Directive on Accounting Standards: GC 5000 Recording Financial Transactions in the Accounts of Canada

Note to reader

This document is part of the Appendix A of the Directive on Accounting Standards.

A. Primary PSAS reference

- N/A

B. Effective date

C. Government of Canada Consolidated Financial Statements

- The objectives of this section are to:

- Ensure the organization’s classification of accounts structure is soundly managed and is based on the government-wide classification structure which allows for accurate identification, aggregation and reporting of financial transactions.

- Ensure that the financial information is accurately reported in the Public Accounts of Canada and departmental accounts.

- The Accounts of Canada are a centralized record of the financial transactions and account balances of the Government of Canada, maintained by the Receiver General. The Accounts of Canada consist of the summarized classification of transactions and account balances by responsibility, financial reporting, authority, program, object and transaction type.

-

The classification structure for the Accounts of Canada is composed of the following six elements:

- Authority classification

- Is the authority (parliamentary appropriation (vote), statute or other legislative authority) under which the financial transaction is authorized. It also identifies whether the transaction is budgetary or non-budgetary and statutory or non-statutory.

- Financial reporting classification

- Identifies the relevant asset, liability, equity, revenue or expense account and is used to maintain the accounts in the “Receiver General-General Ledger” and to prepare financial statements and the Public Accounts of Canada.

- Object classification

- Identifies the type of goods or services acquired, the transfer payments made, the source of receipts or the cause of increases or decreases in assets and liabilities.

- Program classification

- Identifies the core responsibility within the Departmental Results Framework to which a financial transaction is associated. When applicable, the core responsibility must be broken down further to the Program Inventory to capture the lowest level.

- Responsibility classification

- Identifies the organizational unit that is responsible and accountable for the transaction. The responsibility structure must be consistent with the organizational structure to allow aggregation at the department or agency level.

- Transaction type (internal/external) classification

- Identifies transactions as being either internal to the government or external (i.e., related to parties outside the Government of Canada reporting entity), allowing the government to produce consolidated financial statements that exclude internal transactions.

D. Other related references

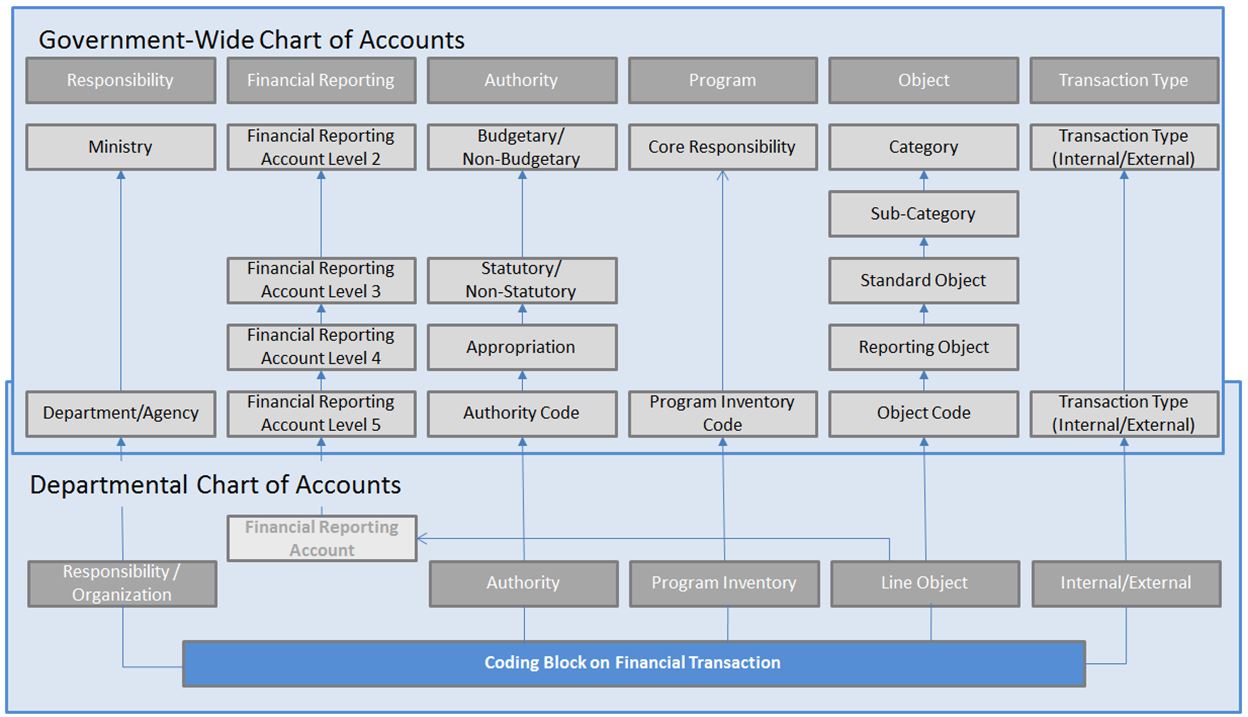

Appendix A - Government-wide classification structure and sample departmental chart of accounts

This chart exhibits the six government-wide classifications for financial transactions. It also illustrates a typical departmental chart of accounts.

Figure 1 - Text version

The top line of the chart includes the six elements of the classification structure of the Accounts of Canada and relates them to the actual code: Responsibility (Department/Agency Code), Financial Reporting (Financial Reporting Account Level 5), Authority (Authority Code), Program (Program Inventory Code), Object (Object Code) and Transaction Type (Internal/External). Each element is linked to the appropriate element in the Departmental Chart of Accounts: Responsibility/Organization, Financial Reporting Account, Authority, Program Inventory, Line Object, Internal/External.