective agreements. The system does not require supervisors or managers to verify that leave types being approved are those that an employee is entitled to under his or her respective collective agreement.

- There is no explanation or interpretation of leave codes available in PeopleSoft, and the audit did not identify any quick reference to these codes outside of the system.

- PeopleSoft allows leave balances to decline into negative values, and does so without requiring approval from higher-level management.

- The system does not restrict leave approval to delegated supervisors. A colleague could approve, deny or delete a leave request. This in fact weakens the effectiveness of delegated authority.

- Leave reports are not being generated for employees or managers for monitoring purposes. The PeopleSoft portal does allow managers to view leave balances of their direct reports but does not provide them with access to leave balances for employees who have been set up in the system to report directly to a supervisor.

The Government of Canada version of PeopleSoft is tailored to the federal government public service environment with limited customization. Human Resources Information Management Unit (HRIM), HRD has made additional modifications to PeopleSoft HRMS (Version 8.0) for use by the central agency cluster. Changes to Version 8.0 have been limited due to the pending upgrade to a new version of PeopleSoft. Consequently, employees may be requesting and are granted leave that they are not entitled to under their respective collective agreements. Also, the risk exists that supervisors may approve leave against nil or negative leave balances due to a lack of access to information on employees' leave summaries or balances.

Recommendation:

- 7. Assistant Secretary, CSS should ensure that changes to user functionality in PeopleSoft are formally identified, evaluated, ranked, documented and approved. Until this occurs, temporary controls should be implemented to ensure compliance with leave requirements.

3.2 Policy Interpretation and Compliance

Guidelines

A complex suite of laws, collective agreements and Treasury Board policies governs leave. There is no mechanism in place to clearly and easily communicate how Secretariat managers and employees manage leave entitlements.

Business processes and controls to capture, record, authorize, activate and report leave events should be explicit, consistent, and formally approved.

Leave earned and taken should be in accordance with applicable central agency and departmental policies, and collective agreements. Issues, concerns, or disputes over policy should be properly escalated and formally resolved and communicated by responsible authorities in a clear and timely manner. Leave payments should be properly authorized and supported by the requisite documentation and information for account verification and the release of funds.

There are no formally approved, consistent departmental guidelines to ensure compliance with leave regulations and requirements. The audit did not identify any single repository of policies, procedures, and tools related to leave and no mechanism is in place to clearly and easily communicate how Secretariat managers and employees are to manage leave.

Leave is delegated to the supervisory level. However, there are no common guidelines for and understanding of employee entitlements. Some supervisors interviewed were unsure as to when to exercise discretion when granting leave for such absences as family related leave and bereavement leave.

Employees and managers were unclear about their entitlements. For example, some supervisors and employees interviewed were not aware of the Leave With Pay Policy that allows leave for medical and dental appointments.

A sample of 59 leave events was selected for detailed examination. Based on risk assessment and input from the client, the sample included employees with high incidences of certified and uncertified sick leave, family related leave, leave without pay, other paid leave other, leave cash-out, and marriage leave.

The review of five personnel files of employees with high incidences of certified sick leave (856 to 2,183 hours) for the audit period found that less than half (two employee files) contained medical certificates. The risk related to certified sick leave is limited in this case because the collective agreement no longer differentiates between certified and uncertified sick leave and management has discretionary power over when to ask for medical certificates. However, when certified sick leave is booked, it is a prudent practice to record an attestation in PeopleSoft or the delegated supervisor forwards a copy of the medical certificate for retention in the employee's personnel file.

The audit also found that two of five uncertified sick leave events of 60 and 300 hours per request were unsupported. It is a good management practice to certify the sick leave of such a duration.

Five employees were granted marriage leave after their respective collective agreements had been signed to replace the “Marriage Leave” entitlements with the “One Time Vacation Leave Entitlement”. This resulted in over-entitlements.

Recommendation:

- 8. Assistant Secretary, CSS should institute formal information sessions with Secretariat employees to update and clarify leave entitlements in order to reinforce compliance with leave policies.

4. Risk Management

There is a lack of risk management of leave and overtime activity at the Secretariat, sector and CSB levels.

The Risk Management Policy reasons that effective risk management ensures the continuity of government operations. Because all manner of risks are present throughout government operations, successful delivery of a program is contingent upon effective and cohesive controls to manage these risks.

Treasury Board's Policy on Active Monitoring requires that departments actively monitor on an ongoing basis their management practices and controls using a risk-based approach.

Departments must develop and maintain their capacity to detect significant risks as well as potential and actual control failures, and take timely and effective action to address deficiencies.

Neither managers nor sector heads interviewed periodically monitor overtime payments they have approved to ensure the expense payments are correct. Generally, sector heads and managers were of the opinion that once a manager signs an overtime claim, CSB then takes all subsequent responsibility for ensuring the accuracy, validity, and reconciliation of these individual expenses.

Overtime is reviewed by managers but only as part of the salary management envelope during the annual budgeting process or for cash-out purposes. CAB performs monitoring and analysis of overtime activity, such as reviewing annual reports on leave, overtime, and compensatory time for cash-out and accrual purposes. This activity, however, is undertaken only at the corporate level.

Managers interviewed were aware that excessive overtime could lead to health issues. They also indicated that there is a significant change in the core values of the new generation of public service employees. Workers' increased expectations of flexibility and work-life balance, coupled with an increased level of mobility, underscores the need for managing and monitoring workload risks and trends to ensure appropriate and timely action.

The audit found limited monitoring of employee leave recorded in the PeopleSoft HRMS. Tools for monitoring individual leave and related trends are not readily available to managers. Also, there is limited capacity to monitor or periodically review leave in the HRD other than for cash-outs at year-end.

In general, managers cannot easily review the overall leave ‘picture' for their sectors. There are a number of limitations in PeopleSoft that inhibit managers and sectors from carrying out their responsibilities for monitoring leave. Supervisors and managers have limited ability to monitor the leave status of their direct reports. No leave reports are automatically generated for formal monitoring; reports are only generated by the HRIM when specifically requested.

Monitoring is generally perceived to be an activity with a low return, especially given the role of CAB to identify errors, employee monitoring of their own leave and overtime claims, and the relatively low dollar value of these claims posing minimal risks. Nevertheless, these incomplete management controls can lead to such things as overpayments, over-entitlements, and overtime payment charges to incorrect fund centres.

Due to inherent process weaknesses, compensating controls such as asking employees to confirm that they agree with their leave balances in PeopleSoft would help to alleviate potential disputes in regards to PeopleSoft balances in the future.

Recommendation:

- 9. The Secretariat should develop and implement a risk management process in order to identify, assess, address, monitor and communicate risk associated with the administration of leave and overtime.

Overall Conclusion

In general, leave and overtime expenditures for the fiscal year ending March 31, 2007 were managed in accordance with applicable laws, policies and collective agreements. However, more could be done to enhance and strengthen controls and guidance in order to reduce the risk of non-compliance, material errors and abuse. For example:

- clear articulation of roles and responsibilities for overtime and leave management;

- update and finalization of training for compensation advisors;

- a more consistent and inclusive approach to understanding the full cost of overtime;

- a more consistent use of the salary forecasting system to accurately reflect the budgeted and actual overtime expenditures;

- more guidance for employees to complete overtime forms correctly;

- improvement of verification of s.34 signatures for overtime expenditures;

- enhancement of PeopleSoft HRMS controls to ensure the reliability of leave data;

- communication, update and clarification of employees' understanding of leave entitlements; and

- development and implementation of a formal risk management and monitoring process for leave and overtime.

Appendix 1: Audit Criteria

| Lines of Enquiry | Audit Criteria [*] |

|---|---|

| Governance and Human Resources Management | Accountabilities, roles and responsibilities for the administration of leave and overtime are adequately defined, comprehensive, current and well communicated. |

| Training of management and staff with leave and overtime responsibility, and awareness of overtime policies and practices by departmental staff, effectively supports the processing of leave and overtime events. | |

| Departmental management organizes employees, and the departmental workload, in a manner that minimizes the amount of overtime required. | |

| Recruitment and retention (R&R) planning and activities are sufficient to ensure key departmental positions are staffed to meet workload demands. | |

| Internal Control and Policy Compliance | Business processes and controls to capture, record, authorize activate and report leave and overtime events are formal, comprehensive, consistent and formally approved. |

| Leave and overtime earned and taken are in accordance with applicable central agency and departmental policies, regulations, directives and collective agreements. Issues or areas of policy concern or dispute are properly escalated and formally resolved and communicated by responsible authorities in a clear and timely manner. | |

| Overtime payments are properly authorized and are supported by the requisite documentation and information for account verification and funds release. | |

| Risk Management | Processes for monitoring are in place to identify and communicate operational and administrative problems and issues for departmental overtime, and subsequent reporting to management is conducted in a clear, comprehensive and timely manner. |

| Mechanisms are in place to identify, assess and mitigate administrative and operational risk related to departmental leave and overtime. |

- [*] Source: The Office of the Comptroller General's Core Management Controls which are organized around the federal government's Management Accountability Framework.

Appendix 2: Business Process Flowcharts

Graphic 1: Display Full Size Graphic

Graphic 1: Display text version

{kind=link}

Graphic 2: Display Full Size Graphic

Graphic 2: Display text version

{kind=link}

Appendix 3: Management Action Plan

| Priority Ranking | Recommendation | Management Action | Completion Date | Office of Primary Interest (OPI) |

|---|---|---|---|---|

| High | Recommendation 1: Assistant Secretary, Corporate Services Sector (CSS) in consultation with Secretariat officials should ensure that accountabilities, roles and responsibilities are clearly defined and formally communicated to managers, employees and key stakeholders involved in the leave and overtime process. | Review TB Policy on leave | Completed | HRD and CAB |

| Consult with TBS policy center | Completed | |||

| Conduct gap analysis | Fall 2008 | |||

| Develop accountability framework | Fall 2008 | |||

| Present new accountability framework to Senior Management for approval | Winter 2009 | |||

| Medium | Recommendation 2: Assistant Secretary, CSS should ensure that written procedures for processing leave and overtime are complete, approved, and included in the updated training program for new CAB compensation advisors. | Draft procedures for processing of leave and overtime | Fall 2008 | HRD and FMD |

| Update Compensation and Benefits training program accordingly | ||||

| Best Practice | Recommendation 3: Assistant Secretary, CSS in consultation with the Secretariat should consider developing a consistent and inclusive approach for corporate reporting of overtime that reflects the true value of the total cost of doing business. | The CSB will conduct a semi-annual analysis of the cost of OT leave taken by organization and report to senior management of any areas of concern. | October 2008 | FMD |

| Medium | Recommendation 4: The Secretariat in consultation with FMD, should forecast overtime requirements by using the salary forecasting system and taking into consideration historical trends, the likelihood of unusual events recurring every year and lessons learned from gaps in previous years' forecasts. | This recommendation refers to the inconsistent use of the salary forecasting system to project OT costs. CSB will ensure that TBS management are aware that the usage of the salary forecasting system is mandatory and that overtime should form part of any projections. Financial Management Advisors will assist managers in determining strategies for accurate forecasting. | September 2008 | FMD |

| High | Recommendation 5: Senior Financial Officer, Secretariat should ensure that access to the appropriate financial signing authority system is granted to compensation advisors so that s.34 signatures can be verified before s.33 authorizes the payment. | HR Compensation Advisors will be given access and training on the Financial Signing Authorities database. | Completed | FMD |

| The Financial Signing Authorities database will become a standard tool for compensation advisors from this point forward. | Fall 2008 | HRD | ||

| Overtime request form (GC179) will be modified to include the Sect. 34 Manager's “printed name” and “fund centre” boxes to simplify the search and save time. | Fall 2008 | HRD | ||

| Medium | Recommendation 6: Assistant Secretary, CSS should ensure that guidelines are developed for filling out overtime forms. The guidance documentation should articulate roles and responsibilities, definitions and terms, and should include common examples to assist both management and staff. | Develop internal guidelines for the completion of overtime forms |

Spring 2009 | CAB |

Articulate roles and responsibilities in the guidelines which are aligned with Recommendation #1 |

||||

Cross-check guidelines to ensure consistency with the procedures developed pursuant to Recommendation #2 |

||||

| High | Recommendation 7: Assistant Secretary, CSS should ensure that changes to user functionality in PeopleSoft are formally identified, evaluated, ranked, documented and approved. Until this occurs, temporary controls should be implemented to ensure compliance with leave requirements. | Identify issues with the list of codes in Leave Self-Service and added customizations. | Completed | HRMS |

| Implement, test and document changes so that employees are only able to take leave according to his\her leave entitlements. | Completed | |||

| Remove the Leave calculator functionality from the system to prevent employees from requesting leave with negative balances. | Completed | |||

| Develop tools to monitor negative balances on a monthly basis. | Completed | |||

| Analyse the issue of leave approval restrictions once PeopleSoft 8.9 Upgrade is implemented and make recommendations to Senior Management. | Summer 2009 | |||

| Medium | Recommendation 8: Assistant Secretary, CSS should institute formal information sessions with Secretariat employees to update and clarify leave entitlements in order to reinforce compliance with leave policies. | Develop training sessions for managers and employees through subject matter specialists |

Spring 2009 | HRD |

Deliver course via On-Line access and/or departmental orientation training (TBS Bootcamp). |

||||

Training sessions and course materials will include points for managers to consider when exercising their discretionary authority vis-ŕ-vis requesting medical certificates in sick leave request situations. |

||||

| High | Recommendation 9: The Secretariat should develop and implement a risk management process in order to identify, assess, address, monitor and communicate risk associated with the administration of leave and overtime. | HRD to provide quarterly reports on leave usage (to supervisors) and compensatory leave (to fund centre managers). The new Salary Forecasting System (SFT SAP), which was implemented April 2008, provides management the capacity of reviewing their overtime expenditures by individual employee and transactions. |

Spring 2009 | HRD/FMD |

HRD to provide guidance and support to supervisors and fund centre managers to analyze reports. |

Appendix 4: List of Acronyms

- CAB

- Compensation and Benefits

- CSB

- Corporate Services Branch

- CSS

- Corporate Services Sector

- FAA

- Financial Administration Act

- FMD

- Financial Management Directorate

- FTE

- Full-time equivalent

- FY

- Fiscal Year

- GC179

- Extra Duty Pay/Shiftwork Report and Authorization

- HRD

- Human Resources Division

- HRMS

- Human Resource Management System

- IAE

- Internal Audit and Evaluation

- MAF

- Management Accountability Framework

- RPS

- Regional Pay System

- Secretariat

- Treasury Board of Canada Secretariat

Footnotes

- [1] Terms and Conditions of Employment Policy

- [2] Collective Agreements

- [3] Overtime taken as compensatory leave is not calculated in terms of cost.

- [4] Salaries and Employee Benefits include severance pay and personnel who cannot claim overtime.

- [5] Includes salaries of employees who are not eligible to earn overtime under the terms of employment.